Ever thought what work goes behind a structured Operating Budget of a successful business? Budgeting is an important practice for small businesses since it allows them to estimate and allocate funds for various business tasks.

Preparing a budget also offers you a clear picture of the funds available to meet your objectives and ensures that you have adequate cash on hand to deal with a crisis. If you want to develop a thriving, long-term business, you'll need a precise and accurate budget. But how do you go about making one?

Let's take a look at how to make a budget for a small business in few simple steps. Following are the topics covered:

- Steps in Budgeting

- Importance of a Budget

- Small business budgets for different types of businesses

- Key takeaways

Steps in Budgeting

Budgeting for a company is a big job, which is why you might require help. Analyzing costs, forecasting revenue, and projecting cash flow are all part of the budgeting process. Having an accounting system in place will provide you with real-time financial information, allowing you to design a budget that works for you.

Examine your costs

You must first examine the running costs of your firm before beginning to develop a budget. Knowing your costs inside and out provides you with the foundation you need to create a successful budget.

If you make a rough budget and then find that you require more funds for your commercial activities, your objectives will be jeopardized. Your budget should be set up such that when your firm grows, you can increase your sales and profit enough to cover your rising expenses.

Fixed, variable, one-time, and unexpected costs should all be considered in your budget. Rent, mortgages, salaries, internet, accounting services, and insurance are all examples of fixed expenses. Cost of products sold and labour commissions are examples of variable expenses.

It's not a bad idea to overestimate the charges because you'll need enough cash to cover your future expenses. If your company is brand new, you'll also need to factor in startup expenditures. This method of budgeting will assist you in making educated decisions and avoiding financial surprises.

Tally your list of sources of income.

First and foremost. When creating a small business budget, you must first determine how much money your company generates each month and where that money comes from.

Your sales figures are a good place to start. Then, throughout the month, you can add any new sources of income for your firm.

Your business plan will determine the total amount of income sources you have.

If you run a freelance writing firm, for example, you may earn money from a variety of sources, including:

• freelance writing projects

• a writing course you offer on your website

• consulting with other writers who are establishing small businesses

Alternatively, if you own a brick-and-mortar store, you may just have one source of revenue from store sales.

Regardless of how many sources of money you have, make sure to account for any and every income that comes into your firm, and then add up all of those sources to get a clear picture of your overall monthly income.

Calculate Fixed Costs

After you've figured out your revenue, it's time to figure out your expenses, starting with fixed costs.

Any expenses that remain the same from month to month are considered fixed costs. Rent, some utilities (such as internet or phone plans), website hosting, and payroll expenditures are all examples of this.

Examine your expenses to discover which ones have remained consistent from month to month. These are the expenses that will be classified as fixed costs.

Once you've determined these expenditures, add them together to get your total fixed cost expenses for the month.

Rent, insurance, electricity, bank fees, accounting and legal services, and equipment leasing are all regular, continuous costs that don't fluctuate depending on how much money you make.

If you're just starting off and don't have any financial data to go on, use estimated costs instead. If you've signed a lease for office space, for example, utilize the monthly rent you'll be paying in the future.

Include Variable costs

Variable costs don't have a set price and fluctuate month to month depending on your company's profitability and activities. Usage-based utilities (such as electricity or gas), shipping expenses, sales commissions, and travel costs are examples of these.

By definition, variable expenses will fluctuate from month to month. You can spend more on the variables that will help your firm scale faster if your profits are larger than projected. However, if your profits are falling short of expectations, consider reducing these variable costs until you can increase your profitability.

Add up your variable expenses at the end of each month. You'll gain a feel of how these expenses change over time in relation to your business performance or during specific months, which can help you generate more accurate financial estimates and budget accordingly.

These fluctuate based on production or sales volume and are directly linked to "costs of goods sold," or anything associated to the manufacture or purchase of the product your company sells.

Raw materials, inventory, production costs, packing, and shipping are all examples of variable costs. Sales commissions, credit card fees, and travel are all examples of variable costs. A detailed budget plan lays out how much you estimate to spend on each of these expenses.

Salaries can be classified as both fixed and variable costs. Your core in-house team, for example, is typically connected with fixed costs, whereas production or manufacturing teams—anything related to the manufacture of goods—are typically classified as variable expenses. Ensure that your various salary costs are filed in the appropriate section of your budget.

You should also consider staff remuneration, which should be in line with the company's income and growth. You should also consider if you'll need to hire, how hiring will affect other parts of your budget, and what amount of experience you'll need for that individual to maximize operations.

Estimate one-time Spends

One-time charges are unrelated to your company's regular operations. These are initial costs such as office relocation, equipment, furniture, and software, as well as additional launch and research costs.

Many of your business expenses, whether fixed or variable, will be recurring costs that you pay each month. However, there are expenditures that will occur significantly less frequently. Just remember to include those costs in your budget as well.

If you know you'll have one-time expenses coming up (for example, a business course or a new laptop), including them in your budget will help you set aside the funds you'll need to cover them—and prevent your company from a huge financial setback.

In addition to adding a buffer to your budget to cover any unanticipated purchases or expenses, such as replacing a broken cell phone or engaging an IT specialist to deal with a security breach, you should also add a buffer to cover any unplanned purchases or expenses. That way, you'll be ready if an unexpected expense arises (which they always do).

Make a provision for unanticipated expenses by setting aside a contingency fund.

We all know that one-time costs don't occur when it's convenient, whether you've ran a firm previously or not. The refrigerator breaks down the day before you host your entire family for Thanksgiving. Your automobile breaks down as you're driving to the most important presentation of your career.

These expenses pop up when you least expect them, and frequently when you're on a budget. When budgeting for your business, make sure you have some extra cash on hand and plan for contingencies within your budget to avoid the worry of unforeseen spending.

Although you may be tempted to spend any extra money on variable expenses, instead put some money aside for an emergency fund. That way, you'll be prepared if equipment breaks down and needs to be replaced, or if inventory is damaged by flooding and needs to be replaced quickly. Of course, a small company loan is always an option — but having more options is preferable to having fewer.

We hope that the adage remains true for every business owner: If you budget for a crisis, the emergency never happens. What happens if an emergency arises? You've budgeted for it, after all. Isn't it true that this isn't a true emergency?

Work out a cost with suppliers

This measure will be beneficial to firms that have been in operation for more than a year and rely on suppliers to sell their products.

Before you start working on your yearly budget, talk to your suppliers and see if you can get cheaper rates on the materials, products, or services you require.

Negotiations provide you the opportunity to build trusting connections with your suppliers. This will come in handy when cash flow is scarce. You might, for example, run a seasonal business. You can pay advance amounts to your suppliers as compensation for instances when you are unable to make payments if you have adequate cash stored up. The major goal here is to figure out how to cut the cost of conducting business in half.

Estimate your revenue

Many businesses have failed in the past as a result of overestimating revenue and borrowing additional funds to meet operational requirements. This defeats the purpose of making a budget in the first place. It's a good idea to look back at previous revenue records to keep things reasonable. Revenue must be tracked on a monthly, quarterly, and annual basis by businesses.

The income figures from the prior year might be used as a benchmark for the coming year. It's critical to rely only on empirical evidence. This will assist you in setting realistic goals for your team, which will eventually lead to the expansion of your company.

This is the estimated profit from the selling of products or services. It's any money you bring in the door, regardless of how much you spend getting there. This is your budget's first line. It can be based on previous year's figures or industry averages (if you're a startup).

Your gross profit margin should be known.

The gross profit margin is the amount of money left over after all expenses have been paid at the end of the year. It provides information about your company's financial health. Here's an example of why this parameter is important to know when creating a budget.

Assume your company earned $5,000,000 in revenue, but you still owe money. Your expenses exceed your revenue at the end of the year, which is not a good indicator for a developing company. This means you must discover and remove any expenses that are not beneficial to the firm in any way. The best approach to achieve this is to list all of the materials' cost of goods sold and deduct them from the overall sales revenue. This data is required to gain a true picture of how your company is doing, allowing you to enhance profits while lowering costs.

After deducting your expenses from your earnings, your profit is what you take home. Profits are increasing, which means the company is expanding. Based on your predicted income, expenses, and cost of goods sold, this is where you'll figure out how much profit you'll make. If your profit margins (the difference between income and expenses) aren't where you'd like them to be, you should reconsider your cost of goods sold and consider raising pricing.

Alternatively, if you believe you can't squeeze any more profit margin from your company, consider increasing the Advertising and Promotions line in your budget to grow overall sales.

After you've gathered all of the aforementioned data, you'll need to put it all together to make your profit and loss statement, or P&L.

We understand that even discussing a P&L might cause anxiety. But keep in mind that you've already completed the task. It's also about addition and subtraction: Add up all of your income for the month, as well as all of your outgoings. After that, deduct the expenses from the income and hope for a favorable result.

You've made a profit if you do! If not, it's a loss — and that's fine as well. Small businesses don't make money every month, much less every year. This is especially true when your company is just getting started.

Cash flow projections

Cash flow is made up of two parts: customer payments and vendor payments. To keep your company's cash flowing, you must strike a balance between these two factors.

It's critical to have flexible payment terms and the flexibility to take payments through conventional payment channels if you want to assure timely consumer payments. Regrettably, you will have to deal with consumers who do not adhere to the agreements. Due to missed payments, this could have an impact on your cash flow estimate.

You may urge clients to pay by giving them a grace period and enforcing harsh late payment regulations. In addition, you should set aside money in your budget for 'bad debt,' in case the consumer does not pay.

You can set an amount for staff pay and travel expenses after you know your incoming cash flow. You can also set aside some funds to cover your fixed vendor costs. If you still have money left over, you can put it toward business efforts like professional development or new equipment.

All money flowing into and out of a business is referred to as cash flow. If more money comes into your organization than goes out over a certain period of time, you have positive cash flow. This is readily computed by subtracting the amount of money available at the start and end of a given time period.

Because cash flow is the lifeblood of any firm, keep track of it weekly, if not monthly. Even if you're making a lot of money, you might not have enough cash on hand to pay your suppliers.

It's critical to keep cash flow income in mind while making your annual budget. For example, you could need to buy merchandise before making sales, and you'll need to make sure you have enough cash on hand to do so. You can build a cash flow statement using your income statement and AR/P turnover rates in these situations.

Seasonal and industry trends

It's absurd to anticipate that you'll meet all of your business objectives and stick to your budget every month. There will be months in an annual cycle when your business is booming, and there may be months when sales are slow. Due to seasonal unpredictability and industry trends, you'll need to spend money wisely so that your company doesn't go out of business during slow times.

Gather information on when your firm performs best to address this difficulty when developing a budget. The goal should be to make enough money during peak months to keep the business afloat during the off-season.

Let's pretend you're the proprietor of a winter clothing company. Because your products are in high demand only during that season, the majority of your money is generated during that time. You can use the earnings to keep the firm functioning for the rest of the year and market to certain target groups, such as hikers or travelers. This will allow you to determine how successful your items are in the off-season, how much money to expect, and how much to save during peak periods.

Set spending goals

Budgeting entails more than simply totaling up your expenses and deducting them from your income. Your business's success is determined by how smartly you spend your money.

Goals provide a strategy for determining whether your money is being spent wisely and avoiding unnecessary expenses.

If you're spending money on stationary that's not being utilized for operational or marketing purposes, for example, it might be time to cut back. This money may be put to better use in your marketing activities, which would result in more leads and income. Determine which expenses will benefit your company in the long run and invest in them.

Future business budget plan

Projecting what will happen to your firm in the future, whether you're a new business or have been in operation for a long, is informed speculation. If you've been in business for a time, you'll find that your estimations are more accurate (as you might, well, guess).

It's time to build your budget now that you've completed your P&L, which is a historical document that shows your company's prior performance. And this is a document that looks to the future.

Referencing your P&L for this phase will help you better understand your business's seasonal ups and downs, which investments are worth repeating, and which you should avoid in the future.

Look for the following trends in your P&L:

• Large supply or equipment acquisitions that result in a net profit.

• Weather-related, natural-disaster-related, or economic-disaster-related seasonal trends.

• Seasonal patterns resulting from school calendars, tourist travel patterns, or supply constraints.

• Profit that is higher than in past years or that is difficult to explain.

When you examine your P&L, you're looking for explanations for your company's variations and changes.

If you run a lemonade stand, for example, you'll make more money in the summer when the weather is pleasant and the kids are out of school. Knowing your most profitable months will assist you in forecasting your upcoming year.

You may use that knowledge to hire additional people and extend your hours during specific seasons of the year, increasing your profits during the months when demand is highest.

A budget calculator

When it comes to business budget planning, a budget calculator can help you know exactly where you are. It may seem self-evident, but compiling all of your budget's figures into a single, easy-to-understand summary is quite beneficial.

Create a summary page in your spreadsheet with a row for each of the budget categories listed above. This is the foundation of your budget.

Then write the total amount you've budgeted next to each category. Finally, add a new column on the right, and use it to record the actual amounts spent in each category at the end of the time period. This gives you a quick snapshot of your budget without having to dig through layers of cluttered spreadsheets.

Check out the sample template below.

Connect the sums on the summary page to the amounts in your other budget tabs. As a result, if you change any data, your budget summary is updated as well. As a result, you now have your own budget calculator.

Bring everything together

It's time to establish your budget after you've gathered all of the information from the previous steps. After you've deducted your fixed and variable expenses from your income, you'll have a good notion of how much money you have.

Be ready to deal with any unexpected one-time charges that may arise. You can next figure out how to put the money to good use in order to attain your short- and long-term objectives.

You can use your annual budget to examine your monthly revenue and expenditures by dividing it by the 12 months of the year. Compare your monthly financial statements to the budget every time you review them to obtain a clearer idea of how close your estimates were. This can help you stay on track with your spending while also allowing you to establish a more accurate annual budget in the future.

Importance of a Budget

A business budget, in particular, can benefit your company by:

• Increasing its efficiency.

• Obtain finance to expand your company. You'll need to present a detailed budget that outlines your income and expenses if you want to seek for a business loan or raise money from investors.

• Identifying funds that are available for reinvestment.

• Make wise financial choices. Your business budget serves as a financial road map in many ways. It assists you in determining where your company's finances stand right now—and what you need to do to meet your financial objectives in the future.

• Predicting slow months so you don't go into debt.

• Calculating how long it will take to break even.

• Offering a glimpse into the future.

• Assisting you in maintaining business control.

• Making a business budget will make it easier and more effective to run your company. A company budget can also help you keep out of debt by ensuring that you spend money in the appropriate locations and at the right times.

• Determine where you can save money or increase revenue. Your business budget can help you find areas where you can cut costs or boost revenue, increasing your profits in the process.

• Estimate how much money you expect to make

• Plan how you'll spend that money

• Examine the gap between your expectations and reality

Small business budgets for different types of businesses

While every effective budget follows the same structure, you'll need to consider the budgeting oddities specific to your industry and business.

Businesses that operate only during certain seasons

Budgeting is especially vital if your firm has a busy season and a slack season.

A budget gives you a good perspective of past and present data to estimate future cash flow because your firm isn't consistent every month. This method of forecasting allows you to recognize annual trends, determine how much money you'll need to get through the slow months, and seek for cost-cutting options to counteract the low season.

You can utilize your downtime to prepare for the coming year, negotiate with vendors, and engage customers to establish loyalty.

However, don't expect the same thing to happen every year. Forecasting, like any other budget, is a dynamic process. So start with what you know, and if you don't, make the best assumption you can. It's preferable to put money aside for an emergency that never occurs than to be caught off guard.

Businesses that provide services

Focus on predicted sales, income, salaries, and consultant costs if you don't have a physical product. Budgets in these areas, whether accounting, legal services, creative, or insurance, must be flexible due to the wide range of figures. These statistics are based on the number of employees needed to offer the service, the cost of their time, and the variable demand from customers.

Businesses that specialize in custom orders

Consider labor time, as well as the cost of operations and supplies, while making custom-ordered goods. Because these differ from order to order, make an educated guess.

E-commerce businesses

Shipping is the most important budgeting factor in e-commerce. Shipping expenses (as well as possible import duties) might have a significant influence.

Do you have enough money in your budget to cover client shipping? If so, do you have a cost-effective alternative strategy in mind, such as flat-rate shipping or real-time shipping quotations for customers? Shipping rates are affected by packaging, so keep that in mind when calculating your cost of products sold. Consider any overseas warehousing expenses and tariffs while you're at it.

You'll also want to provide your customers with the finest online shopping experience possible, so pay for a solid web hosting service, web design, product photography, advertising, blogging, and social networking.

Businesses that deal with inventory

Add this to your cost of goods sold if you need to stock up on inventory to satisfy demand.

Take a best guess at the amount of inventory you'll require based on past year's sales or industry benchmarks. A little research ahead of time helps guarantee you're getting the best pricing from your vendors and sending the proper amount to meet demand, reduce shipping costs, and stay inside your budget.

The amount of inventory you have may have an impact on your pricing. If you order additional stock, for example, your cost per unit will be lower, but your total cost will be greater. Make sure this is taken into account in your budget and pricing, and that the quantity ordered does not exceed the real demand for the product.

You may also need to factor in the expense of storage or the disposal of any leftover inventory.

Startups

Budgeting can be difficult for startups because there is rarely an existing model to employ. Research industry benchmarks for salaries, rent, and marketing costs as part of your due diligence. Inquire with your network about professional fees, benefits, and equipment costs. Set aside a percentage of your money for advisors, such as accountants and lawyers. Investing a few thousand dollars up front could save you tens of thousands of dollars in legal fees and inefficiencies down the road.

This is only the tip of the iceberg; there's a lot more to think about when putting up a startup budget. This The Balance company launch budget guide is an excellent place to start.

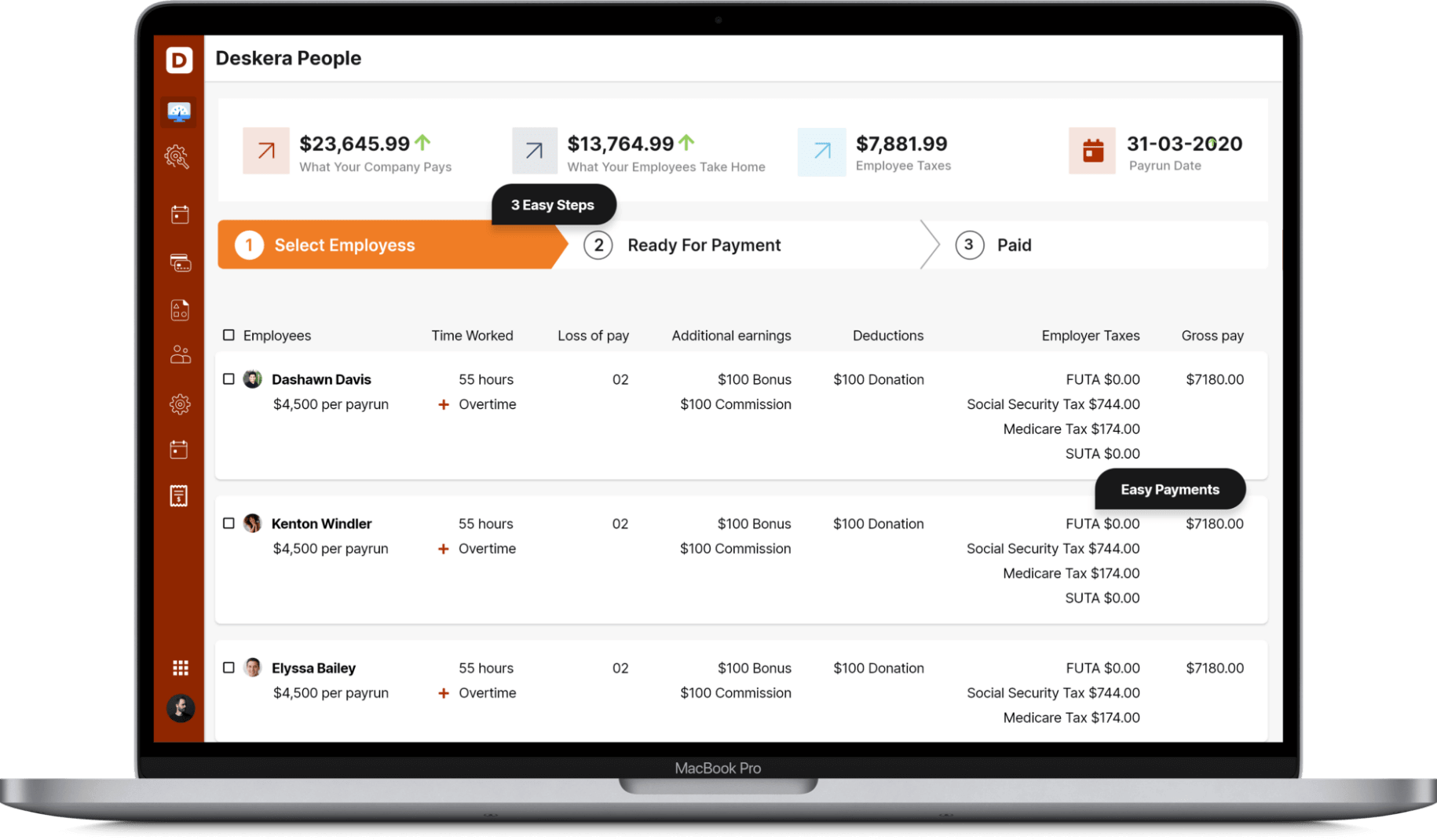

How Deskera Can help You?

Deskera People provides all the employee's essential information at a glance with the employee grid. With sorting options embedded in each column of the grid, it is easier to get the information you want.

Key takeaways

• When you're first starting out in business, it's easy to let budgeting slip between the cracks. It may not seem necessary to prepare a business budget if your company makes a lot of money or is experiencing a period of growth.

• You should create realistic goals for yourself. They should be solely dependent on your company's spending and saving capacity. Following these steps will help you develop an effective, watertight budget once you've established your goals.

• It might be difficult for small firms to forecast for the entire year because the early stages of a company's growth are often erratic. In such cases, you can create smaller budget estimates for two or three months at a time and review them frequently for better results.

Related articles