Overview

The Employees' Provident Fund (known by its acronym EPF, or KWSP in Malay) is a Malaysian government agency that manages a compulsory savings plan and retirement planning for private and non-pensionable public sector employees.

The EPF functions through monthly contributions from employees and their employers towards saving accounts. While in savings these funds may be used in various investments by the EPF or, in some cases, by the members themselves.

Who Can Contribute

Individuals who are employed, self-employed or business owners can opt to contribute based on their own requirements. In the following pages, we have entailed the details that go with Mandatory and Voluntary contributions. As a member, you are eligible to not only enjoy annual dividends on your retirement savings, but also the many withdrawal options and benefits that come with being an EPF Member.

Benefits

There are many benefits to contributing to the EPF, listed below are some:

The EPF, by law, has a minimum dividend rate of 2.5%, but historically has had a much higher rate. For example, in 2014, the dividend rate was 6.75%.

Your EPF contributions are tax-free up to a maximum of RM4,000 per annum, since they are deducted from your chargeable income for calculation of income tax.

Withdrawal

At the age of 50, Malaysian citizens and permanent residents are allowed to withdraw up to 30% of their savings, and at the age of 55 they can withdraw their full savings.

A full withdrawal can also be made in the event that an EPF member emigrates or becomes disabled.

Foreigners who opt to contribute to the EPF may withdraw their funds when they have terminated their employment and are about to leave the country.

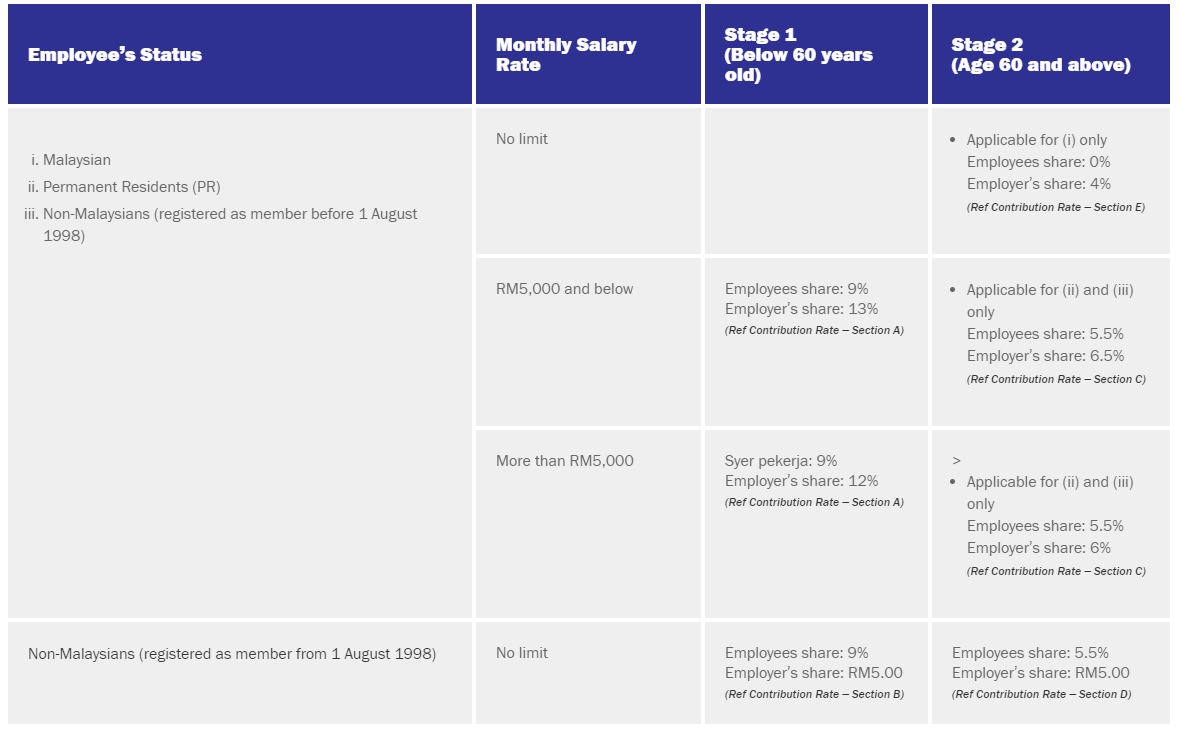

What are the contribution rates for EPF?

Under EPF rules, both employee and employer contributions are payable. Employee contributions are deducted from the employee's salary and paid to KWSP together with the employer contributions. Although the contribution rates are usually featured as a percentage of the salary subject to EPF, the percentage is approximate and the actual contributions must be taken from the EPF Contribution Table.

The EPF contribution rates vary according to the employee's age and whether they are a Malaysian/permanent resident. Foreigners who are not permanent residents are not obligated to contribute and different rates may apply if they do.

Please note, effective from Jan 2021 wages until December 2021 wages the contribution rate was reduced from 11% to 9% for employees aged under 60. However, an employee can maintain their contribution rate at 11%. If the contribution is maintained at 11%, the EPF Contribution Table applies.

Contribution Rate

Note:

- Employers are not allowed to calculate the employer’s and employee’s share based on exact percentage EXCEPT for salaries that exceed RM20,000.00. The total contribution which includes cents shall be rounded to the next ringgit.

- Effective from January 2021 salary/wage up to December 2021 (February 2021 contribution month up to January 2022).

EPF Contribution Payment

The employer must pay their employee's contributions on or before the 15th of the following wage month.

The employer must initially pay to the EPF both his and the employee's shares. However, the employer may recover the employee's share of the contribution by deducting it from the employee's wage when the wage is paid to the employee.

To ensure the accuracy and efficiency of crediting to member’s account, employer should ensure:

- The name and the NRIC in Form A should be as stated in the identification card

- The sum payment matches the contribution sum stated in Form A

Note:

Employer is responsible of submitting contribution form (Form A) together with payment for crediting purpose to member's account.