What does it really cost to produce a product—and are you calculating it accurately? The answer goes far beyond just raw materials and labor. Cost of production is a comprehensive measure that includes every expense incurred in turning inputs into finished goods. For businesses, understanding this cost is not just an accounting exercise—it’s a strategic necessity that directly influences pricing, profitability, and long-term sustainability.

In today’s competitive and cost-sensitive market, even small miscalculations in production costs can lead to significant financial setbacks. Whether you're a manufacturer, a small business owner, or part of a growing enterprise, having a clear view of your production costs helps you set the right prices, control expenses, and improve operational efficiency. It also empowers decision-makers to identify cost-saving opportunities and respond quickly to market changes.

Cost of production is not a one-size-fits-all concept—it includes various types such as fixed costs, variable costs, and indirect expenses that evolve with production levels. Knowing how to break down, analyze, and calculate these costs accurately is essential for maintaining healthy profit margins. More importantly, it allows businesses to scale confidently while minimizing waste and inefficiencies.

Modern tools like Deskera Manufacturing ERP make this process significantly easier and more accurate. With features like real-time cost tracking, inventory management, production planning, and demand forecasting, Deskera helps businesses gain complete visibility into their production expenses. Its integrated system ensures better decision-making, improved cost control, and enhanced operational efficiency—making it an essential solution for manufacturers aiming to stay competitive in today’s dynamic business environment.

What is the Cost of Production?

Cost of production refers to the total expenses a business incurs to manufacture goods or deliver services. It includes every cost involved in the production process—ranging from direct costs like raw materials and labor to indirect costs such as rent, utilities, maintenance, and administrative expenses. In simple terms, it represents the total money required to transform inputs into finished products that can be sold in the market.

These costs are broadly categorized into direct and indirect expenses, as well as fixed and variable costs. Direct costs are directly tied to the production of goods, such as the cost of wood for furniture or wages paid to factory workers. Indirect costs, on the other hand, include overhead expenses like electricity bills, factory rent, insurance, and equipment maintenance. Additionally, taxes imposed by the government and other regulatory expenses also form a part of the overall production cost.

To understand this better, consider a company that manufactures tables. It must spend on raw materials like wood, screws, adhesives, and paint, along with labor costs for skilled workers. Beyond that, the company also incurs overhead expenses such as factory rent, electricity, machinery maintenance, and administrative costs. Similarly, a pharmaceutical company must account for raw materials like chemical compounds, packaging, skilled technicians, and facility-related expenses. When all these costs are combined, they determine the total cost of production.

Tracking the cost of production is essential for evaluating a business’s profitability and efficiency. Without a clear understanding of these costs, companies cannot set accurate pricing, control expenses, or maximize profit margins. By analyzing production costs, businesses can identify inefficiencies, optimize resource allocation, and make informed decisions that support long-term growth and competitiveness.

Key Components of Cost of Production

Understanding the key components of cost of production is essential for businesses to accurately measure expenses, control budgets, and improve profitability. Production costs are made up of several interconnected elements that collectively determine the total cost of manufacturing goods or delivering services.

By analyzing these components, organizations can identify inefficiencies, reduce waste, and make better financial and operational decisions.

1. Raw Materials

Raw materials are the basic inputs used to create finished goods. They form the foundation of the production process and are directly transformed into the final product. These materials may include natural resources, chemicals, metals, plastics, or any other inputs depending on the industry. The cost of raw materials often fluctuates due to market demand, supplier pricing, and availability.

Effective raw material management is critical because even small price changes can significantly impact overall production costs. Businesses must balance quality and cost while ensuring consistent supply to avoid production delays. Proper inventory planning also helps reduce wastage and storage costs, contributing to more efficient production.

2. Labor

Labor refers to the human effort involved in the production process. It includes wages paid to workers who are directly involved in manufacturing as well as indirect labor such as supervisors, quality controllers, and maintenance staff. Labor cost is often one of the most significant components of production expenses.

Several factors influence labor costs, including employee skill levels, productivity, training programs, and availability of skilled workers. Businesses that invest in workforce training and automation often achieve higher productivity and lower per-unit labor costs. Efficient labor management ensures smoother operations and better output quality.

3. Overheads

Overheads are indirect costs that support the production process but are not directly linked to a specific product. These include expenses such as rent, utilities, administrative expenses, insurance, and taxes. Overheads can be fixed or variable depending on the nature of the expense.

Managing overheads effectively is crucial for maintaining profitability because these costs are incurred regardless of production volume. Businesses must continuously evaluate operational efficiency and eliminate unnecessary expenses without affecting productivity. Proper allocation of overheads also ensures accurate product costing.

4. Equipment

Equipment costs include both the initial investment in machinery and the ongoing expenses required to operate and maintain it. This covers purchase costs, depreciation, repairs, servicing, and upgrades. Machinery plays a vital role in modern production systems, especially in large-scale manufacturing.

Efficient equipment management helps reduce downtime, improve productivity, and extend asset life. Businesses must strike a balance between investing in advanced machinery and controlling long-term maintenance costs. Regular maintenance schedules and timely upgrades ensure smooth and cost-effective operations.

5. Packaging

Packaging includes all materials and processes used to prepare finished goods for storage, transportation, and sale. This involves boxes, labels, wrapping materials, and labor required for packing and labeling products. Packaging not only protects goods but also influences branding and customer perception.

The challenge for businesses is to design packaging that is cost-effective while still being functional and visually appealing. Over-investing in packaging can increase production costs, while under-investing may affect product safety and marketability. Efficient packaging strategies help optimize both cost and customer experience.

6. Transportation

Transportation costs include the expenses involved in moving finished goods from the production facility to warehouses, distributors, or end customers. These costs cover fuel, logistics services, vehicle maintenance, and shipping charges. Transportation is a key component of the overall supply chain.

Optimizing transportation is essential for reducing delivery costs and improving efficiency. Businesses often use route optimization, bulk shipping, and logistics planning to minimize expenses. Timely and cost-effective delivery not only reduces costs but also enhances customer satisfaction and market competitiveness.

7. Other Supporting Costs (Additional Insight)

In addition to the major components, production costs may also include other supporting expenses such as quality control, safety compliance, research and development, and administrative support. These costs ensure that production processes meet industry standards and maintain consistent quality.

Although these expenses may not directly contribute to production output, they play a crucial role in sustaining long-term operational efficiency and regulatory compliance. Businesses that manage these supporting costs effectively can maintain higher product quality while keeping overall expenses under control.

Factors Affecting Cost of Production

The cost of production is not fixed—it constantly changes due to internal business decisions and external market conditions. Various economic, operational, and technological factors influence how much it costs to produce goods or deliver services.

Understanding these factors helps businesses anticipate cost fluctuations, improve planning, and maintain profitability in changing market environments.

1. Demand

Demand plays a major role in influencing production costs. When demand for a product increases, businesses often scale up production by purchasing more raw materials, hiring additional workers, and expanding facilities. This expansion naturally increases the overall cost of production.

However, higher demand can also create economies of scale, where the cost per unit may decrease due to bulk purchasing and efficient resource utilization. On the other hand, sudden or unpredictable demand fluctuations can lead to inefficient production planning and increased operational expenses.

2. Technology

Technology significantly impacts production efficiency and cost structure. The adoption of automation, robotics, and advanced machinery can reduce dependency on manual labor and improve productivity.

Although the initial investment in technology may be high, it often leads to lower long-term production costs through faster output, reduced errors, and improved efficiency.

Additionally, modern digital systems require employee training and maintenance, which also adds to short-term costs. Overall, technology is a key driver of cost optimization in modern manufacturing.

3. Exchange Rate

For businesses that rely on imported raw materials or export finished goods, exchange rate fluctuations can directly impact production costs. A weaker domestic currency makes imported materials more expensive, increasing the overall cost of production.

Conversely, a stronger currency can reduce input costs but may make exports less competitive in global markets. Exchange rate volatility creates uncertainty in budgeting and pricing, making it important for businesses to manage currency risks effectively through hedging or supplier diversification.

4. Cost of Materials

Raw material costs are one of the most influential factors in determining production expenses. Prices of materials such as metals, chemicals, fuel, and agricultural inputs can fluctuate due to market demand, supply chain disruptions, geopolitical conditions, and transportation costs.

Even small changes in material prices can significantly affect total production cost, especially in industries with high material dependency. Businesses often manage this by negotiating supplier contracts, maintaining inventory buffers, or sourcing alternative materials.

5. Tax Rates

Taxation is an important indirect factor that affects production costs. Governments may impose various taxes such as corporate tax, manufacturing tax, or employee-related levies, all of which contribute to overall expenses. Changes in tax policies can increase or decrease the financial burden on businesses.

Higher tax rates reduce profit margins and increase the cost of operations, while favorable tax policies can encourage production expansion. Businesses must continuously monitor tax regulations to ensure accurate cost planning and compliance.

6. Interest Rates

Interest rates affect production costs indirectly through business financing. Companies often rely on loans for purchasing machinery, expanding facilities, or managing operational expenses. When interest rates rise, the cost of borrowing increases, leading to higher financial expenses. This, in turn, raises the overall cost of production.

Lower interest rates reduce financing costs and make expansion more affordable. Since interest rates are influenced by economic policies and market conditions, businesses must account for potential fluctuations when planning long-term investments.

7. Additional Influencing Factors (Operational Insight)

Beyond the major economic drivers, several operational factors also impact production costs. These include labor productivity, supply chain efficiency, infrastructure availability, and regulatory compliance requirements. Disruptions in logistics or delays in procurement can increase costs unexpectedly.

Similarly, inefficient workflows or poor resource utilization can raise per-unit production costs. Businesses that focus on process optimization, automation, and supply chain resilience are better positioned to control these hidden cost drivers.

By understanding these factors in detail, businesses can better anticipate cost fluctuations and develop strategies to maintain stable, efficient, and profitable production systems.

Types of Cost of Production

Understanding the types of cost of production helps businesses go beyond basic expense tracking and focus on how costs behave under different conditions. These classifications are especially useful for decision-making, pricing strategies, and evaluating profitability. By analyzing costs from different perspectives, businesses can better control spending, optimize production levels, and improve overall financial performance.

1. Fixed Costs

Fixed costs are expenses that remain constant regardless of the level of production or output in the short run. These costs do not fluctuate with changes in production volume, meaning a business must pay them even if it produces nothing. Fixed costs are essential for maintaining the basic structure of a business and ensuring continuity of operations over time.

These costs are particularly important for long-term financial planning because they create a baseline level of expenditure that must always be covered. Businesses consider fixed costs when setting minimum pricing levels to ensure sustainability.

Examples (conceptual):

- Long-term facility lease or rent agreements

- Salaries of permanent administrative or managerial staff

- Depreciation of production equipment and machinery

- Insurance premiums and regulatory compliance costs

Fixed costs help businesses understand their break-even point and plan production capacity more effectively.

2. Variable Costs

Variable costs are expenses that change directly in relation to the level of production. As output increases, these costs rise, and as production decreases, they fall. Unlike fixed costs, variable costs are flexible and closely tied to the actual manufacturing or service delivery process, making them a key factor in short-term production decisions.

These costs are highly significant in determining per-unit profitability because they directly influence how much it costs to produce each additional unit. Efficient management of variable costs can significantly improve margins and overall competitiveness in the market.

Examples (conceptual):

- Costs that scale with production volume or output levels

- Expenses linked to production activity intensity

- Payments that increase as more units are manufactured or delivered

- Operational costs that fluctuate with usage or demand

Variable costs help businesses evaluate scalability and production efficiency.

3. Semi-Variable (Mixed) Costs

Semi-variable costs, also known as mixed costs, consist of both fixed and variable components. A portion of the cost remains constant regardless of production levels, while the other portion varies depending on how much is produced. This dual nature makes them slightly more complex to analyze but very important for accurate budgeting and forecasting.

These costs often exist in real business environments where expenses cannot be strictly categorized as fixed or variable. Understanding their structure helps businesses allocate costs more accurately and avoid miscalculations in financial planning or pricing decisions.

Examples:

- Electricity bills with a fixed monthly charge plus usage-based billing

- Telephone or internet plans with base fees and additional usage costs

- Maintenance agreements with fixed service fees and variable repair charges

- Equipment servicing costs that include standard contracts and extra work

Proper analysis of semi-variable costs improves cost control and financial accuracy.

4. Total Cost

Total cost refers to the complete cost incurred in producing a given level of output. It includes all fixed and variable costs combined and represents the overall financial burden of production at a specific point in time. Total cost is one of the most important metrics for evaluating business performance and profitability.

This concept helps businesses understand the full expense structure of production and is widely used in break-even analysis and pricing decisions. By analyzing total cost, companies can determine whether their current production level is financially sustainable or needs adjustment.

Formula: Total Cost = Fixed Costs + Variable Costs

Total cost is essential for comparing profitability across different production volumes and identifying optimal output levels.

5. Marginal Cost

Marginal cost is the additional cost incurred when producing one extra unit of output. It measures how total cost changes when production is slightly increased and is a key concept in decision-making for pricing, production scaling, and profitability optimization.

Businesses use marginal cost to determine whether producing additional units is financially beneficial. If the revenue from an additional unit is higher than its marginal cost, production can be expanded profitably. This makes marginal cost a critical tool in short-term production strategy and operational efficiency.

Example (conceptual):

- The cost difference between producing 100 units and 101 units

- Incremental expenses incurred due to increased production activity

- Additional resource usage required for one more unit

Understanding marginal cost helps businesses avoid overproduction or underutilization of resources.

6. Average Cost

Average cost refers to the cost per unit of output produced. It is calculated by dividing the total cost by the number of units produced. This measure helps businesses evaluate how efficiently resources are being used across the entire production process and is essential for pricing and competitiveness analysis.

Average cost is particularly useful for comparing production efficiency at different output levels. As production increases, average cost may decrease due to economies of scale, or increase due to inefficiencies. This makes it a key indicator of operational performance and cost management effectiveness.

Formula: Average Cost = Total Cost ÷ Number of Units Produced

Businesses use average cost to set pricing strategies and ensure products are sold at profitable margins.

7. Opportunity Cost

Opportunity cost is the value of the next best alternative that is foregone when a business makes a decision. Unlike direct costs, it is not recorded in financial statements but plays a crucial role in strategic decision-making. It represents what a business sacrifices when it chooses one option over another.

This concept helps businesses evaluate trade-offs and make more informed choices about resource allocation. Opportunity cost is especially important when resources such as capital, labor, or time are limited, as it ensures that decisions are made in favor of the most beneficial alternative.

Example (conceptual):

- Choosing to invest in one product line instead of another

- Allocating production capacity to one project and missing potential gains from another

- Using limited resources in a way that excludes alternative profitable opportunities

Understanding opportunity cost helps businesses maximize long-term value and avoid inefficient decisions.

8. Direct Costs

Direct costs are expenses that can be directly traced to the production of a specific product or service. These costs are clearly identifiable and vary depending on what is being produced. They form an essential part of product costing because they directly impact the cost of each unit produced.

Direct costs are important for determining product-level profitability since they allow businesses to see exactly how much is spent on creating a specific output. They are often used in cost accounting to allocate expenses accurately across products or projects.

Examples (conceptual):

- Costs directly associated with manufacturing a specific product

- Expenses tied to individual production batches or units

- Inputs that can be directly measured per product

- Costs that vary clearly with product output

Direct costs help businesses track profitability at the product level.

9. Indirect Costs (Overheads)

Indirect costs, also known as overheads, are expenses that support the overall production process but cannot be directly traced to a specific product. These costs are necessary for running operations smoothly but are shared across multiple products or departments.

Indirect costs are important for understanding the full cost structure of a business. Since they cannot be assigned to a single unit, they are allocated proportionally, which makes accurate cost distribution essential for financial planning and pricing decisions.

Examples (conceptual):

- Expenses supporting overall production operations

- Shared administrative and facility-related costs

- Costs that benefit multiple products simultaneously

- General operational expenses not tied to a single unit

Indirect costs ensure smooth business operations and infrastructure support.

Importance of Calculating Cost of Production

Calculating the cost of production is a fundamental aspect of business management that directly impacts profitability, pricing, and long-term sustainability. It provides a clear picture of how much is being spent to manufacture goods or deliver services, enabling businesses to make informed financial and operational decisions.

Without accurate cost calculation, companies risk poor pricing strategies, inefficient resource use, and reduced profit margins.

1. Helps in Pricing Decisions

One of the most important uses of calculating the cost of production is in setting the right selling price. Businesses must ensure that the selling price covers all production expenses while also generating a reasonable profit.

If costs are not properly calculated, companies may underprice their products and suffer losses or overprice them and lose customers. Accurate cost data allows businesses to position their products competitively in the market while maintaining profitability.

2. Assists in Profit Calculation

Cost of production plays a direct role in determining a company’s profitability. By comparing total production costs with revenue generated from sales, businesses can easily calculate profit or loss. This helps organizations evaluate financial performance over time and identify which products or services are most profitable. It also supports financial reporting and ensures transparency in business accounting, making it easier to track growth and sustainability.

3. Supports Budget Planning

Accurate calculation of production costs helps businesses prepare realistic budgets. When companies understand how much is spent on various production elements, they can allocate resources more efficiently and plan future expenditures effectively.

This leads to better financial discipline and reduces unnecessary spending. Budgeting based on production cost data also helps businesses prepare for fluctuations in demand, material prices, and operational expenses.

4. Improves Cost Control and Efficiency

Tracking the cost of production enables businesses to identify areas where expenses can be reduced or optimized. It helps detect inefficiencies such as wastage of raw materials, excessive labor costs, or high overhead expenses.

By analyzing these factors, companies can implement cost-saving measures and improve operational efficiency. Over time, this leads to better resource utilization and higher profitability.

5. Aids in Strategic Decision-Making

Cost of production is a key input for managerial decision-making. Business leaders rely on cost data to decide whether to expand production, discontinue a product, outsource operations, or invest in new technology.

It also helps evaluate whether a product is financially viable in the long run. With accurate cost information, companies can make strategic decisions that align with market conditions and business goals.

6. Helps in Financial Planning and Stability

Understanding production costs supports long-term financial planning by providing insights into fixed and variable expenses. This allows businesses to forecast future costs, manage cash flow, and maintain financial stability.

It also helps organizations prepare for economic changes such as inflation, rising material costs, or changes in demand, ensuring they remain resilient in competitive markets.

7. Enhances Business Competitiveness

Businesses that accurately calculate and manage their production costs are better positioned in the market. Lower production costs allow companies to offer competitive pricing without sacrificing profitability.

It also enables continuous improvement in operations, leading to higher efficiency and stronger market performance. In the long run, effective cost management becomes a key competitive advantage.

How to Calculate Cost of Production

Calculating the cost of production is a crucial part of financial management that helps businesses understand how much it actually costs to manufacture goods or deliver services. It involves identifying all expenses related to production and using structured formulas to evaluate total cost, unit cost, and efficiency.

Accurate calculation supports better pricing, budgeting, and profitability analysis, helping businesses make informed and strategic decisions.

1. Calculation of Total Cost

Total cost represents the complete expenditure incurred in the production process. It includes both direct and indirect expenses such as materials, labor, overheads, and other production-related costs. This calculation gives businesses a clear overview of the total financial investment required to produce goods or services within a specific time period.

Formula: Total Cost = Direct Costs + Indirect Costs

Example: A bakery produces cakes in a month. Its direct costs include ingredients like flour, sugar, eggs, and wages of bakers. Indirect costs include electricity, shop rent, and equipment maintenance. If direct costs are ₹80,000 and indirect costs are ₹40,000, then:

Total Cost = ₹80,000 + ₹40,000 = ₹1,20,000

This helps the bakery understand its total monthly production expense.

2. Unit Cost (Cost per Unit) Calculation

Unit cost shows how much it costs to produce a single unit of a product. It is derived by dividing the total cost by the number of units produced. This is essential for pricing decisions, as businesses need to ensure each unit is sold above its production cost to earn profit.

Formula: Unit Cost = Total Cost ÷ Number of Units Produced

Example: A small soap manufacturer spends ₹1,50,000 to produce 5,000 soap bars in a month.

Unit Cost = ₹1,50,000 ÷ 5,000 = ₹30 per soap bar

This means each soap bar costs ₹30 to produce before adding profit margin.

3. Average Cost Calculation

Average cost is similar to unit cost but is often used to analyze cost efficiency across different production levels. It helps businesses understand whether production is becoming more efficient or expensive as output changes.

Formula: Average Cost = Total Cost ÷ Total Output Units

Example: A textile unit produces 2,000 shirts at a total cost of ₹4,00,000.

Average Cost = ₹4,00,000 ÷ 2,000 = ₹200 per shirt

This helps the company evaluate whether scaling production is reducing or increasing per-unit cost.

4. Marginal Cost Calculation

Marginal cost measures the additional cost incurred when producing one extra unit of output. It is useful for short-term decision-making, especially when determining whether increasing production is profitable.

Formula: Marginal Cost = Total Cost of (n units) – Total Cost of (n−1 units)

Example: A furniture company spends ₹10,00,000 to produce 100 chairs and ₹10,08,000 to produce 101 chairs.

Marginal Cost = ₹10,08,000 – ₹10,00,000 = ₹8,000

This shows the cost of producing one additional chair.

5. Standard Cost Calculation

Standard costing involves setting a benchmark cost for materials, labor, and overheads, and then comparing it with actual costs. This helps businesses identify variances and control inefficiencies in production.

Formula: Cost Variance = Actual Cost – Standard Cost

Example: A garment factory sets a standard cost of ₹500 per shirt, but actual production cost comes out to ₹520.

Variance = ₹520 – ₹500 = ₹20 (unfavorable variance)

This indicates higher-than-expected production costs that need investigation.

6. Absorption Costing Method

Absorption costing allocates all production costs—both fixed and variable—to each unit produced. It gives a complete picture of the total cost per unit, which is important for external reporting and pricing decisions.

Formula: Absorption Cost per Unit = (Total Direct Costs + Total Overhead Costs) ÷ Number of Units Produced

Example: A toy manufacturer incurs ₹3,00,000 in direct costs and ₹1,50,000 in overheads to produce 5,000 toys.

Absorption Cost per Unit = ₹4,50,000 ÷ 5,000 = ₹90 per toy

This reflects the full cost of each toy.

7. Activity-Based Costing (ABC) Method

Activity-Based Costing assigns costs based on the actual activities that drive production expenses. Instead of dividing costs equally, it links costs to specific processes such as machine setup, quality testing, or packaging.

Formula: Cost Allocation = (Cost of Activity ÷ Total Activity) × Activity Consumption

Example: A company spends ₹1,00,000 on machine setups for 200 setups in a month. If Product A uses 50 setups:

Cost per setup = ₹1,00,000 ÷ 200 = ₹500

Allocated cost for Product A = ₹500 × 50 = ₹25,000

This ensures more accurate cost tracking based on actual resource usage.

8. Simple Cost of Production Formula

At a basic level, cost of production can be calculated using:

Formula: Cost of Production = Fixed Costs + Variable Costs

Example: A bakery has fixed costs of ₹60,000 (rent, salaries) and variable costs of ₹90,000 (ingredients, packaging, utilities).

Cost of Production = ₹60,000 + ₹90,000 = ₹1,50,000

This gives a clear overall production cost for the period.

Calculating cost of production using different methods helps businesses understand both overall and per-unit expenses. Whether using simple formulas or advanced costing techniques like absorption or ABC costing, these calculations provide valuable insights into pricing, profitability, and operational efficiency, enabling smarter and more sustainable business decisions.

Common Mistakes to Avoid While Calculating Cost of Production

Accurate calculation of cost of production is essential for pricing, profitability, and financial planning. However, many businesses make avoidable errors that lead to incorrect cost estimation, poor decision-making, and reduced profit margins.

These mistakes often arise from incomplete data, poor cost classification, or lack of proper tracking systems. Understanding these common pitfalls helps businesses improve accuracy and maintain better financial control.

1. Ignoring Indirect Costs

One of the most common mistakes is focusing only on direct costs like raw materials and labor while ignoring indirect costs such as rent, utilities, maintenance, and administrative expenses. These overheads may not be directly linked to a single product, but they significantly impact the overall cost structure.

When indirect costs are excluded, the calculated cost of production becomes artificially low, leading to incorrect pricing decisions and reduced profitability. Proper allocation of overheads is essential for a realistic cost estimate.

2. Misclassifying Fixed and Variable Costs

Many businesses incorrectly categorize fixed and variable costs, which leads to inaccurate cost analysis. For example, treating semi-variable expenses as purely fixed or variable can distort financial planning. Fixed costs remain constant regardless of production levels, while variable costs change with output.

Misclassification affects break-even analysis, budgeting, and pricing strategies. A clear understanding of cost behavior is necessary to ensure accurate calculations and better decision-making.

3. Not Updating Costs Regularly

Production costs are not static—they change due to inflation, supplier pricing, labor rates, and market conditions. A major mistake is relying on outdated cost data for decision-making. When costs are not updated regularly, businesses may set incorrect prices or underestimate expenses.

Regular cost reviews ensure that pricing and budgeting reflect current market realities. This helps maintain profitability and prevents financial discrepancies over time.

4. Overlooking Small or Hidden Costs

Small expenses such as packaging materials, machine lubrication, transportation losses, or minor maintenance costs are often ignored during calculation. While each may seem insignificant individually, collectively they can have a major impact on total production cost.

Overlooking these hidden costs leads to underestimation of actual expenses. A detailed cost-tracking system ensures that even minor expenses are recorded and included in the final cost calculation.

5. Inaccurate Allocation of Overheads

Improper distribution of overhead costs across products is another frequent error. Businesses sometimes allocate overheads equally without considering actual resource usage. This results in some products appearing more or less profitable than they actually are.

Accurate allocation based on production time, machine usage, or activity levels is necessary for precise costing. Activity-based costing methods can help improve accuracy in overhead allocation.

6. Ignoring Wastage and Rework Costs

Many businesses fail to account for material wastage, defective products, and rework during production. These inefficiencies directly increase the cost of production but are often excluded from calculations.

Ignoring them leads to unrealistic cost estimates and weak process control. Including wastage and quality-related costs helps businesses identify inefficiencies and improve production processes.

7. Using Incorrect Production Volume Data

Another common mistake is using inaccurate or inconsistent production volume when calculating unit cost. If the number of units produced is overestimated or underestimated, the cost per unit becomes misleading. This can result in wrong pricing decisions and incorrect profitability analysis. Ensuring accurate production data is essential for reliable cost calculations.

8. Not Considering Opportunity Cost

Businesses often ignore opportunity cost while evaluating production decisions. This refers to the value of the next best alternative that is sacrificed. While it may not be a direct expense, it plays a crucial role in strategic decision-making. Ignoring opportunity cost can lead to suboptimal resource allocation and missed profit opportunities.

9. Lack of Proper Cost Tracking Systems

Relying on manual tracking or inconsistent record-keeping can lead to errors in cost calculation. Without proper systems, businesses may miss important expenses or duplicate entries. This results in unreliable cost data and poor financial decisions. Implementing structured cost tracking systems or ERP tools helps ensure accuracy, transparency, and real-time visibility into production costs.

10. Ignoring Economies of Scale

Some businesses fail to consider how production volume affects cost per unit. As production increases, fixed costs are spread over more units, reducing average cost. Ignoring this relationship can lead to incorrect assumptions about profitability at different production levels. Understanding economies of scale helps businesses optimize production planning and pricing strategies effectively.

Strategies to Reduce Cost of Production

Reducing the cost of production is essential for improving profitability, maintaining competitiveness, and ensuring long-term business sustainability.

Organizations achieve this by eliminating inefficiencies, optimizing resources, improving workflows, and adopting smarter technologies. Effective cost reduction does not mean compromising quality; instead, it focuses on maximizing output while minimizing waste and unnecessary expenses.

The following strategies provide practical and widely used approaches to reduce production costs across industries.

1. Budgeting and Financial Planning

Budgeting and financial planning are fundamental strategies for controlling production costs. By setting clear financial targets, businesses can allocate resources efficiently and monitor spending against predefined limits. This helps identify overspending early and ensures better financial discipline across departments.

A well-structured budget also allows companies to forecast expenses, plan investments, and avoid unnecessary costs. When financial planning is consistent and data-driven, it becomes easier to maintain profitability and make informed production decisions. This approach also improves accountability within teams and reduces the risk of financial mismanagement.

2. Lean Manufacturing and Process Optimization

Lean manufacturing focuses on eliminating waste in all forms, including time, materials, and effort, to improve overall efficiency. By streamlining production processes, businesses can reduce unnecessary steps, minimize downtime, and increase productivity.

Process optimization ensures that every stage of production adds value and operates at maximum efficiency. Techniques such as continuous improvement and workflow standardization help reduce variability and defects. Over time, lean practices significantly lower operational costs while improving product quality and delivery speed, making production more efficient and cost-effective.

3. Supplier and Vendor Management

Effective supplier and vendor management plays a crucial role in reducing production costs. Businesses can negotiate better pricing, secure bulk discounts, and establish long-term contracts to stabilize material costs. Building strong relationships with suppliers also improves reliability and reduces delays in the supply chain.

Additionally, comparing multiple vendors ensures competitive pricing and better service quality. When suppliers are managed strategically, companies can reduce procurement expenses, minimize risks, and maintain consistent material availability, which directly contributes to smoother and more cost-efficient production operations.

4. Inventory Management Optimization

Efficient inventory management helps reduce unnecessary storage costs and prevents capital from being locked in excess stock. Methods like just-in-time (JIT) inventory ensure materials are ordered and used only when needed, reducing holding and warehousing expenses. Proper inventory tracking also minimizes wastage due to spoilage or obsolescence.

Maintaining optimal stock levels ensures that production runs smoothly without interruptions or overstocking. With better inventory control systems, businesses can improve cash flow, reduce waste, and achieve a more balanced and cost-efficient production cycle.

5. Energy and Resource Efficiency

Energy and resource optimization is a powerful way to reduce production costs. By monitoring and minimizing energy consumption, businesses can significantly lower utility expenses such as electricity, fuel, and water usage. Investing in energy-efficient machinery and encouraging responsible usage practices among employees further enhances savings.

Regular energy audits help identify inefficiencies and areas for improvement. Reducing resource wastage not only lowers costs but also supports sustainability goals. Over time, efficient energy management contributes to lower operational expenses and improved environmental responsibility.

6. Automation and Outsourcing

Automation and outsourcing help businesses reduce labor-intensive tasks and improve productivity. Automation technologies streamline repetitive processes, reduce human error, and increase production speed. Although initial investment may be high, it leads to long-term savings in labor and operational costs.

Outsourcing non-core activities allows businesses to focus on their main production processes while reducing overhead expenses. By combining automation with strategic outsourcing, companies can achieve higher efficiency, lower production costs, and improved scalability without compromising output quality or operational control.

7. Cost Monitoring and Continuous Analysis

Regular cost monitoring and analysis help businesses identify inefficiencies and areas of overspending. By reviewing financial reports and production data, companies can track cost trends and make timely adjustments. Variance analysis helps compare actual costs with planned budgets to detect deviations early.

This continuous evaluation enables proactive decision-making and prevents cost overruns. When organizations consistently analyze costs, they can implement corrective measures quickly, improve financial control, and maintain better overall production efficiency and profitability.

8. Waste Reduction and Quality Improvement

Reducing waste and improving product quality directly lowers production costs. Minimizing defects, rework, and material wastage ensures better utilization of resources. Techniques such as quality control checks, process standardization, and root cause analysis help identify inefficiencies in production.

When waste is reduced, companies save on raw materials, labor, and time. High-quality production also reduces returns and customer complaints, further lowering costs. Over time, focusing on quality and waste reduction leads to more efficient operations and stronger financial performance.

9. Factory Layout Optimization and Process Design

Optimizing factory layout improves workflow efficiency and reduces unnecessary movement of materials and workers. A well-designed layout ensures that production processes follow a logical sequence, minimizing delays and transportation costs within the facility.

Efficient space utilization also reduces storage requirements and improves safety. When equipment and workstations are properly arranged, productivity increases, and operational time decreases. This leads to lower production cycle times and reduced labor fatigue, ultimately contributing to significant cost savings in manufacturing operations.

10. Technology Adoption and Manufacturing Systems

Modern manufacturing technologies and systems play a key role in reducing production costs. Tools such as manufacturing software improve visibility across production, inventory, and supply chain processes. Features like demand forecasting, real-time tracking, and production planning help businesses avoid overproduction and stock shortages.

Automation and data-driven decision-making reduce manual errors and improve efficiency. By integrating technology into operations, businesses can optimize resource utilization, reduce waste, and achieve better control over production costs, leading to long-term operational efficiency.

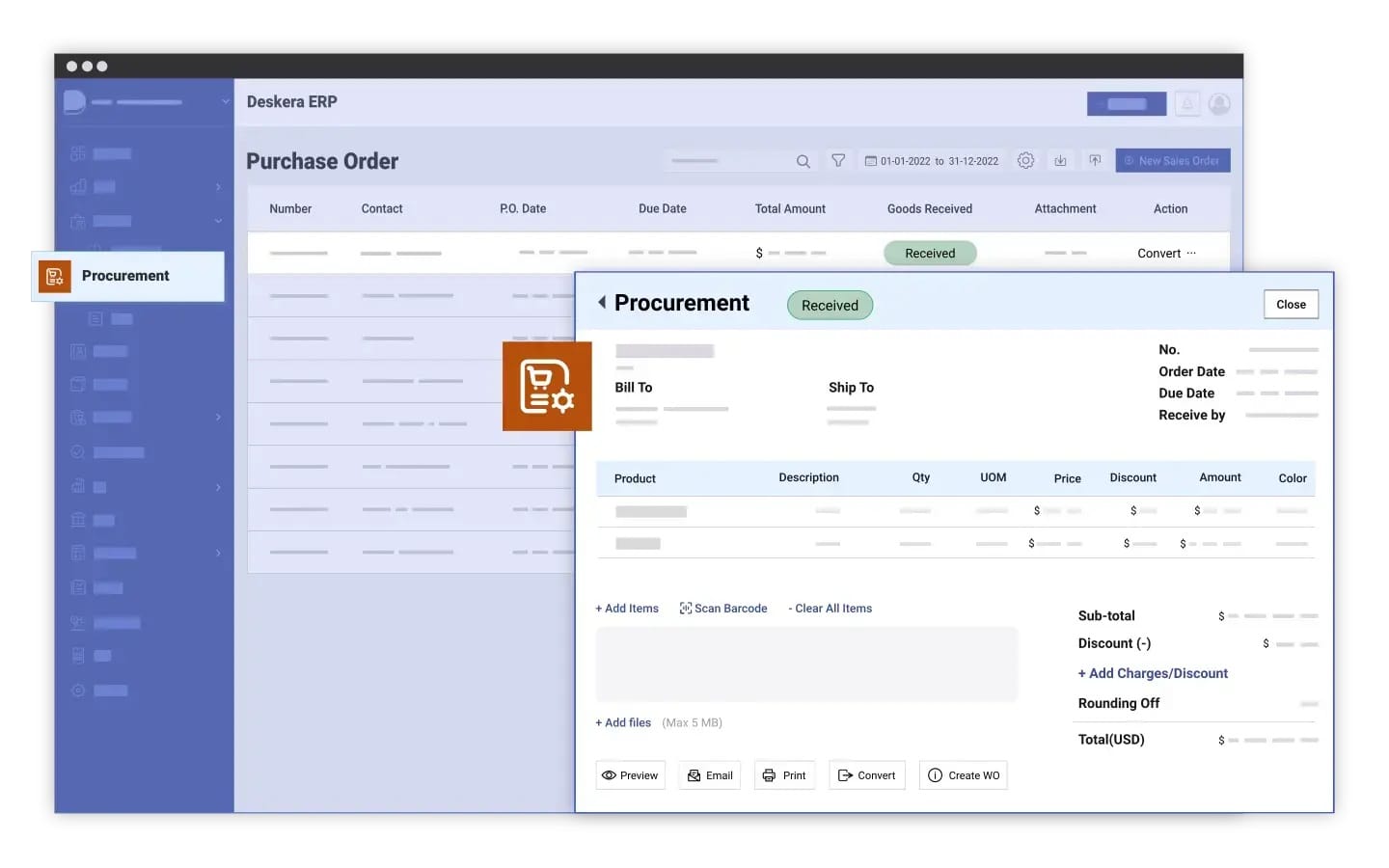

How Can Deskera Manufacturing ERP Help You Manage Cost of Production

Managing the cost of production effectively requires real-time visibility into materials, labor, overheads, and overall operational efficiency. A manufacturing ERP system like Deskera helps businesses centralize all production-related data, automate cost tracking, and improve decision-making. By integrating finance, inventory, production, and reporting into one platform, Deskera manufacturing ERP enables manufacturers to accurately calculate, monitor, and optimize their cost of production while reducing manual errors and inefficiencies.

1. Real-Time Cost Tracking and Visibility

Deskera ERP provides real-time tracking of production costs across materials, labor, and overheads. Instead of relying on manual spreadsheets, businesses can view updated cost data instantly, helping them understand where money is being spent during the production cycle. This visibility allows manufacturers to identify cost fluctuations early and take corrective actions before they impact profitability. With better transparency, decision-makers can ensure that production stays within budget and aligns with financial goals.

2. Accurate Material and Inventory Cost Control

Raw materials and inventory form a major portion of production costs, and Deskera helps optimize this through automated inventory tracking and BOM (Bill of Materials) management. The system ensures that materials are issued efficiently, wastage is minimized, and stock levels are maintained at optimal ranges. By tracking material usage in real time, businesses can avoid overstocking, stockouts, and unnecessary procurement costs, leading to more controlled and efficient production expenses.

3. Production Planning and Resource Optimization

Deskera ERP improves production planning by aligning demand forecasts with available resources. This helps businesses schedule production more efficiently and reduce idle time, machine downtime, and resource wastage. Better planning ensures that labor, machinery, and materials are used optimally, which directly reduces per-unit production costs. It also helps businesses avoid overproduction or underproduction, both of which can increase financial inefficiencies and reduce profitability.

4. Automated Cost of Goods Sold (COGS) Calculation

One of the key benefits of Deskera ERP is automated calculation of Cost of Goods Sold (COGS). The system captures all direct and indirect costs involved in production and updates financial records in real time. This eliminates manual calculations and reduces errors in cost estimation. With accurate COGS data, businesses can better understand product profitability and make informed pricing decisions that ensure healthy margins.

5. Reduction of Wastage and Production Inefficiencies

Deskera helps identify inefficiencies in the production process through detailed reporting and analytics. Businesses can track scrap rates, rework levels, and material wastage to understand where costs are increasing unnecessarily. By highlighting these inefficiencies, the ERP system enables manufacturers to implement corrective actions, improve process quality, and reduce waste. Over time, this leads to lower production costs and improved operational efficiency.

6. Better Supplier and Procurement Management

Supplier management plays a key role in controlling production costs. Deskera ERP allows businesses to manage suppliers, compare pricing, and track procurement performance from a single platform. This helps in negotiating better deals, ensuring timely delivery of materials, and reducing procurement-related delays. Strong supplier management contributes directly to cost savings and smoother production cycles.

7. Data-Driven Decision Making and Reporting

Deskera provides advanced reporting and analytics tools that give businesses insights into production performance, cost breakdowns, and profitability trends. These reports help managers make data-driven decisions regarding pricing, production scaling, and cost optimization strategies. With accurate insights, businesses can identify high-cost areas and implement targeted improvements to enhance overall financial efficiency.

8. Improved Financial Integration and Control

By integrating accounting and production data, Deskera ensures that all costs are accurately reflected in financial statements. This eliminates data silos and ensures consistency between operational and financial records. Businesses gain a clear understanding of how production activities affect overall profitability, helping them maintain stronger financial control and long-term stability.

Deskera ERP helps manufacturers manage cost of production by providing real-time visibility, automating cost calculations, improving resource planning, and reducing inefficiencies. With integrated modules for production, inventory, procurement, and accounting, it enables businesses to optimize every stage of manufacturing. This results in better cost control, higher efficiency, and improved profitability in a competitive market.

Key Takeaways

- Cost of production represents the total expenses incurred in manufacturing goods or delivering services, including direct, indirect, fixed, and variable costs. Understanding it is essential for pricing accuracy and profitability.

- Raw materials, labor, overheads, equipment, packaging, and transportation collectively form the core cost structure. Efficient management of each component helps reduce overall production expenses.

- Different cost types such as fixed, variable, semi-variable, direct, indirect, total, marginal, average, and opportunity cost help businesses analyze cost behavior and make better financial decisions.

- Demand, technology, material prices, exchange rates, taxes, and interest rates significantly influence production costs and must be monitored for effective cost control.

- Accurate cost calculation supports pricing decisions, profit analysis, budgeting, cost control, and strategic business decision-making.

- Businesses use formulas such as Total Cost = Fixed + Variable Costs and unit cost calculations to determine overall and per-unit production expenses.

- Lean manufacturing, automation, inventory optimization, supplier management, energy efficiency, and waste reduction help improve efficiency and reduce costs.

- Ignoring indirect costs, misclassifying expenses, outdated data usage, and poor overhead allocation can lead to inaccurate cost estimation and wrong decisions.

- Deskera ERP enables real-time cost tracking, accurate COGS calculation, inventory optimization, production planning, and data-driven decision-making to improve cost efficiency.

Related Articles