The GSTR-5 (Goods and Service Tax Return) is a kind of GST return statement/document that needs to be filed every month by a registered non-taxable person (NRTP).

It is further for those individuals who execute businesses establishment transactions in India. This process can be filed either by online method or from a tax facilitation center.

In this brief article, we will understand GSTR-5 for non-resident and related concepts. We’ll cover:

- About Non-Resident Foreign Taxpayer

- Significance of GSTR-5

- Due Date of GSTR-5

- Registration of Non-Resident Foreign Taxpayers (under section 27)

- Consequences of not filing GSTR-5

- Consequences of delayed GSTR-5 filing

- Detail Requirements Needs to be Provided in GSTR-5

- Frequently Asked Questions (FAQs) on GSTR-5

About Non-Resident Foreign Taxpayer

NRTP stands for Non-Resident Foreign Taxpayers. It signifies those suppliers who do not have fixed or permanent business establishments in India.

Further, non-resident foreign taxpayers (NRTP) occasionally engage in transactions of goods or services from abroad and make local supplies in India. Those individuals are required to fill in GSTR-5 details.

In addition, Section 24 of the GST Act specifies the obligation for non-resident taxable persons to register. It lists a number of businesses and entities that must register under the Goods and Services Tax but are exempt from the Rs. 20 lakh/ Rs. 10 lakh minimum threshold restriction.

Eventually, every non-resident individual or organization will be required to register under the Goods and Services Tax, regardless of whether the business engages in a one-time or frequent taxable transaction.

Significance of GSTR-5

GSTR-5 is highly important as it contains all business information on all outgoing supplies (sales) and inward (purchases) supplies made and received by the non-resident taxpayer. Moreover, GSTR-5 form details will auto-populate into GSTR-2A of buyers.

Due Date of GSTR-5

As per the GST Act (as per Section 27), the GSTR-5 is due on the 20th of each consecutive month, or within 7 days of the registration expiry date.

Under Section 27 of the GST Act, a special GST Registration certificate shall be provided to NRTP or CTP (casual taxable person). It will also be valid for the specified time or 90 days from the date of effective registration, whichever comes first.

As a result of this clause, the NRTP is required to provide the GSTR-5 within 7 days of the GST Registration expiring.

Check the following table to know the schedule of GSTR-5:

Registration of Non-Resident Foreign Taxpayers (under section 27)

As per section 27 of the CGST Act, a temporary registration certificate is issued to NRTP, which is valid for 90 days. However, the GST authority can further extend the period only if proper reasons are provided.

Once the non-resident taxable person receives the certificate, he/she can carry out business transactions in India. Although, it must be noted that the NRTP taxpayer needs to file GSTR-5 within seven days before the interim GST registration expires.

Consequences of not filing GSTR-5

You will not be able to file returns for the succeeding month if you fail to file GSTR-5 returns. Also, a heavy fine or penalty will be imposed for the same.

Consequences of delayed GSTR-5 filing

You will be assessed interest and a late fee if you fail to file your return on time. Further, 18 percent is the annual rate of interest.

Moreover, it must be evaluated by the taxpayer based on the amount of unpaid tax. The time period will run from the next day after filing (the 21st of the month) until payment is received.

Nevertheless, a late fee of Rs. 50 per day and Rs. 20 is charged if there is no return. The maximum penalty for delayed filing is Rs. 5,000.

Note that there is no late penalty when it comes to IGST.

Detail Requirements Needs to be Provided in GSTR-5

As prescribed by the Government, there are 14 headings that come under the GSTR-5 form. Check the following detailed requirements that must be reported under GSTR-5.

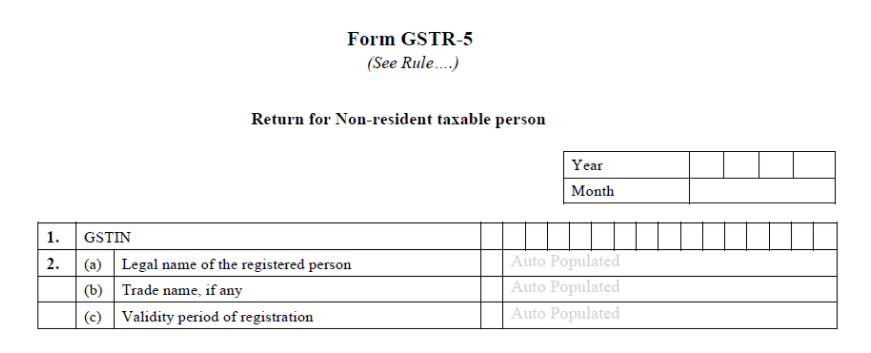

1. GSTIN

GSTIN stands for Goods and Services Tax Identification Number. Further, it is a 15-digit number with a 2-digit state code, a 10-digit permanent account number, and a 3-digit includes state, future usage, and check-digit. When we file returns, it is auto-populated.

The NRTP has to enter your GSTIN. However, you can use your provisional ID in case you do not have GSTIN.

2. Name of the Taxpayer

Three fields will be auto-populated: the taxpayer's legal name, the business's trade name, and the registration's validity period.

- This box should be filled in with the name of the registered taxpayer for your company (who is also the authorized signatory under the GST law).

- Registration validity duration – The registration validity period will be auto-populated as well.

- Month/Year — Indicate the month and year in which the GSTR-5 is being filed.

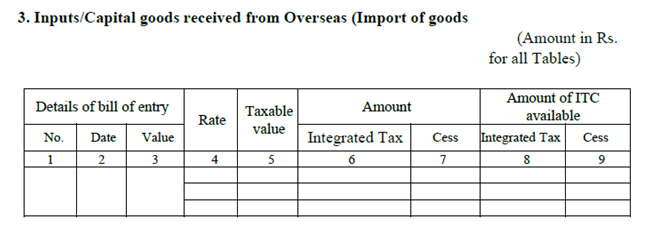

3. Inputs/Capital goods received from Overseas (Import of goods)

Inputs and capital items imported into India must be reported to the NR.

Details of the bill of entry, including the tax rate, IGST, and cess paid, as well as the amount of ITC available. Note that an NR will only be able to import materials from outside the country (purchases).

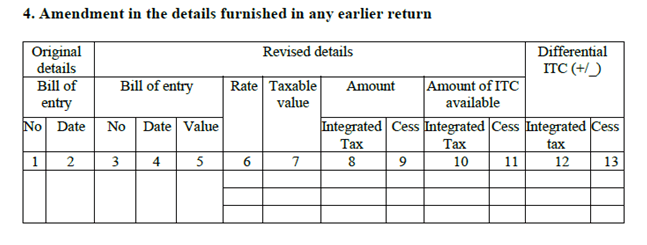

4. Amendment in the details furnished in any earlier return

The NR can update any details in imports provided in previous returns in this section. Modifications can be made in numerous ways.

- Bill of entry details (B.O.E)

- Rate of GST.

- Taxable Value.

- Amount of IGST and Cess.

- Amount of ITC available.

- Differential ITC amount emerging from those modifications (if excess will be reversed and vice versa).

Note: Both the original and revised Bill of Entry information must be showcased.

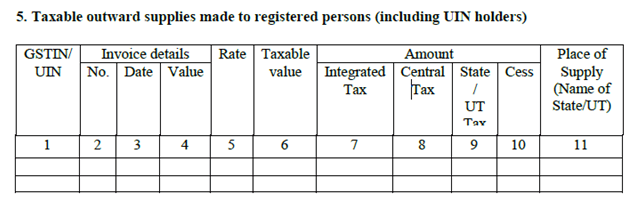

5. Taxable outward supplies made to registered persons (including UIN holders)

The NRTP is needed to record all outbound supplies details, including UIN holder to sales, in this portion of GSTR-5. Moreover, details about IGST/CGST, SGST, and Cess, as well as the state, must be provided.

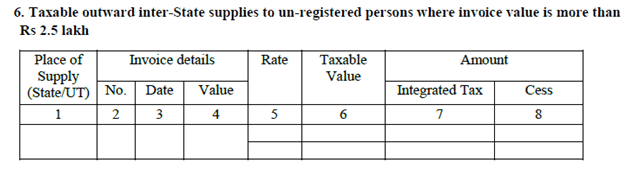

6. Taxable outward inter-State supplies to un-registered persons where invoice value is more than Rs 2.5 lakh

Under this segment of the GSTR-5 Form, the non-resident taxpayers must declare all contents associated with B2C large sales, i.e. inter-state invoices with values surpassing the 2.5 lakh INR limit.

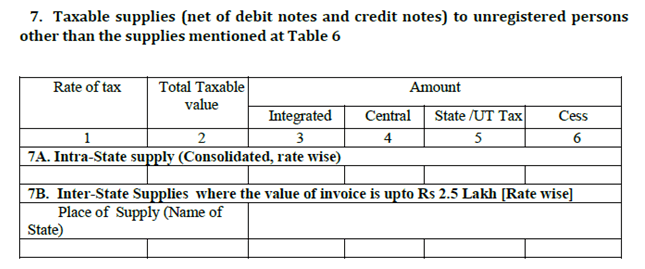

7. Taxable supplies (net of debit notes and credit notes) to unregistered persons other than the supplies mentioned at Table 6

It comprises information on sales to unregistered suppliers that will be encompassed in the report (B2C Others). Further, sales of less than 2.5 lakhs, including intra-state and inter-state, must be mentioned. Furthermore, Inter-state sales must be listed separately for each state, whereas intra-state sales can be included in a consolidated summary.

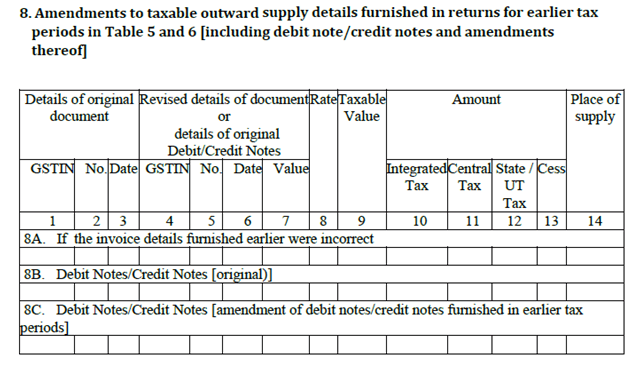

8. Amendments to taxable outward supply details furnished in returns for earlier tax periods in Table 5 and 6 [including debit note/credit notes and amendments thereof]

Any modifications in particulars of B2B and B2C from prior months will be mentioned under this segment. Here, original debit and credit notes from the preceding month will be provided. In addition, changes to invoices, as well as debit and credit notes issued, will be listed here. Moreover, original details must be supplied in the case of revisions.

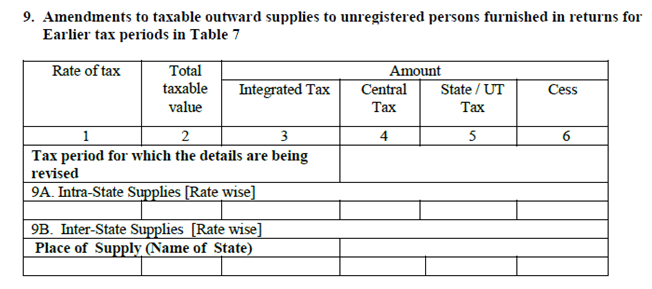

9. Amendments to taxable outward supplies to unregistered persons furnished in returns for earlier tax periods in Table 7

Under this section, modifications in particulars of B2C sales from preceding months will be recorded (formerly published in Table 7). Furthermore, in a consolidated summary, intra-state sales can be highlighted. State-by-state interstate sales must be disclosed.

10. Total Tax Liability

This segment will showcase your total tax liability. As a result of the outward supply:

- This section will detail the tax liability for outbound shipments for the current month.

- Due to the fact that the differential ITC in Table 4 is negative:

- This will include any additional tax due to the reversal of ITC (i.e., differential ITC being negative) on any adjustments to earlier months' imports (Table 4).

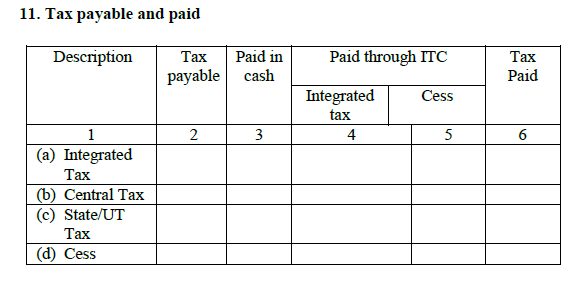

11. Tax Payable and Paid

The specifics of the tax you paid during the month will be listed under this heading. The IGST, CGST, SGST, and Cess will be showcased here. Moreover, the taxpayer has the option to choose between paying cash or claiming the ITC.

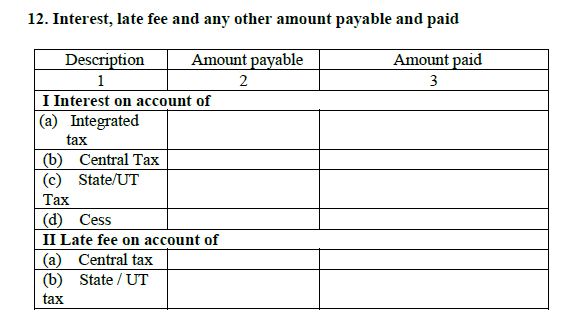

12. Interest, late fee, and any other amount payable and paid

This heading will detail the amount of interest and late fees due and paid as a result of the return's late filing.

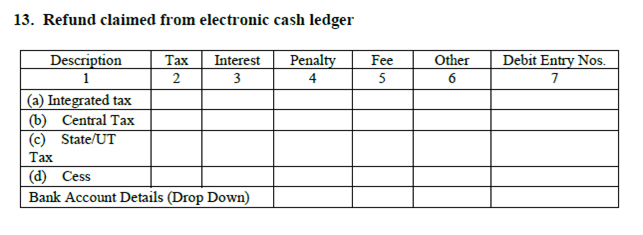

13. Refund claimed from electronic cash ledger

In this section, the NRTP needs to submit information on refunds claimed from the electronic cash ledger under multiple headings. It includes IGST, CGST/UTGST, CESS, and SGST. Also, the NR can choose which bank account the refund should be sent to from a dropdown menu.

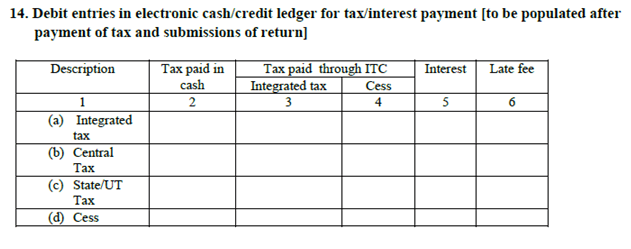

14. Debit entries in electronic cash/credit ledger for tax/interest payment [to be populated after payment of tax and submissions of return]

In this division of the GSTR-5 Form, the NRTP must provide the information of cash outflow from the credit ledger or e-cash for interest payment or tax.

Finally, an authorized signature must sign the GSTR-5 Form along with a designation.

Verification

Note: In this case, the NRTP representative is an authorized signatory who is both an Indian citizen and possesses a valid PAN.

Frequently Asked Questions (FAQs) on GSTR-5

We have added some frequently asked questions that will clear all your doubts. Let’s check:

1. How Can I obtain access to GSTR-5?

After logging in to the Returns Dashboard, the taxpayer can quickly obtain GSTR-5 on the GST Portal.

Let's take a look at the path:

2. Can I preview GSTR-5 before submission?

Yes, you can preview GSTR-5 on the GST portal.

3. Which modes are associated with signing GSTR-5?

You can sign in through EVC or DSC.

4. Is there a way to get a credit for taxes paid on services imported from outside India?

A non-resident taxpayer's credit card claim is not eligible for taxes paid on the import of services from outside India.

5. Can I reclaim the refund and when?

Yes, the refund might be claimed from the electronic cash ledger in the last refund, which would be determined after taking into account the extended registration period. Moreover, the refund from the Electronic Cash Ledger can be implemented if the liability register has zero balance covering the major and minor heads.

How Deskera Can Assist You?

Discover how you can combine accounting, finances, inventory, and much more, under one roof with Deskera Books. It's now easier than ever to manage your Journal entries and billings with Deskera. The remarkable features, such as adding products, services, and inventory, will all be available to you from one place.

Experience the ease of implementation of the tool and try it out to get a new perspective on your accounting system.

It is an innovative system for invoicing, accounting, and various aspects related to accounting such as fixed assets, purchase order and invoice, credit note. Fundamentally, Deskera Books is an all in one place that helps businesses focus on their core tasks and goal accomplishment.

Deskera Books is a time-saving strategy for managing your work contacts, invoicing, bills and expenses. In addition, opening balances can be imported and chart accounts can be created through it.

Key Takeaways

We have summarised the crucial points for your reference in this end section of this detailed guide. It includes:

- The GSTR-5 (Goods and Service Tax Return) is a kind of GST return statement/document that needs to be filed every month.

- NRTP stands for Non-Resident Foreign Taxpayers.

- Section 24 of the GST Act specifies the obligation for non-resident taxable persons to register.

- As per the GST Act (as per Section 27), the GSTR-5 is due on the 20th of each consecutive month, or within 7 days of the registration expiry date.

- You will not be able to file returns for the succeeding month if you fail to file GSTR-5 returns.

- The NRTP has to enter your GSTIN. However, you can use your provisional ID in case you do not have GSTIN

Related Articles