Tax-exempt refers to incomes that are free from tax at the State, local, or federal level. The reporting of tax-free items may be on a taxpayer's business or individual tax return and shown for informational reasons only..

Tax-exempt also refer to the status of a organisation or a business which has limits on the amount of gifts or income which are taxable. These organizations include religious and charitable institutions.

Following are the below tax exempted from gross income:

- The amount received by insurance as return of premium, Life insurance policies

- Gifts, and devises bequests

- Compensation for sickness or injuries

- Income exempted under the treaty

- Pension, Retirement benefits, and gratuities

- Miscellaneous income Income obtained by other gov

- Income received by the government/ its political subdivisions

- Awards and prizes exempt by law, awards, and prizes in the sports-related tournament.

- Other benefits and 13th-month pay benefits subject to the PHP90,000 limit

- GSIS, SSS, Medicare and other contributions

- Gains from the sale of bonds, debentures, or other certificates of indebtedness with a maturity of more than five years

- Gains from the redemption of shares in the mutual fund

Who is exempt from the Income Tax?

a. Income from the foreign country of a non-resident citizen who is:

i. A citizen of the Philippines who resides abroad from the Philippines during the taxable year, either for employment permanently or an immigrant.

ii. A citizen of the Philippines who derives and works income from foreign and whose job requires him to be physically present in foreign most of the time during the taxable year

iii. A citizen who has been previously considered as a non-resident citizen and who arrives in the Philippines at any time during the year to reside permanently in the Philippines will likewise be treated as a non-resident citizen during the taxable year in which he arrives in the Philippines, with respect to his income derived from sources abroad until the date of his arrival in the Philippines.

b. Overseas Filipino Worker, including overseas seaman

An individual citizen of the Philippines who is working and deriving income from abroad as an overseas Filipino worker is taxable only on income from sources within the Philippines; provided, that a seaman who is a citizen of the Philippines and who receives compensation for services rendered abroad as a member of the complement of a vessel engaged exclusively in international trade will be treated as an overseas Filipino worker.

c. General Professional Partnership

d. Government Service Insurance System (GSIS)

e. Social Security System (SSS)

f. Philippine Health Insurance Corporation (PHIC)

g. Local Water Districts (LWD)

Who is not required to file an Income Tax Return?

- An individual earning purely compensation income whose taxable income does not exceed P250,000.00

-An individual whose income tax has been withheld correctly by his employer, provided that such individual has only one employer for the taxable year

- An individual whose sole income has been subjected to final withholding tax or who is exempt from income tax pursuant to the Tax Code and other special laws.

- An individual who is a minimum wage earner

- Those who are qualified under “substituted filing”. However, substituted filing applies only if all of the following requirements are present:

- the employee received purely compensation income (regardless of amount) during the taxable year;

- the employee received the income from only one employer in the Philippines during the taxable year;

- the amount of tax due from the employee at the end of the year equals the amount of tax withheld by the employer;

- the employee’s spouse also complies with all 3 conditions stated above;

- the employer files the annual information return (BIR Form No. 1604-CF); and

- the employer issues BIR Form No. 2316 (Oct 2002 ENCS version) to each employee.

How does Tax exemption work on Deskera Book?

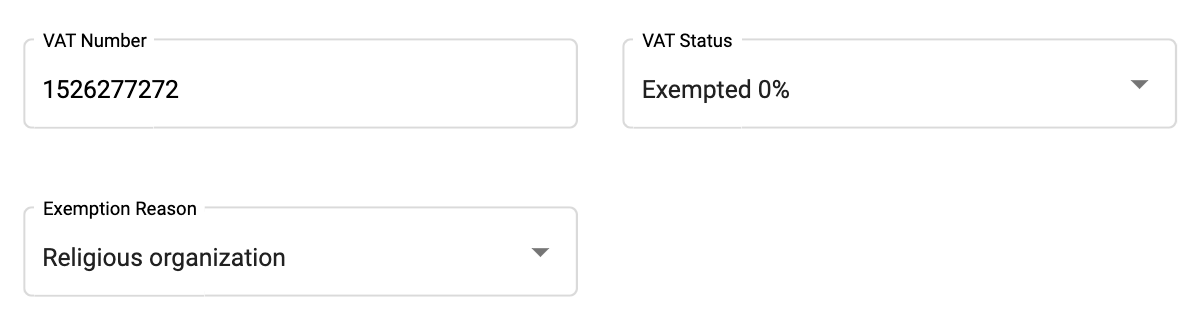

When creating a new Contact, you will need to indicate if your Contact is exempt from sales tax. If the contact is exempted from tax, tax won’t be applied to the business transactions for this particular contact. On the Add Contact page, Under VAT Status you need to select Exempted option from the dropbox .Selecting it will prompt for the Tax Exemption Reason, where from the drop down menu you can select different tax exemption reasons.

Take note that the tax-exemption reason is a mandatory field fill in if the Contact is exempt from tax.

When the Contact created is tax-exempt, sales tax will not be applied for Quotes and Invoices involving this Contact. This ensures that sales tax is not incorrectly charged.