As a small business owner, it’s crucial that you know how to track, manage, and organize your business’ finances. This is done through a process known as financial reporting.

Financial reporting is the formal recording of the financial activities of your business into accounting reports.

From these reports, you can gain valuable insights related to the overall financial health of the business, as well as disclose these insights to various stakeholders and investors.

In this guide, we will go through the main principles of financial reporting, what makes the process so important, and everything else you need to know to manage financial reporting for your small business.

Here’s what we’ll cover:

- What Is Financial Reporting?

- Financial Reporting Standards

- Why Is Financial Reporting Important?

- Financial Reporting Principles

- 4 Main Types of Financial Reports

- 9+ Tips for Better Financial Reporting

- Financial Reporting FAQ

- Automate Your Financial Reporting with Online Accounting Software

What Is Financial Reporting?

Financial reporting is the accounting practice business owners use to generate their financial statements. Financial statements, also commonly known as accounting reports, are documents that summarize key financial insights of the business.

The main financial statements business generate are four. They include:

- The balance sheet statement, which provides a financial snapshot at a particular point in time of three main components: assets, liabilities, and owner’s equity.

- The statement of changes in equity displays the ownership the business owner has over the business after debt and other financial liabilities have been paid off.

- The income statement or profit & loss statement, which reports all revenue and expense accounts during an accounting period.

- The cash flow statement, which reflects the cash that has been spent for operating, financing, and investing activities.

This document lets you know where cash comes from & goes, the type of assets and equity you own, as well as the profitability of your business.

Typically, financial reporting covers a one-year period, meaning accounting reports are created at the end of each fiscal year. However, if you want to get a more frequent view of your finances, you’re free to generate reports more often, whether that is quarterly or every six months.

Financial Reporting Standards

Depending on where your business is located, financial reporting is standardized through two main accounting guidelines:

1. Generally Accepted Accounting Principles (G.A.A.P)

Generally Accepted Accounting Principles (G.A.A.P) are a set of accounting principles, standards, and procedures that public companies in the United States must adapt to when doing their financial reporting.

Other non-publicly traded companies and small businesses in the US are not legally required to comply with GAAP. That being said, most companies, no matter their ownership or size, still follow GAAP rules, as the guidelines are preferred by lenders and creditors.

In fact, almost all financial institutions will require G.A.A.P-compliant accounting reports as part of their debt agreement. So, if you’re ever in need of a loan, funding, premises, or any other form of resource, banks and investors will be hesitant to lend to you if you can’t provide them with reliable, G.A.A.P-compliant financial documents.

2. The International Financial Reporting Standards (IFRS)

The International Financial Reporting Standards (IFRS) are a set of financial reporting rules for over 120 countries in the European Union, Asia, and South America. These rules specify how companies should maintain their accounts, define the various types of financial transactions, and establish a consistent set of guidelines for financial reporting.

Similar to G.A.A.P, only public companies are legally required to follow IFRS. However, IFRS is embraced by most businesses, as it helps them maintain transparency and credibility in global financial markets, as well as attract new creditors.

Why Is Financial Reporting Important?

As we’ve mentioned, almost every business, regardless of whether it is legally required, generates financial statements and keeps daily records of transactions.

Here are 5 of the main reasons why financial reporting is so important:

1. Managing Finances

Financial reporting is built upon rules that guarantee accurate and comprehensive bookkeeping of your cash and financial transactions. Everything gets recorded chronologically through a systematic process that tracks down every aspect of your transactions.

You always have a 360-degree view of the money that’s flowing in and out of the business, as well as any receivables, payables, customer past due invoices, profit generated, losses incurred, inventory count and so much more.

2. Taxation

A government agency known as the Internal Revenue Service (IRS) is responsible for analyzing your accounting reports to ensure that you are paying the right amount in taxes. So, it’s important that you record every transaction that occurs within the business, to best comply with the legal tax requirements of the IRS.

At the same time, by using financial reporting to keep a proper record of all your business expenses, you can deduct them from your taxable income, and pay less in taxes at the end of the year.

If you want to learn how to manage your deductibles and how to create an income statement that helps you pay less in taxes, head over to our guide on business expenses.

3. Investors and Creditors

For investors, shareholders, creditors, and customers to take a serious interest in your business, you need to have an appropriate financial reporting system set in place. This can help show third parties that you’re managing an honest, professional, and reliable business. It also lets them know what to expect from you in the future.

Creditors, for instance, need to take a look at your cash flow to evaluate your business’ ability to meet loans, invoice payments, and other financial obligations. Investors, on the other hand, want to look at your net profit, sales, margins, to assess how much value your business holds and evaluate whether the investment is worth it.

4. Decision-Making and Analysis

Financial reporting makes it easier for businesses to analyze their situation and make educated decisions.

Through financial reports, businesses can identify best-selling goods and services, growing departments, re-investment opportunities, the current value of assets, and many other real-time metrics and financial insights, all of which can be used for decision-making and analysis.

5. Reducing Errors

In financial reporting, transactions are recorded based on debit and credit rules. These rules make it so that debit and credit entries are always equal in the end. If these entries aren’t equal, you’ve most likely made an accounting error along the way.

Financial reporting makes spotting and correcting these mistakes easy - all you have to do is take a glance at the balance sheet statement. And if you’re using online cloud accounting software to automate financial reporting, you’ll be notified right away in case of any out-of-balance amounts.

Financial Reporting Principles

Before diving into the nits and grits of each financial statement, let’s first cover some of the most important accounting principles.

As you already know, your financial statements are made up of your financial transactions. Now, your transactions can’t be immediately translated into financial statements - they first need to go through a step-by-step process known as the accounting cycle.

The accounting cycle initially records transactions as journal entries, based on the double-entry bookkeeping method. In double-entry bookkeeping, one transaction affects at least two accounts, where one is debited and the other is credited.

There are five main types of accounts that experience these debit and credit changes, and they include:

- Assets: What a business owns

- Liabilities: Obligations a business owes

- Owner’s equity: The owner’s rights on assets of the business

- Revenue: Income from sales, services, and other operating activities.

- Expenses: The costs of doing business

More specifically, debits increase an asset or expense account and decrease a liability or owner’s equity account.

Meanwhile, credits do the opposite: they increase a liability or owner’s equity account and decrease an asset or expense account.

The next step in the accounting cycle is posting these journal entries and their appropriate debit and credit balances, into the general ledger. The general ledger is a record-keeping system that keeps track of all the business’ accounts and their content.

Then, the data is transferred into an unadjusted trial balance, which is a listing of the general ledger accounts before any end-of-period adjustments have been made. Then, when the end of the period (year or month) comes, adjusting entries are made to ensure accounting reports are up-to-date and contain the correct financial information.

Once these adjustments are finished, a new adjusted trial balance is created. Now your business has all the necessary data to prepare accounting reports.

4 Main Types of Financial Reports

We previously went through and defined the four main types of accounting reports generated through the financial reporting process.

Now, we’ll go through the details and purpose of each statement one by one, so you can better understand how to create these reports for your own small business accounting.

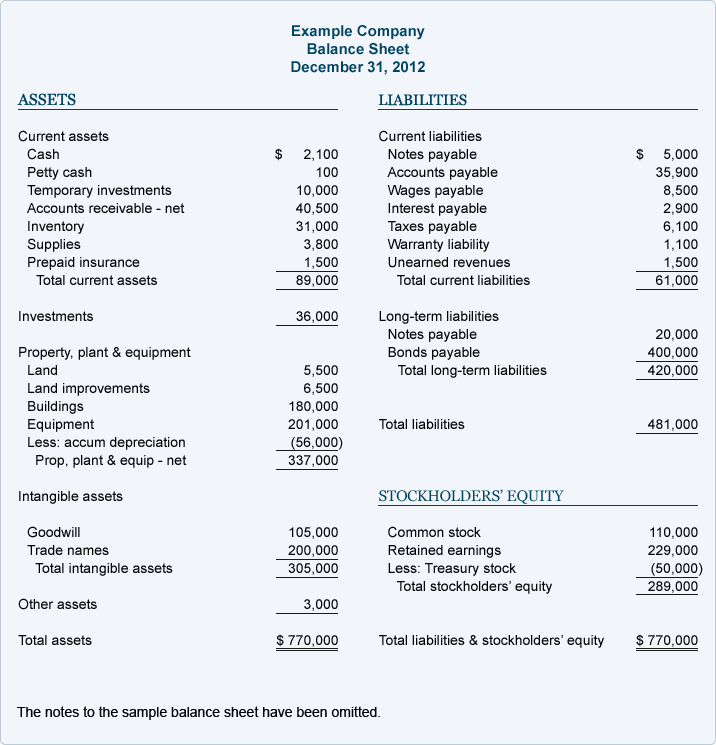

1. The Balance Sheet

The balance sheet displays a business’ financial position at a specific date. As the document presents the financial data only for a particular moment, rather than a time interval, the balance sheet is also commonly referred to as a snapshot of the financial health of a business.

The balance sheet expresses the equality of the accounting equation, which goes as follows:

Assets are the resources a business owns. They’re listed first, on the left side of the statement. There are three main asset categories that include current, fixed, and intangible assets.

Liabilities represent the obligations of a company. They are listed second on the right side of the balance sheet. They’re commonly divided into two types: current and non-current liabilities.

Owner’s equity/shareholder’s equity (if we’re dealing with a corporation). This is a list of the owner’s investment in the business, retained earnings, common stock, and treasury stock.

According to the equation, assets must always be equal to the total balance of liabilities and owner’s equity, or else, a mistake was likely made along the way.

Here’s an example of a balance sheet:

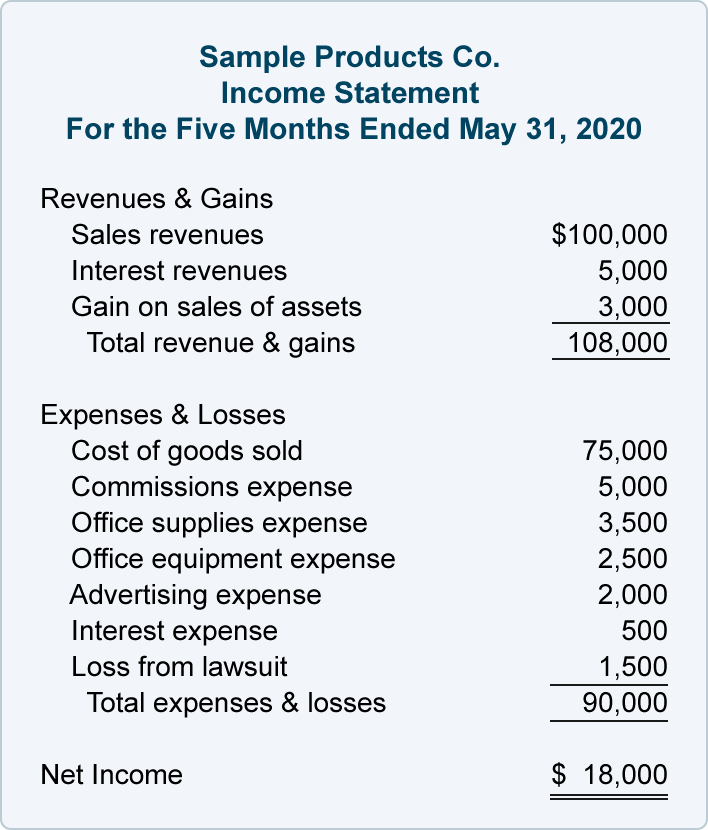

2. The Income Statement (Profit & Loss Statement)

The income statement, or profit and loss statement, is an accounting report that displays how profitable your business has been over a certain period, usually a fiscal year.

More specifically, the income statement displays two important financial accounts: revenue and expenses.

Revenue is listed first, and it includes the total amount of cash and profit the business has been able to generate from financial activities such as sales, services, interest revenue, and more.

After listing the revenue accounts and their balance, second, come expense accounts. Those include operating expenses and non-operating ones, such as maintenance, utilities, rent, insurance, depreciation, amortization, and more.

The ending balance of expenses is subtracted from revenue, determining the profitability of the business, or in other words the net income/net loss.

This is what these elements put together into an income statement usually look like:

3. Cash Flow Statement

A cash flow statement provides data regarding cash inflows and outflows from operating, financing, and investing activities. So, the purpose of this financial reporting document is to show you whether these types of financial activities have increased cash income for a certain time period.

Operating activities are the core activities that a business conducts in order to provide its products or services. This can include manufacturing, marketing, and any other core activity that directly influences cash flow.

Financing activities focus on how a business raises capital and pays back vendors, so it records transactions related to debt, equity, and dividends.

Lastly, investing activities include investments into the business, such as the purchase or sale of long-term assets.

Here’s an example of a cash flow statement:

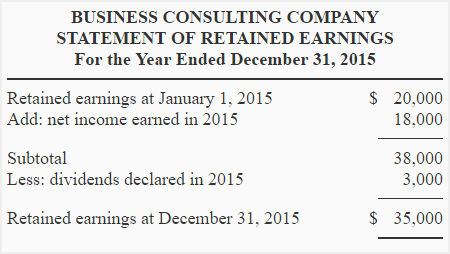

4. Statement of Changes in Equity

A statement of changes in equity or a statement of retained earnings is an accounting report that details the changes in owner’s equity over one accounting period. The changes reflected on the document include components such as earned profits, dividends, investment in capital, withdrawal of capital, net loss, and so on.

Here’s an example of a statement of changes in equity:

9+ Tips for Better Financial Reporting

- Store all of your financial data into one spreadsheet or software, to eliminate errors and inconsistencies.

- Log in every dollar coming in and out of the business, even if it’s a small and inconsequential purchase. Recording everything is crucial in bringing in investors, paying less in taxes, and staying legally compliant.

- Keep records of all the receipts and sales invoices you receive and issue, so you can easily balance your accounts at the end of the year.

- Create a standard chart of accounts for every type of transaction the business takes part in.

- Separate your personal finances from the business finances by opening a new business bank account.

- Consider opening a second savings account where you deposit a percentage of your business’ earnings every month.

- Make monthly reconciliations for both your bank account and credit card statements, to prevent possible errors from hanging around your books.

- Automation is a lifesaver for your small business financial reporting. The more you automate, the more accurate your bookkeeping and reports will be, and the more time you’ll free up to focus on managing your business.

- If your business is expanding, and taxes have become way too complex for you to manage on your own, consider looking for help by outsourcing through an accountant.

- Use accounting software to access your accounting information at any point in time, from any device with an internet connection.

Financial Reporting FAQ

1. How Does IFRS differ from GAAP?

Besides the fact that the International Financial Reporting Standards (IFRS) is adopted globally, and Generally Accepted Accounting Principles is used exclusively by companies in the United States, there are two other important differences between the two guidelines:

Firstly, GAAP is rule-based, whereas IFRS is principle-based. As a principle-based guideline, the IFRS is better at capturing the financial details of a transaction than GAAP.

The second important difference relates to inventory valuation methods. With GAAP you can use the Last In, First Out (LIFO) inventory valuation method, whereas the IFRS doesn’t allow it.

If you’re a merchandising company and want to learn more about inventory tracking, check out our guide on inventory management.

2. Who Is Responsible for Financial Reporting?

Most of the time, managers are tasked with the responsibility of generating financial reports and making sure they comply with all legal requirements.

That being said, getting outside help from a qualified accountant or automated software is a common business practice for many companies.

3. What Are Financial Reporting Requirements?

Some of the basic requirements or features that financial reporting statements need to reflect include: a fair presentation, an ongoing concern, use of the accrual basis of accounting, annual generation, and consistency.

Automate Your Financial Reporting with Online Accounting Software

With cloud accounting software like Deskera, you can manage, plan, and track all of your small business’ financial reporting, through one integrated platform.

The software covers all of your reports, starting from income statement, balance sheet, statement of cash flow, statement of changes in equity, all the way to the initial general ledger and trial balance reports.

Tax calculation is just as easy!

Deskera comes with an in-built tax feature that generates all of your tax reporting in compliance with the corresponding tax regulations of the country that your business is located in.

And that’s not even the best part.

The software and its features are accessible anytime, anywhere, from any device with an internet connection, by simply downloading the Deskera mobile app.

Give financial reporting with Deskera a try out right away, by signing up for our completely free trial.

Key Takeaways

And that’s a wrap! If you’ve made it this far, you might be feeling a bit overwhelmed by the amount of information in this guide.

So, let’s quickly recap some of the main points we’ve covered today:

- Financial reporting is the practice of generating financial statements at the end of an accounting period.

- This practice is supported and standardized through two main guidelines: Generally Accepted Accounting Principles (G.A.A.P) for the US and Generally Accepted Accounting Principles (G.A.A.P) for the global market.

- Financial reporting is crucial as it helps you manage your finances, complies with taxation rules, draws in investors and creditors, aids the decision-making process, and reduces the possibility of error.

- The four main reports generated during the financial reporting process include:

- The balance sheet statement

- The income statement

- The cash flow statement

- Statement of owner’s equity

- Through accounting software like Deskera, you can completely automate your financial reporting, in a matter of seconds.

Related Articles