Are you trying to navigate through the complex world of project accounting? If yes, then you are on the right page.

In today's rapidly evolving business landscape, effective project management and financial oversight have become essential components for organizations aiming to stay competitive and achieve their goals. Navigating the complex world of project accounting is a critical endeavor that requires a deep understanding of not only financial principles but also the intricacies of project lifecycles, resource allocation, risk management, and compliance.

Project accounting goes beyond traditional financial tracking, offering a comprehensive framework that allows businesses to capture, analyze, and optimize the financial aspects of individual projects. From initial budgeting and resource allocation to ongoing monitoring and post-project evaluation, project accounting provides the insights necessary to make informed decisions, manage costs, and ensure projects are executed efficiently.

However, this endeavor is not without its challenges. The multifaceted nature of project accounting demands a nuanced approach that considers various factors, including project scope changes, unforeseen expenses, resource fluctuations, and regulatory requirements. Moreover, as organizations increasingly engage in diverse and global projects, the complexity intensifies, requiring a sophisticated understanding of international accounting standards, tax implications, and currency conversions.

Throughout this journey of navigating project accounting, professionals are tasked with aligning financial goals with strategic objectives, fostering collaboration between project teams and finance departments, and implementing robust software solutions that enable accurate tracking and reporting. As technology continues to advance, leveraging automation and data analytics becomes crucial to streamline processes, enhance accuracy, and extract actionable insights from financial data.

The topics covered in this article are:

- What is Project Accounting?

- Objectives of Project Accounting

- 8 Main Principles of Project Accounting

- Project Accounting Vs. Financial Accounting

- Why is Project Accounting also known as Project Cost Accounting?

- How Does Project Accounting Work?

- Project Accounting Revenue Recognition Methods

- What are the Functions of Project Accounting?

- Navigating the Complex World of Project Accounting

- Challenges Associated with Project Accounting

- Benefits of Project Accounting

- When to Use Project Accounting?

- Best Practices and Tips for Successful Project Accounting

- What to Include in a Project Accounting Annual Report?

- What is a Project Accountant?

- How to Learn Project Accounting?

- Emerging Trends of Project Accounting

- What is Project Accounting Software?

- How to Buy Project Accounting Software?

- How can Deskera Help You with Project Accounting?

- Key Takeaways

- Related Articles

What is Project Accounting?

Project accounting is a specialized accounting method used to track and manage the financial aspects of individual projects within an organization. Unlike traditional financial accounting, which focuses on the overall financial health of a business, project accounting zooms in on the financial performance of specific projects or initiatives.

Key features of project accounting include:

- Budgeting and Planning: Project accounting involves creating detailed budgets for each project, outlining the expected costs and revenue. This initial budget serves as a benchmark for measuring project performance.

- Resource Allocation: It tracks the allocation of resources such as manpower, materials, and equipment to each project. This helps ensure that resources are utilized efficiently and effectively.

- Cost Tracking: Project accounting monitors actual costs incurred during the project's execution. This includes not only direct costs like salaries and materials but also indirect costs like overhead and administrative expenses.

- Revenue Recognition: For projects that generate revenue, project accounting determines when and how to recognize that revenue based on project milestones or other criteria.

- Time Tracking: It involves tracking the time spent by employees and contractors on specific projects. This information can be crucial for accurate cost allocation and project evaluation.

- Risk Management: Project accounting considers potential risks and uncertainties that could impact project financials. This can include factors like scope changes, market fluctuations, and regulatory changes.

- Performance Analysis: Throughout the project's lifecycle, project accounting compares actual financial data against the budgeted amounts. This analysis provides insights into the project's financial health and helps identify areas for improvement.

- Reporting: Project accounting generates various reports to communicate the project's financial status to stakeholders. These reports might include project financial summaries, variance analysis, and profitability assessments.

- Compliance: Depending on the industry and location, projects might need to adhere to specific accounting standards, tax regulations, and other compliance requirements. Project accounting ensures that these are met.

- Post-Project Evaluation: After a project is completed, project accounting evaluates the actual financial outcomes against the initial projections. This retrospective analysis aids in refining future budgeting and decision-making processes.

Project accounting is particularly valuable in industries where projects are diverse, complex, and have distinct financial requirements. Examples include construction, engineering, consulting, software development, and manufacturing.

By implementing effective project accounting practices, organizations can enhance their ability to manage costs, optimize resource allocation, and make well-informed strategic decisions on a project-by-project basis.

Objectives of Project Accounting

The objectives of project accounting are centered around effectively managing and controlling the financial aspects of individual projects within an organization. These objectives are designed to ensure that projects are executed efficiently, remain financially viable, and contribute to the overall success of the organization.

Here are the key objectives of project accounting:

- Accurate Budgeting and Planning: The primary objective of project accounting is to create accurate and realistic budgets for each project. This involves estimating all costs associated with the project, from labor and materials to overhead and indirect expenses. Accurate budgeting sets the foundation for financial management throughout the project's lifecycle.

- Effective Cost Management: Project accounting aims to track and manage project costs in real-time. This includes monitoring both direct and indirect costs, identifying cost overruns, and taking corrective actions to keep costs within the allocated budget.

- Resource Allocation: Efficiently allocating resources such as manpower, equipment, and materials is a crucial objective. Project accounting ensures that resources are distributed optimally to achieve project goals while minimizing waste.

- Timely Revenue Recognition: For projects that generate revenue, project accounting ensures that revenue is recognized at the appropriate times, often tied to project milestones or completion stages. This objective contributes to accurate financial reporting and revenue forecasting.

- Risk Management: Identifying and managing project risks is essential to project success. Project accounting helps assess financial risks associated with cost overruns, scope changes, and other factors that could impact the project's financial health.

- Accurate Performance Measurement: Project accounting compares actual project financial performance against the budgeted amounts. This allows project managers and stakeholders to assess how well the project is progressing financially and make informed decisions based on the data.

- Compliance and Regulatory Adherence: Projects often need to adhere to specific accounting standards, tax regulations, and industry-specific compliance requirements. Project accounting ensures that the project's financial activities align with these regulations.

- Transparent Reporting: Transparent and accurate reporting of project financials is vital for stakeholders, including project sponsors, investors, and senior management. Project accounting generates reports that provide insights into the project's financial status and progress.

- Informed Decision-Making: The financial data collected and analyzed by project accounting supports informed decision-making throughout the project lifecycle. This includes decisions related to scope changes, resource allocation, risk mitigation, and project continuation.

- Continuous Improvement: Post-project evaluation and analysis are key objectives of project accounting. By assessing actual outcomes against initial projections, organizations can identify lessons learned and areas for improvement in future projects.

- Enhanced Profitability: Ultimately, the objective of project accounting is to contribute to the organization's profitability by ensuring that projects are completed within budget, revenue is maximized, and costs are effectively managed.

- Variance Analysis and Decision-Making: Analyze variances between budgeted and actual costs and revenues. Use variance analysis to make informed decisions, identify areas for improvement, and adjust project strategies as needed.

- Integration with Organizational Systems: Integrate project accounting data with the organization's overall financial systems for comprehensive reporting and analysis. Ensure consistency between project-specific financial records and the organization's financial records.

- Efficient Project Evaluation: Evaluate the success of each project by analyzing financial performance and comparing it to project goals. Determine whether the project achieved its objectives and contributed to the organization's strategic goals.

By fulfilling these objectives, project accounting plays a critical role in aligning financial goals with project outcomes, helping organizations achieve their strategic objectives and maintain a competitive edge in a complex business environment.

8 Main Principles of Project Accounting

The 8 main principles of project accounting are as follows:

Cost Principle:

- This principle dictates that costs should be recorded based on their actual incurred amount. It requires accuracy and transparency in reporting expenses related to a project.

- Costs should be properly classified as direct costs (specifically tied to the project) or indirect costs (shared among multiple projects or overhead).

Matching Principle:

- The matching principle suggests that expenses should be matched with the revenues they help generate. In the context of project accounting, this means that costs should be recognized in the same accounting period as the revenue they contribute to.

- For example, if a project generates revenue over several months, the associated costs incurred in those months should be recognized alongside the revenue.

Consolidation Principle:

- The consolidation principle pertains to combining financial information from various sources or business units to create a comprehensive view of an organization's financial health.

- In project accounting, this might involve consolidating financial data from different projects to understand the overall performance of the organization's project portfolio.

Full Disclosure Principle:

- The full disclosure principle requires organizations to provide all relevant and necessary information in their financial statements and reports to ensure transparency.

- In project accounting, full disclosure would involve including detailed information about project costs, revenues, risks, and uncertainties in financial reports.

Prudence Principle (Conservatism):

- The prudence principle suggests that when faced with uncertainty, accountants should exercise caution and conservatism in financial reporting.

- In project accounting, this means being cautious when estimating revenues and recognizing them only when they are reasonably assured.

Liability Principle:

- The liability principle involves recognizing liabilities (debts or obligations) when they are incurred, regardless of when the actual payment is made.

- In project accounting, this applies to recording liabilities related to project costs (such as salaries, materials, and subcontractor fees) when these obligations arise.

Control Principle:

- The control principle emphasizes the importance of having proper controls in place to ensure accurate financial reporting and prevent errors, fraud, or mismanagement.

- In project accounting, having controls over time and expense tracking, resource allocation, and cost monitoring helps maintain the integrity of financial data.

Resource Allocation Principle:

- This principle centers on allocating resources (such as labor, materials, and equipment) efficiently to achieve project goals while staying within budget.

- Resource allocation involves determining the optimal distribution of resources to different project tasks or work packages.

Each of these principles guides project accountants in maintaining accurate financial records, making informed decisions, ensuring transparency, and adhering to accounting standards and regulations. Applying these principles helps organizations manage projects effectively and report their financial performance accurately.

Project Accounting Vs. Financial Accounting

Project accounting and financial accounting are two distinct branches of accounting that serve different purposes within an organization. Let's compare these two types of accounting:

1. Focus:

- Financial Accounting:

- Focuses on recording, summarizing, and reporting the financial transactions of an entire organization as a whole.

- Provides information to external stakeholders such as investors, creditors, regulators, and the general public.

- Emphasizes producing general-purpose financial statements like the balance sheet, income statement, and cash flow statement.

- Project Accounting:

- Focuses on tracking and managing the financial aspects of individual projects or jobs within the organization.

- Provides detailed insights into project-specific costs, revenues, and profitability.

- Primarily serves internal stakeholders such as project managers, executives, and those responsible for project resource allocation.

2. Time Frame:

- Financial Accounting:

- Operates on a regular reporting schedule (quarterly and annually) to provide an overview of the organization's financial health over a specific period.

- Emphasizes historical financial data.

- Project Accounting:

- Operates on a project-based timeline, tracking financial data throughout the lifecycle of each project.

- Focuses on current and forward-looking financial data specific to each project.

3. Purpose:

- Financial Accounting:

- Aims to provide a comprehensive view of an organization's financial position and performance for decision-making by external parties.

- Focuses on overall profitability, liquidity, solvency, and compliance.

- Project Accounting:

- Aims to manage and control the financial aspects of projects to ensure project success, cost control, and optimal resource utilization.

- Focuses on project-specific profitability, costs, budget adherence, and timely completion.

4. Users:

- Financial Accounting:

- Information is primarily used by external stakeholders, including investors, creditors, analysts, regulators, and tax authorities.

- Project Accounting:

- Information is mainly used by internal stakeholders such as project managers, executives, and teams responsible for project management.

5. Reporting:

- Financial Accounting:

- Produces standardized financial statements that follow generally accepted accounting principles (GAAP) or international financial reporting standards (IFRS).

- Emphasizes adherence to accounting regulations for external reporting.

- Project Accounting:

- Produces project-specific reports and analyses tailored to the needs of project managers and internal decision-makers.

- Emphasizes project-specific data and metrics.

6. Regulatory Requirements:

- Financial Accounting:

- Subject to various regulations and standards that dictate how financial information is reported to external stakeholders.

- Project Accounting:

- While it should adhere to accounting principles, project accounting is more internally focused and flexible in terms of reporting formats.

In summary, financial accounting provides a broader overview of an organization's financial health for external stakeholders, while project accounting focuses on managing the financial aspects of individual projects to ensure their success and optimal resource utilization. Both types of accounting play crucial roles in helping organizations make informed decisions and maintain financial control.

Why is Project Accounting also known as Project Cost Accounting?

Project accounting is sometimes referred to as "project cost accounting" because one of its primary focuses is on tracking and managing the costs associated with individual projects.

While project accounting encompasses a broader range of financial aspects related to projects, including revenue recognition, resource allocation, and performance analysis, the term "project cost accounting" highlights the significant role that cost management plays within this framework.

Here are a few reasons why project accounting is often referred to as project cost accounting:

- Cost Emphasis: The term "cost accounting" underscores the importance of accurately tracking and managing project costs. This includes monitoring direct costs like labor, materials, and equipment, as well as indirect costs like overhead and administrative expenses. Understanding and controlling costs is critical for ensuring the financial viability of a project.

- Precision in Resource Allocation: A major aspect of project accounting is allocating resources efficiently to achieve project objectives. The term "cost accounting" emphasizes the need to allocate resources in a way that minimizes unnecessary expenditures and maximizes project value.

- Financial Control and Analysis: The term "cost accounting" highlights the control and analysis of project costs, which involves comparing actual costs against budgeted costs, identifying cost overruns or savings, and making adjustments as needed to stay on track financially.

- Decision-Making: Project cost accounting provides essential information for decision-making throughout a project's lifecycle. By focusing on costs, organizations can make informed choices regarding project scope changes, resource allocation, and project continuation.

- Accountability: The term "cost accounting" reinforces the concept of holding project teams and stakeholders accountable for managing costs effectively. This accountability is crucial for maintaining transparency and financial responsibility within projects.

It's important to note that while "project cost accounting" emphasizes the cost-related aspects of project accounting, the term doesn't capture the full scope of project accounting's responsibilities, which also include revenue recognition, time tracking, risk management, compliance, and overall financial performance analysis.

How Does Project Accounting Work?

Project accounting works by systematically tracking and managing financial information related to specific projects or jobs within an organization. It involves several key steps and processes to ensure accurate budgeting, cost tracking, revenue recognition, and reporting.

Here's a step-by-step overview of how project accounting works:

Project Initialization and Budgeting:

- Each project is assigned a unique identifier for tracking purposes.

- Project managers and accountants collaborate to create a budget that outlines expected costs and revenues for the project.

- The budget includes both direct costs (e.g., labor, materials, subcontractors) and indirect costs (e.g., overhead, administrative expenses).

Resource Allocation:

- Resources, including personnel, materials, and equipment, are allocated to the project based on the budget and project requirements.

Time and Expense Tracking:

- Employees and contractors record the time they spend on project tasks using timesheets or time-tracking software.

- Expenses related to the project, such as travel costs or equipment purchases, are also recorded.

Cost Accumulation and Allocation:

- Direct costs are accumulated and assigned to specific project tasks or work packages.

- Indirect costs are allocated to projects based on predetermined allocation methods, such as labor hours or square footage.

Revenue Recognition:

- Revenue is recognized based on project milestones or completion of specific tasks.

- Revenue recognition methods vary based on industry standards and contractual agreements.

Invoicing and Billing:

- Invoices are generated for clients based on completed project milestones or predetermined billing cycles.

- Invoices include project-specific details, such as work completed, expenses incurred, and terms of payment.

Resource Management:

- Resources are monitored to ensure efficient allocation, preventing overutilization or underutilization.

- Adjustments are made as project requirements evolve.

Risk Management:

- Financial risks are identified and assessed, such as potential cost overruns or revenue shortfalls.

- Strategies are developed to mitigate risks and prevent negative impacts on project finances.

Financial Reporting:

- Financial reports are generated at regular intervals, detailing the project's financial status.

- Reports include comparisons between actual and budgeted costs, revenue, and resource utilization.

Performance Analysis:

- Actual financial performance is compared to the budget and revenue projections. Variances are analyzed to understand reasons for deviations and identify areas for improvement.

Variance Analysis:

- Regularly comparing actual costs and revenues to the budgeted amounts to identify variances.

- Variances are analyzed to understand the reasons behind budget overruns or cost savings.

Profitability Analysis:

- Calculating the profitability of the project by subtracting total costs from recognized revenues.

- Analyzing profitability helps evaluate the success of the project and informs decision-making.

Reporting and Communication:

- Generating project-specific financial reports, such as project status reports, profitability reports, and variance analysis reports.

- Sharing reports with project managers, executives, stakeholders, and clients to provide insights into project performance.

Compliance and Documentation:

- Ensuring that project accounting practices adhere to relevant accounting standards, industry regulations, and tax requirements.

- Maintaining proper documentation of financial transactions, invoices, contracts, and other project-related records.

Continuous Monitoring and Adjustments:

- Continuously monitoring project financials, tracking progress, and making necessary adjustments to budgets and resource allocation as needed.

- Adapting to changes in project scope, unexpected costs, or shifts in priorities.

Integration with Overall Financial Systems:

- Ensuring that project accounting data is integrated with the organization's overall financial systems for accurate financial reporting and consolidation.

Decision-Making:

- Project managers and stakeholders make informed decisions based on accurate financial data and analysis.

- Decisions encompass resource allocation, scope changes, and risk mitigation.

Post-Project Evaluation:

- After project completion, an evaluation is conducted to compare actual outcomes against initial projections.

- Lessons learned are documented for future projects.

Continuous Improvement:

- Processes and practices are continuously refined based on feedback, outcomes, and best practices.

Technology and Automation:

- Project accounting software and tools automate processes, streamline workflows, and enhance accuracy.

Strategic Alignment:

- Project accounting ensures that project objectives align with the organization's strategic goals and contribute to overall success.

Project accounting often relies on specialized software or project management tools to streamline processes, automate calculations, and provide real-time insights into project financials. This approach helps organizations effectively manage multiple projects while maintaining control over costs and ensuring project profitability.

Project Accounting Revenue Recognition Methods

Project accounting uses various revenue recognition methods to determine how and when to recognize revenue for a specific project. The choice of method often depends on the nature of the project, industry standards, and contractual agreements.

Here are some common revenue recognition methods in project accounting:

Percentage of Completion Method

- This method recognizes revenue based on the percentage of work completed in relation to the total project.

- Revenue is recognized as work progresses and reaches certain milestones or stages.

- Expenses are matched with the corresponding recognized revenue.

Formula:

(Actual Costs Incurred / Total Estimated Costs) * Total Contract Revenue

Example:

- Total Contract Revenue: $100,000

- Estimated Total Costs: $60,000

- Actual Costs Incurred: $30,000

Revenue Recognition = ($30,000 / $60,000) * $100,000 = $50,000

Completed Contract Method

- Revenue is recognized only when the project is substantially complete or when the project has been delivered to the client.

- No revenue is recognized during the project's progress; it's recognized in its entirety upon completion.

- Expenses are accumulated until completion and then matched with recognized revenue.

Formula:

Revenue is recognized upon project completion or substantial completion.

Example:

- Total Contract Revenue: $100,000

- Estimated Total Costs: $60,000

- Actual Costs Incurred: $50,000

Revenue Recognition = $0 (Recognized only upon project completion)

Milestone Method

- Revenue is recognized upon achieving specific milestones or project stages, as outlined in the project contract.

- Milestones could include completion of certain tasks, delivery of specific components, or achievement of predetermined project goals.

Formula:

Revenue is recognized upon reaching specific project milestones.

Example:

- Total Contract Revenue: $100,000

- Milestone 1 Reached: $30,000 (30% completion)

- Milestone 2 Reached: $70,000 (70% completion)

Revenue Recognition = $30,000 + $70,000 = $100,000

Cost-Recovery Method

- Revenue is recognized only after project costs have been recovered.

- It's often used when uncertainty exists about the collectability of project revenues.

Formula:

Revenue is recognized after project costs are recovered.

Example:

- Total Contract Revenue: $100,000

- Total Project Costs: $80,000

- Costs Recovered: $60,000

Revenue Recognition = $0 (Recognized only after costs are fully recovered)

Percentage of Completion-Cost Recovery Hybrid Method

- Combines elements of both the percentage of completion method and the cost-recovery method.

- Revenue is recognized based on the percentage of work completed, but the method includes provisions for cost recovery before recognizing significant profit.

Formula:

Lesser of [(Actual Costs Incurred / Total Estimated Costs) * Total Contract Revenue] and [Total Contract Revenue - Costs Recovered]

Example:

- Total Contract Revenue: $100,000

- Estimated Total Costs: $60,000

- Actual Costs Incurred: $30,000

- Costs Recovered: $20,000

Revenue Recognition = Lesser of [($30,000 / $60,000) * $100,000] and [$100,000 - $20,000] = $50,000

Units of Delivery or Production Method

- Revenue is recognized based on the number of units delivered or produced in the project.

- Commonly used in manufacturing or production projects where output can be quantified.

Formula:

Revenue is recognized based on the number of units delivered or produced.

Example:

- Revenue per Unit: $10

- Units Delivered: 8

Revenue Recognition = $10 * 8 = $80

Cost-to-Cost Method

- A variation of the percentage of completion method.

- Recognizes revenue based on the ratio of costs incurred to total estimated costs.

- Useful when costs are a reliable indicator of progress.

Formula:

Recognized Revenue = Total Contract Revenue × (Actual Costs Incurred / Total Estimated Costs)

Example:

A construction project with a total contract value of $800,000 has incurred $300,000 in costs out of a total estimated cost of $600,000. The recognized revenue would be $800,000 × ($300,000 / $600,000) = $400,000.

Output Method

- Revenue is recognized based on the value of outputs delivered to the customer.

- Suitable for projects where the value of the completed deliverables drives revenue recognition.

- Often used in projects with unique or complex deliverables.

Formula:

Recognized Revenue = Value of Outputs Delivered

Example: An architectural design project involves creating detailed blueprints for a building. Upon delivering the completed blueprints, the recognized revenue is the agreed-upon value for the blueprints.

Input Method

- Revenue is recognized based on the costs incurred in relation to the total estimated costs.

- Focuses on the effort expended on the project as an indicator of progress.

- Suitable for projects where labor and other resources are primary contributors to project value.

Formula:

Recognized Revenue = Total Contract Revenue × (Actual Costs Incurred / Total Estimated Costs)

Example: A consulting project with a total contract value of $150,000 has incurred $90,000 in costs out of a total estimated cost of $120,000. The recognized revenue would be $150,000 × ($90,000 / $120,000) = $112,500.

Straight-Line Method

- Recognizes revenue evenly over the project's duration.

- Suitable for projects where the work is consistent and evenly spread out.

Formula:

Recognized Revenue = Total Contract Revenue / Number of Reporting Periods

Example: An advertising campaign project with a total contract value of $240,000 spans over 12 months. The recognized revenue for each month would be $240,000 / 12 = $20,000.

Percentage Completion of Specific Activities

- Recognizes revenue for specific activities or components within a larger project.

- Useful when different parts of the project have varying degrees of completion.

Formula:

Recognized Revenue = Total Contract Revenue × Percentage of Completion for Specific Activity

Example: A software development project has three phases. Each phase is worth 30% of the total contract value. After completing the first phase, the recognized revenue would be $100,000 × 0.30 = $30,000.

It's important to note that revenue recognition methods can have significant implications for financial reporting, profitability analysis, and even tax liabilities. The choice of method should be consistent with the organization's accounting policies, industry standards, and any regulatory requirements. Additionally, the terms of the project contract and the degree of completion and uncertainty play a key role in determining the appropriate revenue recognition method.

What are the Functions of Project Accounting?

Project accounting encompasses various functions that revolve around managing the financial aspects of individual projects within an organization. These functions are essential to ensure that projects are executed efficiently, costs are controlled, revenues are recognized accurately, and project goals are achieved.

Here are the key functions of project accounting:

Budgeting and Planning:

- Collaborating with project managers to create detailed project budgets.

- Allocating resources and funds to different project tasks and phases.

- Estimating costs and revenues for each project element.

Cost Tracking and Control:

- Monitoring and tracking project expenses in real time.

- Comparing actual costs with the budgeted amounts to identify variances.

- Taking corrective actions to control costs and prevent overruns.

Revenue Recognition:

- Applying appropriate revenue recognition methods to match revenue with project progress.

- Ensuring that revenue recognition complies with industry standards and contractual agreements.

Time and Expense Management:

- Implementing systems to track time spent by team members on project-related tasks.

- Managing and recording project-related expenses, including travel, materials, and subcontractor costs.

Invoicing and Billing:

- Generating invoices for clients based on completed project milestones or contractual terms.

- Ensuring that invoices accurately reflect work completed, expenses incurred, and agreed-upon terms.

Resource Allocation:

- Optimizing resource allocation to maximize productivity and efficiency.

- Allocating personnel, equipment, and materials to different project components.

Variance Analysis:

- Analyzing discrepancies between budgeted and actual costs and revenues.

- Identifying reasons for variances and providing insights to project managers.

Financial Reporting:

- Producing project-specific financial reports, including project status, profitability, and variance reports.

- Communicating financial information to project managers and stakeholders.

Risk Management:

- Identifying and assessing financial risks associated with projects.

- Suggesting strategies to mitigate risks and minimize their impact.

Compliance and Documentation:

- Ensuring that project accounting practices adhere to accounting standards, industry regulations, and tax requirements.

- Maintaining accurate documentation of financial transactions and project-related records.

Integration and Automation:

- Integrating project accounting data with broader financial systems for consistent reporting.

- Automating processes like data entry, time tracking, and invoicing.

Profitability Analysis:

- Evaluating the profitability of each project by comparing recognized revenue to total costs.

- Determining whether projects are meeting financial goals and contributing to the organization's overall profitability.

Decision Support:

- Providing financial insights and data to project managers and executives to support informed decision-making.

- Assisting in evaluating project feasibility, risks, and potential returns.

Project accounting functions are integral to managing the financial health of projects, ensuring accountability, and maximizing project success within the broader organizational context.

Navigating the Complex World of Project Accounting

Navigating the complex world of project accounting requires a comprehensive understanding of financial principles, project management, and industry-specific practices.

Here's a guide to help you navigate through the intricacies of project accounting:

Establish Clear Objectives:

- Define the goals and objectives of your project accounting processes. Determine what you want to achieve, whether it's cost control, accurate financial reporting, or project profitability.

Select Appropriate Software:

- Invest in project accounting software or project management tools that streamline time tracking, expense management, budgeting, and reporting.

- Ensure the software integrates with your overall financial systems for consistency.

Design Effective Processes:

- Develop efficient workflows for cost tracking, revenue recognition, and resource allocation.

- Document and communicate these processes to ensure consistency and compliance.

Understand Revenue Recognition:

- Familiarize yourself with different revenue recognition methods and choose the one that best aligns with your projects and industry standards.

Allocate Resources Wisely:

- Optimize resource allocation to ensure the right people, materials, and equipment are allocated to projects efficiently.

- Monitor resource utilization to prevent overallocation or underutilization.

Monitor Costs Closely:

- Regularly track project costs against budgets to identify any discrepancies and take corrective actions.

- Implement controls to prevent unauthorized spending.

Utilize Time and Expense Tracking:

- Implement robust time and expense tracking systems to accurately capture project-related activities and costs.

- Encourage team members to submit accurate and timely data.

Embrace Communication:

- Foster open communication between project managers, accountants, and stakeholders.

- Regularly share financial updates and reports to keep everyone informed.

Analyze Variances:

- Perform variance analysis to understand differences between budgeted and actual costs and revenues.

- Use this analysis to make informed decisions and improve future projects.

Adapt to Changes:

- Be prepared for changes in project scope, requirements, or unexpected events that might impact project finances.

- Adjust budgets and plans accordingly.

Maintain Compliance:

- Adhere to accounting standards, industry regulations, and tax requirements that apply to project accounting.

- Ensure all financial transactions and records are properly documented.

Evaluate Project Profitability:

- Regularly assess the profitability of your projects by comparing recognized revenue with total costs.

- Determine whether projects are meeting financial goals.

Continuous Learning:

- Stay updated with industry trends, new accounting regulations, and advancements in project management practices.

- Attend workshops, webinars, and training sessions to enhance your skills.

Collaboration with Project Managers:

- Collaborate closely with project managers to align financial goals with project objectives.

- Ensure accurate data exchange between project management and accounting teams.

Consult Professionals:

- If your projects are complex or involve intricate financial arrangements, consider consulting accounting experts or advisors.

Remember, project accounting is a dynamic process that requires ongoing attention and adjustment. By combining financial expertise with effective project management, you can successfully navigate the complexities of project accounting and achieve project success while maintaining financial control.

Challenges Associated with Project Accounting

Project accounting comes with its share of challenges, especially in managing complex projects and ensuring accurate financial management. Here are some common challenges associated with project accounting:

- Cost Tracking Complexity: Managing and tracking various project costs, including direct and indirect costs, can be complex and require robust systems to ensure accuracy.

- Resource Allocation: Allocating resources efficiently while preventing overutilization or underutilization can be challenging, especially in dynamic project environments.

- Accurate Budgeting: Creating accurate project budgets that encompass all potential costs and revenue streams can be difficult due to uncertainties and changing project requirements.

- Scope Changes: Managing financial implications when project scope changes can lead to challenges in adjusting budgets, timelines, and resource allocation.

- Varied Revenue Recognition: Determining the appropriate criteria for revenue recognition in projects with different deliverables, milestones, or payment structures can be intricate.

- Data Accuracy: Relying on accurate data from various sources is essential, but inconsistencies or errors in data entry can lead to inaccurate financial reporting.

- Resource Availability: Ensuring the availability of skilled personnel and necessary resources to meet project deadlines while adhering to budgets can be a juggling act.

- Complex Contracts: Projects with complex contractual agreements, involving multiple stakeholders and diverse deliverables, can complicate revenue recognition and cost allocation.

- Risk Management: Identifying, assessing, and mitigating financial risks associated with projects requires careful planning and ongoing monitoring.

- Integration with Project Management: Seamlessly integrating project accounting with project management systems to ensure that financial data accurately reflects project progress can be challenging.

- Reporting Challenges: Generating accurate and timely financial reports that provide insights into project performance and profitability can be demanding.

- Compliance and Regulations: Adhering to accounting standards, tax regulations, and industry-specific compliance requirements while managing projects can be complex.

- Cross-Functional Collaboration: Ensuring effective communication and collaboration between project managers, finance teams, and other stakeholders can be a challenge.

- Technology Adoption: Adopting and integrating new project accounting software and technologies requires training and adjustments to existing processes.

- Change Management: Implementing project accounting practices may require changes in the organization's culture and practices, which can meet resistance.

- Data Security: Ensuring the security and privacy of project financial data in an increasingly digital environment is a critical challenge.

- Performance Measurement: Effectively measuring project financial performance against benchmarks and budgeted figures requires accurate data and a comprehensive understanding of project dynamics.

While these challenges may seem daunting, they can be addressed with careful planning, the use of appropriate technologies, continuous communication, and adherence to best practices in project accounting. Overcoming these challenges can lead to more effective financial management and successful project outcomes.

Benefits of Project Accounting

Project accounting offers a range of benefits that contribute to better financial management, decision-making, and overall project success. Here are some of the key benefits of implementing project accounting:

- Accurate Financial Tracking: Project accounting provides real-time visibility into project costs, helping you track expenses accurately and prevent cost overruns.

- Cost Control: By closely monitoring project costs, project accounting enables effective cost control, ensuring that budgets are adhered to and resources are allocated efficiently.

- Informed Decision-Making: Accurate financial data from project accounting supports informed decisions about resource allocation, scope changes, and project direction.

- Resource Optimization: Project accounting helps maximize the use of resources like manpower, materials, and equipment, reducing waste and improving efficiency.

- Timely Revenue Recognition: For revenue-generating projects, project accounting ensures that revenue is recognized at appropriate milestones, leading to accurate financial reporting.

- Risk Management: Identifying and managing financial risks is easier with project accounting, enabling you to take proactive measures to mitigate potential issues.

- Transparency and Accountability: Project accounting promotes transparency by documenting all financial activities, fostering accountability among project teams and stakeholders.

- Compliance Adherence: Especially important in regulated industries, project accounting helps ensure projects adhere to accounting standards, tax regulations, and industry-specific requirements.

- Performance Evaluation: By comparing actual financial performance against budgets, project accounting aids in evaluating project success and identifying areas for improvement.

- Efficient Reporting: Project accounting generates detailed financial reports, providing stakeholders with insights into project financial health and progress.

- Strategic Alignment: Project accounting aligns project objectives with the organization's strategic goals, contributing to overall profitability and growth.

- Enhanced Forecasting: Accurate financial data collected through project accounting supports better forecasting and planning for future projects.

- Resource Accountability: Time tracking and cost allocation in project accounting hold team members accountable for their contributions to the project.

- Improved Communication: Project accounting helps communicate project financials effectively to stakeholders, ensuring everyone is on the same page.

- Efficiency and Automation: Utilizing project accounting software automates processes, reducing manual work and improving efficiency.

- Post-Project Learning: Analyzing project financial outcomes informs future projects, leading to continuous improvement and more accurate estimations.

- Competitive Edge: Effective project accounting can provide a competitive edge by enabling better cost management and financial control.

- Holistic Project Insights: Project accounting offers a comprehensive view of projects, combining financial data with other project-related information.

- Quality Risk Assessment: By identifying financial risks early, project accounting allows for better risk assessment and planning.

- Satisfied Stakeholders: Accurate and transparent financial reporting fosters trust and satisfaction among stakeholders, enhancing relationships.

Overall, project accounting empowers organizations to manage project finances with precision, make data-driven decisions, and ensure that projects contribute positively to the organization's bottom line and long-term success.

When to Use Project Accounting?

Project accounting should be used in situations where an organization is engaged in managing complex projects with significant financial implications. It is particularly relevant when projects require meticulous financial management, accurate tracking of costs and revenue, and strategic decision-making based on project-specific financial data.

Here are some scenarios when project accounting should be used:

- Diverse Projects: When an organization undertakes a variety of projects with different scopes, sizes, and financial requirements, project accounting helps manage the unique financial aspects of each project.

- Resource Allocation: Project accounting is useful when projects require efficient allocation of resources such as manpower, materials, and equipment to ensure optimal utilization and cost control.

- Cost Management: If projects have substantial budgets and expenses that need to be carefully monitored to prevent cost overruns, project accounting can provide effective cost management.

- Revenue Generation: For projects that generate revenue based on milestones, deliverables, or services provided, project accounting ensures accurate revenue recognition at the right times.

- Risk Management: When projects involve financial risks that need to be identified, assessed, and mitigated, project accounting helps manage and track these risks.

- Regulated Industries: In industries with regulatory compliance requirements, such as construction, healthcare, and government contracting, project accounting ensures adherence to accounting standards and regulatory guidelines.

- Long-Term Projects: For projects with extended durations, project accounting helps manage financial aspects over the entire project lifecycle, preventing financial surprises.

- Resource-Intensive Projects: In projects that require significant human and capital resources, project accounting assists in tracking costs and optimizing resource allocation.

- Contractual Agreements: When projects are governed by complex contractual agreements that dictate revenue recognition, billing milestones, and payment terms, project accounting ensures compliance with these terms.

- Project-Driven Organizations: Organizations that rely heavily on project-based work, such as consulting firms, engineering companies, and construction firms, benefit from project accounting to manage multiple projects simultaneously.

- Decision-Making: When financial decisions about projects need to be based on accurate and up-to-date financial data, project accounting provides the necessary insights.

- Financial Transparency: If transparency in financial reporting and accountability for project financials are priorities, project accounting helps maintain clear records of project-related expenses and revenue.

- Performance Evaluation: Organizations that want to evaluate the financial performance of projects against budgets and projections can use project accounting for accurate performance analysis.

- Auditing and Compliance: Projects that undergo audits or need to comply with accounting standards require proper documentation and adherence to revenue recognition and cost allocation guidelines.

- Enhanced Reporting: Organizations seeking detailed financial reports on project costs, revenue, and profitability can benefit from project accounting's reporting capabilities.

In essence, project accounting should be considered when the financial management of projects becomes intricate and requires specialized attention beyond the organization's regular accounting processes.

It enables accurate tracking, efficient resource allocation, informed decision-making, and compliance with accounting standards, ultimately contributing to the success of individual projects and the organization as a whole.

Best Practices and Tips for Successful Project Accounting

Implementing project accounting best practices can significantly enhance your ability to manage project finances effectively and achieve better outcomes. Here are some key tips and best practices for successful project accounting:

Comprehensive Budgeting:

- Develop detailed project budgets that include all anticipated costs and revenue.

- Account for direct costs (labor, materials) and indirect costs (overhead, administrative).

- Consider potential risks and contingencies when budgeting.

Accurate Cost Tracking:

- Implement robust systems for tracking all project-related costs in real-time.

- Regularly compare actual costs against the budgeted amounts to identify variances.

- Keep a close eye on both direct and indirect costs.

Resource Allocation Efficiency:

- Allocate resources based on project needs and timelines to optimize utilization.

- Adjust resource allocation as project requirements change.

- Monitor resource utilization to prevent overallocation or underutilization.

Timely Revenue Recognition:

- Establish clear criteria for recognizing revenue at project milestones or deliverable completions.

- Align revenue recognition with project agreements and accounting standards.

Risk Management Integration:

- Identify potential financial risks early and develop strategies to mitigate them.

- Regularly reassess risks and adjust mitigation strategies as needed.

Robust Reporting:

- Generate accurate and detailed financial reports that provide insights into the project's financial status.

- Include information on budgeted vs. actual costs, revenue, and resource utilization.

Cross-Functional Collaboration:

- Foster collaboration between project teams, finance departments, and other stakeholders.

- Ensure open communication about the financial aspects of projects.

Clear Documentation:

- Maintain clear documentation of all project-related financial activities, decisions, and agreements.

- Document any changes to the project scope, budget, or resources.

Regular Performance Analysis:

- Continuously analyze project performance against financial benchmarks.

- Identify trends and patterns in project financial data for future planning.

Software Utilization:

- Invest in project accounting software to automate processes, streamline workflows, and reduce errors.

- Choose a software solution that aligns with your organization's needs and requirements.

Adherence to Compliance:

- Ensure that all project financial activities adhere to relevant accounting standards and regulations.

- Address any industry-specific compliance requirements or tax implications.

Training and Education:

- Provide training for project managers and team members on project accounting principles and processes.

- Keep team members informed about the financial impact of their activities.

Post-Project Evaluation:

- Conduct thorough evaluations of completed projects, comparing actual outcomes to initial projections.

- Use lessons learned to refine future budgeting and decision-making.

Continuous Improvement:

- Continuously review and improve project accounting processes based on feedback and outcomes.

- Incorporate feedback from stakeholders to enhance financial management practices.

Data Security and Privacy:

- Ensure that project financial data is stored securely and accessed only by authorized personnel.

- Adhere to data protection and privacy regulations.

By following these project accounting best practices, you can establish a solid foundation for managing project finances, making informed decisions, and achieving successful project outcomes while maintaining financial control and transparency.

What to Include in a Project Accounting Annual Report?

An annual report for project accounting provides stakeholders with a comprehensive overview of a project's financial performance, accomplishments, challenges, and future outlook over the course of a year. This report serves as a valuable communication tool to keep stakeholders informed and engaged.

Here's what you should consider including in a project accounting annual report:

Executive Summary:

- Provide a concise overview of the project's purpose, key achievements, and financial highlights.

Project Overview:

- Describe the project's objectives, scope, and significance within the organization.

- Highlight any major milestones or completed deliverables.

Financial Performance:

- Present a summary of the project's financial performance over the year.

- Include data on budgeted vs. actual costs, revenue, and any significant variances.

- Provide insights into how the project's financial performance aligned with expectations.

Resource Utilization:

- Discuss how resources were allocated and utilized throughout the year.

- Highlight any improvements made in resource allocation efficiency.

Revenue Recognition:

- Detail how revenue was recognized over the course of the project.

- Explain the criteria and milestones used for recognizing revenue.

Cost Control and Management:

- Showcase efforts made to control costs and manage project expenses.

- Describe strategies implemented to prevent cost overruns.

Risk Management:

- Discuss any financial risks that were identified and managed during the year.

- Explain the impact of risk mitigation strategies on project financials.

Performance Analysis:

- Provide an analysis of the project's financial performance compared to initial projections.

- Explain any significant discrepancies and the reasons behind them.

Future Outlook:

- Discuss the project's outlook for the upcoming year.

- Highlight anticipated challenges, opportunities, and financial goals.

Lessons Learned:

- Share insights gained from the project's financial performance and management.

- Detail any lessons learned that can be applied to future projects.

Strategic Alignment:

- Explain how the project's financial performance aligns with the organization's strategic goals.

- Describe the project's contribution to the organization's overall financial health.

Transparency and Accountability:

- Highlight the transparency of financial reporting and the accountability maintained in managing project finances.

Graphs and Charts:

- Use visual representations to illustrate financial data, trends, and comparisons.

- Graphs and charts can make complex financial information easier to understand.

Acknowledgments and Appreciation:

- Recognize the contributions of project team members, stakeholders, and partners.

- Express gratitude for their support throughout the year.

Appendices:

- Include additional details such as detailed financial reports, breakdowns of costs, and any supporting documentation.

Contact Information:

- Provide contact information for project leads or finance personnel for any questions or inquiries.

Remember that the content and format of the annual report should be tailored to your organization's preferences and the specific needs of the project.

A well-structured annual report can effectively communicate the project's financial performance and provide stakeholders with a clear understanding of the project's impact and future direction.

What is a Project Accountant?

A project accountant is a financial professional who specializes in managing the financial aspects of individual projects within an organization.

Their role is to ensure that project-related financial transactions are accurately recorded, tracked, and reported, helping the organization effectively manage project costs, revenues, and profitability.

Project accountants work closely with project managers, executives, and stakeholders to provide financial insights and support throughout the project lifecycle.

Key responsibilities of a project accountant include:

Budgeting and Planning:

- Collaborating with project managers to create project budgets based on estimated costs and expected revenues.

- Allocating resources and funds to different project tasks or work packages.

Cost Tracking and Control:

- Monitoring project expenses to ensure they stay within budget.

- Identifying cost overruns and suggesting corrective actions.

Revenue Recognition:

- Applying appropriate revenue recognition methods to match revenue with project progress.

- Ensuring that recognized revenue aligns with contractual agreements and industry standards.

Time and Expense Management:

- Overseeing time and expense tracking systems to ensure accurate recording of project-related activities and costs.

- Reviewing timesheets and expense reports for accuracy and compliance.

Invoicing and Billing:

- Generating invoices for clients based on project milestones, stages, or contractual terms.

- Ensuring that invoices accurately reflect work completed and expenses incurred.

Variance Analysis:

- Analyzing differences between budgeted and actual costs, as well as comparing project performance to financial projections.

- Identifying reasons for variances and providing insights to project managers.

Financial Reporting:

- Producing project-specific financial reports and analyses for internal stakeholders.

- Communicating financial performance and trends to project teams and management.

Risk Management:

- Identifying financial risks associated with projects and suggesting strategies to mitigate them.

- Assessing the impact of risks on project financials.

Compliance and Documentation:

- Ensuring that project accounting practices adhere to accounting standards, industry regulations, and tax requirements.

- Maintaining accurate documentation of financial transactions and project-related records.

Integration with Overall Financial Systems:

- Integrating project accounting data with the organization's general financial systems for accurate reporting and consolidation.

Project accountants play a critical role in helping organizations maintain control over project finances, optimize resource utilization, and make informed decisions to ensure project success and overall financial health.

How to Learn Project Accounting?

Learning project accounting involves gaining knowledge of financial management practices specific to project-based environments. Here's a step-by-step guide to help you learn project accounting:

1. Understand Basic Accounting:- Start with a solid foundation in basic accounting principles. This includes concepts like debits and credits, financial statements, and accounting equations.

2. Study Project Management:- Familiarize yourself with project management principles, methodologies, and processes. Understanding project lifecycles, scope, scheduling, and resource management is crucial.

3. Explore Project Accounting Concepts:- Dive into project-specific accounting concepts such as revenue recognition, cost allocation, budgeting, and variance analysis.

4. Enroll in Courses:- Consider taking courses specifically focused on project accounting. Many online platforms offer courses in accounting, project management, and financial management.

5. Online Learning Platforms:- Platforms like Coursera, Udemy, LinkedIn Learning, and edX offer courses on accounting and project management. Look for courses that address project accounting topics.

6. Professional Certifications:- Explore professional certifications such as the Certified Project Accountant (CPA) certification offered by various organizations. These certifications validate your expertise in project accounting.

7. Books and Resources:- Explore textbooks, eBooks, and articles related to project accounting. Look for resources that provide practical examples and case studies.

8. Practice with Software:- Gain hands-on experience with project accounting software. Many platforms offer trial versions that allow you to explore the software's features.

9. Practical Application:- Apply your learning to real-world scenarios. If you work on projects, try implementing project accounting practices within your projects.

10. Networking: - Connect with professionals in project management and accounting fields. Join industry groups, forums, and associations to learn from others' experiences.

11. Workshops and Seminars: - Attend workshops, seminars, and webinars on project accounting. These events provide insights from experts and opportunities for networking.

12. On-the-Job Learning: - If you're working in a project-based organization, seek opportunities to collaborate with project accountants or take on responsibilities related to project financial management.

13. Mentorship: - If possible, seek mentorship from experienced project accountants. Learning from those who have practical experience can be invaluable.

14. Continuous Learning: - Project accounting is a dynamic field. Stay updated with industry trends, changes in accounting standards, and advancements in project management practices.

15. Apply Learning Gradually: - As you learn, gradually apply the principles and practices to real-world situations. Over time, your confidence and expertise will grow.

Remember that learning project accounting is an ongoing journey. It's a combination of understanding financial principles, project management concepts, and practical application. Continuous learning and practical experience will help you become proficient in effectively managing project finances.

Emerging Trends of Project Accounting

As business practices evolve and technology advances, project accounting is also subject to emerging trends that shape its practices and methodologies. Here are some of the emerging trends in project accounting:

- Technology Integration: Adoption of advanced technologies like artificial intelligence (AI) and machine learning (ML) to automate repetitive tasks, enhance data analysis, and improve accuracy in cost estimation and risk assessment.

- Cloud-Based Solutions: Increasing use of cloud-based project accounting software that enables real-time collaboration, data accessibility, and seamless integration with other systems.

- Data Analytics and Visualization: Utilization of data analytics tools to extract insights from project financial data and visualize trends, helping in better decision-making and strategic planning.

- Predictive Analytics: Implementation of predictive analytics to forecast project outcomes, identify potential issues and make proactive adjustments to mitigate risks.

- Mobile Accessibility: Mobile apps and platforms that enable project managers and team members to access and update financial data on the go, facilitating real-time decision-making.

- Integrated Project Management: Closer integration between project management and accounting systems, ensuring that financial data is aligned with project progress and vice versa.

- Agile Project Accounting: Application of agile methodologies to project accounting, allowing for flexibility in managing changing project requirements, budgets, and resource allocation.

- Blockchain for Transparency: Experimentation with blockchain technology to ensure transparency and accuracy in financial transactions, enhancing trust among project stakeholders.

- Ecosystem Collaboration: Increased collaboration among software providers, financial institutions, and project management platforms to create comprehensive ecosystems that support project accounting needs.

- Remote Work Adaptation: Adjustment of project accounting practices to accommodate remote work and distributed teams, emphasizing virtual collaboration and secure data access.

- Environmental, Social, and Governance (ESG) Reporting: Integration of ESG metrics into project accounting, considering the impact of projects on sustainability and societal factors.

- Real-Time Reporting: Emphasis on real-time reporting and dashboards that provide instant insights into project financials, enabling faster decision-making.

- Regulatory Compliance Automation: Automation of compliance-related tasks to ensure adherence to accounting standards and regulations, reducing manual efforts.

- Skills and Talent Development: Focus on upskilling project accountants to understand and leverage technology, data analytics, and financial technologies for improved practices.

- Cybersecurity Measures: Heightened attention to cybersecurity measures to protect sensitive financial data, especially as more processes are digitized.

These emerging trends in project accounting reflect the increasing integration of technology, data-driven decision-making, and the need for adaptable and responsive financial management practices in the dynamic business landscape. Organizations that embrace these trends can enhance their project accounting capabilities and drive better project outcomes.

What is Project Accounting Software?

Project accounting software is a specialized category of software designed to facilitate the financial management of individual projects within an organization. These software solutions are tailored to the needs of project-based businesses and industries where work is conducted on a project-by-project basis.

Project accounting software offers a range of features and tools that help streamline budgeting, cost tracking, revenue recognition, time and expense management, and reporting for projects.

Here's an introduction to project accounting software:

Key Features and Functionalities:

Budgeting and Planning:

- Create project budgets based on estimated costs and expected revenues.

- Allocate resources and funds to different project tasks or phases.

Cost Tracking and Control:

- Monitor and control project expenses, including direct and indirect costs.

- Identify cost overruns and take corrective actions.

Revenue Recognition:

- Apply revenue recognition methods to match revenue with project progress.

- Ensure revenue recognition aligns with industry standards and contractual agreements.

Time and Expense Management:

- Track time spent by team members on project tasks and activities.

- Manage and record project-related expenses, including travel and materials.

Invoicing and Billing:

- Generate invoices for clients based on project milestones or agreed-upon terms.

- Include detailed information about work completed, expenses, and terms of payment.

Resource Allocation:

- Optimize resource allocation to maximize productivity and efficiency.

- Allocate personnel, equipment, and materials to different project components.

Variance Analysis:

- Analyze discrepancies between budgeted and actual costs and revenues.

- Gain insights into project performance and financial health.

Financial Reporting:

- Generate project-specific financial reports, such as project status, profitability, and variance reports.

- Communicate financial information to project managers and stakeholders.

Integration and Automation:

- Integrate project accounting data with broader financial systems for consistent reporting.

- Automate processes like data entry, time tracking, and invoicing.

Compliance and Auditability:

- Adhere to accounting standards, regulations, and tax requirements specific to project accounting.

- Maintain accurate documentation for auditing purposes.

Benefits of Project Accounting Software:

- Efficiency: Project accounting software streamlines financial processes, reducing manual data entry and administrative tasks.

- Accuracy: Automated calculations and data entry minimize the risk of errors in financial reporting.

- Transparency: Project managers and stakeholders gain clear insights into project financials and progress.

- Real-time Reporting: Access to real-time financial data enables informed decision-making.

- Cost Control: The software helps monitor costs, prevent overruns, and maximize profitability.

- Resource Optimization: Efficient resource allocation leads to better resource utilization.

- Compliance: Ensures adherence to accounting standards and regulatory requirements.

Considerations When Choosing Software:

- Industry-specific features

- Integration capabilities with existing systems

- Scalability to accommodate growing projects

- User-friendliness and ease of adoption

- Cost and budget considerations

- Customer support and training offerings

In conclusion, project accounting software is a valuable tool for organizations that manage projects, helping them maintain control over finances, optimize resource utilization, and achieve project success.

It simplifies complex financial processes, enhances transparency, and supports effective decision-making throughout the project lifecycle.

How to Buy Project Accounting Software?

Purchasing project accounting software requires careful consideration of your organization's needs, budget, and specific requirements. Here's a step-by-step guide to help you navigate the process of buying project accounting software:

1. Identify Your Needs:

- Determine the specific needs of your organization. What features and functionalities are essential for your project accounting processes?

2. Define Your Budget:

- Set a budget for the software purchase, considering not only the initial cost but also ongoing expenses like licensing, support, and training.

3. Research and Shortlist:

- Research available project accounting software solutions in the market.

- Consider factors such as industry fit, scalability, integration capabilities, user-friendliness, and customer reviews.

4. Request Demos:

- Contact software vendors to request product demos. Demos allow you to see the software in action and assess how well it meets your requirements.

5. Evaluate Features:

- Evaluate each software's features and functionalities against your organization's needs.

- Prioritize features that align with your core requirements and project accounting processes.

6. Consider Integration:

- Check if the software can integrate with your existing systems (e.g., financial systems, project management tools, CRM).

- Integration ensures seamless data flow between different systems.

7. Scalability:

- Consider whether the software can accommodate your organization's growth and evolving project accounting needs.

8. Check Vendor Reputation:

- Research the reputation and reliability of the software vendor. Look for customer reviews, case studies, and testimonials.

9. Request References:

- Ask the vendor for references from organizations similar to yours that have implemented the software successfully.

10. Trial Period:

- If possible, opt for a trial period to test the software's functionality in your real-world scenarios.

11. Assess Support and Training:

- Inquire about the vendor's customer support and training options. Adequate support and training are crucial for successful software implementation.

12. Licensing and Pricing:

- Understand the software's pricing structure, including licensing fees, subscription models, and any additional costs.

13. Negotiation:

- Negotiate pricing and terms with the vendor to ensure the best deal for your organization.

14. Implementation Plan:

- Develop an implementation plan outlining the steps for deploying the software within your organization.

15. Training and Onboarding:

- Arrange training sessions for your team to ensure they are comfortable using the software effectively.

16. Data Migration:

- If applicable, plan for migrating existing data to the new software.

17. Contract Review:

- Carefully review the software contract before finalizing the purchase. Ensure it includes all agreed-upon terms and conditions.

18. Implementation and Launch:

- Follow the implementation plan to set up and configure the software as per your organization's needs.

19. Post-Implementation Support:

- Work closely with the vendor's support team to address any issues or questions that arise after implementation.

20. Continuous Evaluation:

- Continuously evaluate the software's performance and its impact on your project accounting processes.

Remember that buying project accounting software is an investment that can significantly impact your organization's efficiency and effectiveness. Take the time to thoroughly research, evaluate, and choose the solution that best aligns with your requirements and supports your project accounting goals.

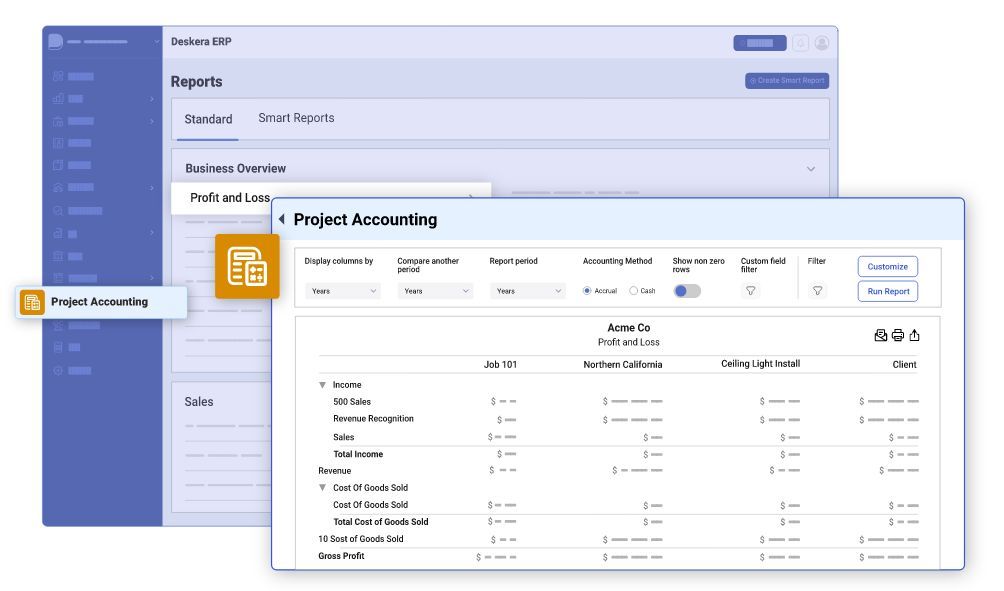

How can Deskera Help You with Project Accounting?

Deskera ERP offers a comprehensive suite of cloud-based business software solutions that can assist organizations with various aspects of project accounting.

Here's how Deskera can help you with project accounting:

- Bill of Quantities: This will help you accurately track project costs and revenue. This is because Deskera automatically calculates prices, discounts, taxes, and other factors for each item, while also ensuring real-time updates of a project’s bill of quantities.

- Project Time Tracking: Through Deskera, you would be able to monitor your project progress because it automatically logs time spent on tasks and projects. It also ensures accurate billing based on actual project time. Deskera ERP also enables efficient project tracking and management.

- Payment Milestones: With Deskera, you will be able to create payment milestones to streamline accounts payable, set custom payments with specific dates and amounts, and ensure timely payments by setting reminders and notifications.

- Revenue Recognition: With Deskera you will be able to ensure timely invoicing because it enables upfront recognition of revenue. It also allows cost-based accounting for revenue recognition. Lastly, Deskera ERP ensures accurate reporting of revenue.

- Project Costing and P&L: Deskera will assist you in tracking financial health by monitoring, managing, and tracking project costs. It will also help in identifying and analyzing cost overruns, as well as monitoring and reviewing budget performance. Deskera ERP will also generate real-time Profit and Loss reports, and analyze cost and benefit performance, while also giving you financial visibility.

Moreover, you can use these features to create detailed reports and dashboards that provide you with an in-depth understanding of your project finances. With Deskera ERP, you can easily keep track of your project's financials and make better decisions that lead to increased profitability.

Key Takeaways

- Project accounting is a specialized branch of accounting that focuses on tracking, managing, and analyzing the financial aspects of individual projects within an organization. It involves monitoring project costs, revenue recognition, resource allocation, and financial reporting.

- Traditional accounting focuses on the overall financial management of an organization, while project accounting is specific to managing the finances of individual projects, tracking costs, and ensuring project profitability.