The U.S. Department of Labor (DOL) says that up to 11 million individuals across the country who work for small businesses or are independently employed don't have employer-sponsored insurance for medical care.

This ignites a need for knowledge about AHPs. Going through the insights, the U.S. Office of Commerce revealed that several effective AHPs across various states accomplished huge investment funds of 13% to 49%.

As an entrepreneur, deciding what health care coverage plan is best for your business is critical to recruiting and retaining workers. To get a more profound understanding of AHPs, this article will unload the ideas of Association health plans.

- Association Health Plan

- History of Association Health Plans

- Features of AHP

- Changes Made In Final Association Plan Rule

- Regulation

- How do Association Health Plans work?

- How to Join an Association Health Plan?

- Plan Types

- What Are Some AHP Advantages?

- What Are Some AHP Disadvantages?

- Most Recent News on Association Health Plans

- Key takeaways

Association Health Plan

AHPs are courses of action in which small businesses and self-employed workers band together within businesses, geographic regions, or professions to either buy large group health coverage or self-insure. Association health plans (AHPs) are a kind of altered medical coverage that a few managers love. New rule changes imply that AHPs will get one more opportunity at acknowledgment. AHPs permit independent companies to gather as one and haggle for protection plans as a large business would.

In the insurance world, there are two sorts of the group (i.e., employer) insurance: little and huge. Each state has its own definition for "little" and "huge," in any case, the contrast between the little group and huge group insurance is significant on the grounds that the costs and guidelines you should keep rely upon your group.

Despite the fact that lowers in cost, AHPs accompany less consumer protection. AHP critics claim the arrangement will urge healthy workers to leave the individual health care coverage market, making it less cutthroat and leaving behind sicker and costlier workers in the business sectors to battle for coverage.

History of Association Health Plans

Association health plans have been around for a really long time yet became undesirable during the 1990s. Colorado even prohibited the formation of new AHPs within its borders, referring to scams and false claims coming from the actual plans.

Association plans that accepted impossibly broad groups used to be designated "fake AHPs," on the grounds that they served "air breathers" or "weight trainers" instead of narrow professional organizations.

The 2014 Affordable Care Act was the straw that broke the camel's back for many AHPs. They essentially vanished from public view once individual health insurance became simpler to see on the net.

Bringing association plans back is essential for the continuous political battle over American health care coverage. In October 2017, directly following an unsuccessful attempt to repeal Obamacare, the White House declared a few recommendations for public medical services policy - including the extension of AHPs.

Features of AHP

Easier To Join

To keep individuals from holding on to purchase insurance until they're wiped out, Affordable Care Act plans are simply open to new individuals during the 6-week Open Enrollment Period. When Open Enrollment closes, many individuals must choose the option to purchase temporary health insurance. Some even do without coverage by any means.

Conversely, association health plans can decide to be more straightforward to access consistently.

Include Health Insurance Basics

Association health plans work like conventional, significant medical health insurance. Whenever you go along with it, you ought to hope to get a familiar membership card.

Most association plans to partner with a bigger health insurer’s network of doctors. You might be acquainted with how smaller cell phone companies lease and resell minutes from AT&T. Additionally, your association plan can give low rates by paying for members’ care in bulk.

New Plan Designs

Association health plans can be planned such that appeals to specific groups more than others. A few plans will offer skimpy coverage for professionally prescribed drugs, yet better coverage for yearly tests.

Thusly, AHPs might draw healthy members from their present coverage. Obamacare plans and employer-based insurance will keep on engaging more Americans with chronic conditions.

Price Flexibility

Association health plans can set different month-to-month costs known as premiums in light of risk characteristics like age, orientation, and industry factors. Plans framed before new government rules were made in 2018 can use a small group’s health status to set premiums.

The Affordable Care Act (ACA) prevented most health plans from utilizing health status or preexisting circumstances to decide premiums, however, risk attributes like age were permitted. Along these lines, insurance agencies spread the costs of enrollees' cases - even the priciest claims - among everybody in the plan.

Association health plans will recapture greater flexibility to set month-to-month premiums on an individual basis. Subsequently, more youthful Americans, who tend to be healthier, will by and large pay less to use an association health plan rather than an Obamacare plan. Notwithstanding, Obamacare plans do incorporate powerful subsidies for those with low incomes.

AHPs won't be permitted to deny membership or charge various costs in view of protected qualities like race or religion. They can't charge somebody something else for being wiped out or exclude coverage for a pre-existing condition.

Older Insurance Rules

AHPs will qualify as least fundamental coverage under the Affordable Care Act, and when smaller groups join under an AHP with 50 or more workers, it's likely to have large group rules, which are more lenient than small-group rules. However dissimilar to most health coverage that you can buy all alone, association health plans are barely managed by the ACA and the Department of Health and Human Services.

All things being equal, a few guidelines for association plans are checked on by the Department of Labor. Since AHPs are supported by employers, they are viewed as Multiple Employer Welfare Arrangements (MEWAs) under a more seasoned government regulation known as ERISA. Other AHP rules might fall under state guidelines rather than the national government.

While there are cross-country consumer protection laws that apply to association health plans, many state regulations keep away from the subject of AHPs. AHPs might not need to meet the stricter financial stability prerequisites of most other insurance plans, follow local complaint resolution laws, or keep state rules for sufficient doctor access.

Changes Made In The Final Association Plan Rule

An AHP can offer completely insured health plans bought through a dealer or self-fund and work their own health plans. AHPs with completely insured health plans can begin offering them under the new rule beginning September 1, 2018.

The last rule made a couple of changes in accordance with current AHP rules, including:

- Extends the rules for membership, giving individuals access to a similar profession or geographic region form and join AHPs.

- Permits sole owners, consultants, and their families called "working owners" to join AHPs.

- Forestalls health underwriting, or utilizing every member’s medical conditions to decide their month-to-month premiums.

- Loosens yet doesn't get rid of the meaning of "associations". Already, an AHP's supporting association couldn't exist principally to give medical insurance. Presently, the associations behind AHPs can exist to give medical insurance as their principal objective. Basically, assuming that the associations behind AHPs perform support only a bit of community service alongside their arrangement, they will not be penalized.

Eventually, new AHP rules keep up with certain limitations on who can join a plan. The new principles additionally don't give AHPs a free pass from state or government guidelines.

State protection guidelines additionally apply to AHPs. To complicate the issue, individual state insurance commissions have weighed in regarding the AHP circumstance, for certain states endorsing the new DOL rule and different states dismissing it.

As a matter of fact, POLITICO reports that the National Federation of Independent Businesses (NFIB) feels that the expansive new AHP strategy isn't what they wanted. NFIB was a main backer of AHPs for quite a long time. Yet, as indicated by the NFIB's disappointed representative, they can't set up an AHP under the new guidelines any more than they could under the old standards.

A few pieces of the AHP guidelines were at issue in the legal dispute, including:

Permitting AHPs to reduce expenses by not expecting them to give all fundamental medical advantages as expected by the ACA

- Extending the meaning of employer to including groups coordinated for insurance purposes without a past commonality of interest

- Permitting AHPs to be named large group plans, keeping away from some state regulations

- Permitting independently employed people to join an AHP since the first purpose was inclusion for "workers"

To assist associations that have already formed and that need to shape AHPs, the DOL has permitted health plans to work on one of two sets of rules, called "Pathway 1" the old rule, and "Pathway 2" the new rule.

- Pathway 1 AHPs go on as in the past, including not permitting independently employed people without workers to join and not permitting associations dependent exclusively upon geography.

- Pathway 2 AHPs can't join new employer members, however, they can keep on enlisting new hires and current workers on special enlistment events like marriage, birth, and so on.

Regulation

Association health plans are controlled by a mix of government regulations. The numerous regulations relating to AHPs include:

- The Women’s Health and Cancer Rights Act

- ERISA - The Employee Retirement Income Security Act of 1974 (ERISA)

- ACA - The Affordable Care Act

- HIPAA - The Health Insurance Portability and Accountability Act of 1996 (HIPAA)

- The Genetic Information Nondiscrimination Act

- PHS - The Public Health Service (PHS) Act

- MHPAEA - The Mental Health Parity and Addiction Equity Act of 2008

- COBRA - The Consolidated Omnibus Budget Reconciliation Act of 1985

- MHPAEA - The Mental Health Parity and Addiction Equity Act of 2008

- The Civil Rights Act

AHPs are additionally controlled at the state level. For instance, state regulations overseeing Multiple Employer Welfare Arrangements (MEWAs) apply to AHPs. Moreover, AHPs utilizing an outsider insurance agency for their health coverage may likewise be liable to state-explicit benefit mandates.

How do Association Health Plans work?

Organizations in small group coverage all pay a similar rate for a similar arrangement. Large group coverage, then again, permits you to arrange the rates. Since AHPs qualify as a "large group," this implies private companies could possibly get less expensive plans and give those reserve funds to their workers.

AHPs are coordinated and overseen under ERISA and they should follow guidelines of the Affordable Care Act (ACA) that safeguards workers in employment-based group health plans.

How to Join an Association Health Plan?

To join an AHP, your association should share a "commonality of interest" with its individuals. By and large, this has implied that you are in a similar exchange, industry, line of business, or profession. Under the new rule, an AHP could likewise be made in light of organizations in a similar region, like a state, province, or metro region.

For instance, an AHP should be a "bona fide group or association of employers." Under the standard, its main purpose can be to give medical coverage to its individuals. Nonetheless, it should have no less than one communicated business purpose irrelevant to giving medical care. While the rule didn't unequivocally characterize "business purpose," models referred to include:

- To participate in advertising exercises like promoting, advertising, and distributing on business issues important to association individuals.

- To set business norms or practices

- To offer classes on business issues important to its individuals

An AHP should be constrained by its individuals, however, those individuals don't need to run the everyday tasks of it and can rather choose directors, legal administrators, and such to do as such. One significant exemption for note is that an AHP can't be possessed or constrained by an insurance issuer or a subsidiary or affiliate of one.

Track down an AHP by checking with your trade association to check whether they have an arrangement.

A few different spots to check:

- Existing associations like the International Franchise Association

- Your school alumni association

- Industry, trade, or expert groups

Notwithstanding AHPs, the DOL permits small businesses to unite as one to offer Association Retirement Plans (ARPs) to their workers.

Plan Types

An association health plan can either be completely safeguarded or self-insured. These terms concern how the AHPs are supported and who holds the monetary risk related to medical cases.

Completely insured plans are the insurance course of action with which most buyers are familiar. In this model, an outsider health care coverage organization assumes the risk of medical costs in return for expenses. A self-insured arrangement, interestingly, doesn't move the risk of medical cases to an outsider insurance agency.

All things considered, it holds the obligation to pay those costs itself. A self-insured plan pays for the cases from its own monetary assets including any expenses charged to workers. A self-insured arrangement might in any case involve outsiders for exercises, for example, record-keeping, claims management, compliance, and so forth A self-insured plan may likewise use "stop-loss" insurance to safeguard the AHP from horrendous medical expenses.

According to an administrative point of view, self-insured plans are commonly considered to have more adaptability than completely insured plans, however, there are state contrasts by the way they are directed. Self-insured plans can likewise cost less than fully-insured plans since they are not subject to health care coverage tax and an outsider health care coverage organization isn't creating gain from the coverage however some benefit might be paid assuming that a stop-loss insurer is utilized.

Besides the funding types of completely insured and self-insured, an association health plan can come in any of the traditional types of healthcare delivery:

- EPO

- HMO

- PPO

An EPO is an Exclusive Provider Organization. EPOs are like HMOs with respect to in-network care limitations however they ordinarily miss the mark on the need for referrals from a primary care provider.

An HMO is a Health Maintenance Organization. In an HMO, health benefits are limited to in-network suppliers for standard care for example non-emergency circumstances. HMO members should acquire a reference from their primary care providers for lab tests, trained professionals, and different services not given by a primary care doctor.

A PPO is a Preferred Provider Organization. In a PPO, members might pick in-network or out-of-network medical care suppliers without the need for a prior referral. Larger out-of-pocket costs are commonly charged for out-of-network care.

What Are Some AHP Advantages?

Expand Your Range of Healthcare Options

AHPs should have significant and considerable member representation. Employers should effectively practice control over the plan’s advantages and administration, regardless of whether they run the everyday workings of the plan.

It's critical to have more options in the unfriendly medical coverage market. In principle, making AHPs bigger can effectively distribute risk and cut down costs for everybody. Truly, that is something we've heard in each round of American health reform, with little achievement.

Avoids Expensive Obamacare Requirements

Association health plans don't need to adhere to large numbers of the ACA's principles.

- AHPs can stay away from the charges that individual health insurance needs to pay, as:

-sponsoring their ACA competitors-"risk adjustment"

-offering income-based discounts with respect to services "cost-sharing reductions", which used to be paid by the central government, yet are currently fused into premiums

- AHPs can qualify for large group rules, so they skip small group rules like EHB prerequisites, single risk pool, risk adjustment, and "metal levels" necessities.

- AHPs don't need to record as much paperwork as plans that are recorded on the national government's medical insurance site. In many states, AHPs have fewer regulatory burdens also.

Work With HSAs and Existing Health Tools

Different parts of the health framework are viable with association plans.

- On the off chance that you have a health savings account (HSA), you can utilize it to pay for AHP medical costs - yet if you have any desire to continue to add to your HSA, your AHP should be an HSA-qualified high-deductible health plan.

- Doctor workplaces by and large don't have the slightest care about what sort of insurance you have.

- Also, association plans actually need to play by fair principles, similar to no illegal discrimination and no exclusions of pre-existing health conditions.

Don't Pay for Unnecessary Care

Association health plans don't need to cover Obamacare's fundamental medical advantages. Most health plans in individual and small group markets have needed to cover every one of these 10 significant kinds of care - like rehabilitation and emergency services- started around 2014.

Rivals of mandatory essential health benefits dislike that the advantages are one-size-fits-all. For example, EHBs expect men to pay for unused maternity care. Furthermore, fundamental medical advantages are not generally covered well - they're essentially covered. A large part of the expense sharing weight can in any case be on the plan member and not the plan, for services that are not entirely covered with few physicians available.

What Are Some AHP Disadvantages?

AHPs might be liable for fraud

AHP fraud-fake AHPs have been normal previously, and there's some disarray with the new DOL guideline about whether these plans are likely to state guidelines.

Don't Focus On Consumer Protection

ACA plans and completely insured AHPs have to spend 80% or a greater amount of their monthly premiums on medical care, yet self-insured AHPs don't. There's likewise no government cap on what dealers can be paid for referring individuals to AHPs. This risks creating plans that offer unusually poor health advantages, or spend unnecessarily on regulatory costs.

The new rules explicitly forbid AHPs from fitting their own guidelines to deny coverage to explicit, high-need individuals. This keeps plans from skipping a specific ZIP code or dismissing a specific business since it's the known area of somebody with a chronic health condition. Be that as it may, the weight of proving this rule is for the most part on the impacted individual or employer.

Avoid Essential Health Benefits

Since association health plans follow large group guidelines, they don't need to cover fundamental medical advantages. Affordable Care Act plans in the individual and small group markets have needed to cover every one of these 10 significant sorts of care - like rehabilitation and emergency services- started around 2014.

Supporters of fundamental medical advantages battle the advantages are essential so that individuals don't experience unexpected gaps in their health care coverage. Advocates say that the presence of these advantages brings down costs for everybody since, in such a case that individuals stay better, they're less inclined to record expensive claims. The AHP model risks everybody paying something else for any of the more uncommon services they'll ultimately require.

Decreased state guidelines could likewise mean less spotlight on the monetary principles of AHPs, potentially expanding the risk that an AHP would become insolvent and not have the option to pay benefits. In any case, as per the DOL, the last rule "doesn't lessen state oversight, which stays set up. States will impart enforcement authority to the bureaucratic government."

Weaken the Obamacare Market

Assuming more individuals move to Obamacare options, the Obamacare market turns out to be less cutthroat. AHPs will speed up this pattern. Specialists accept that the normal spending per individual who stays on an ACA plan will increment by 1.4 to 4.4% and that their month-to-month charges would increment too.

Fewer advantages for workers

Being excluded from giving all fundamental medical advantages implies that some AHPs might remove a few advantages for workers like maternity medical services or mental health services and charge something else for certain, workers in view of health status and gender.

Most Recent News on Association Health Plans

Association health plans are in the news more than ever. In June 2018, the Department of Labor under Secretary Alex Acosta published its final rule on AHPs. A bunch of existing AHPs started to work under the new principles as early as August 20, 2018.

Nonetheless, 11 states, led by New York, effectively sued the government Department of Labor to forestall the AHP changes from producing results.

On March 28, 2019, DC District Court Judge John D. Bates decided that new AHP rules were clearly an end-run around existing health care coverage regulation. Self-insured plans utilizing the new AHP principles would have been permitted to start on April 1, 2019.

The Department of Labor chose to appeal the ruling. They additionally get an opportunity to reconsider and limit the new AHP rules all things considered. On Jan. 28, 2021, the Department of Justice mentioned a 60-day cessation to give the Biden organization time to review the issues for the situation and decide how to continue. A final decision is as yet forthcoming.

A review from the Society of Actuaries says that 3 to 10% of individuals with individual Obamacare plans would have joined an AHP because of the Executive Order. Researchers anticipated that between 13 should 43% of independently employed individuals would have joined an AHP. Moreover, up to 60% of individuals on Obamacare's catastrophic coverage level might have moved to AHPs.

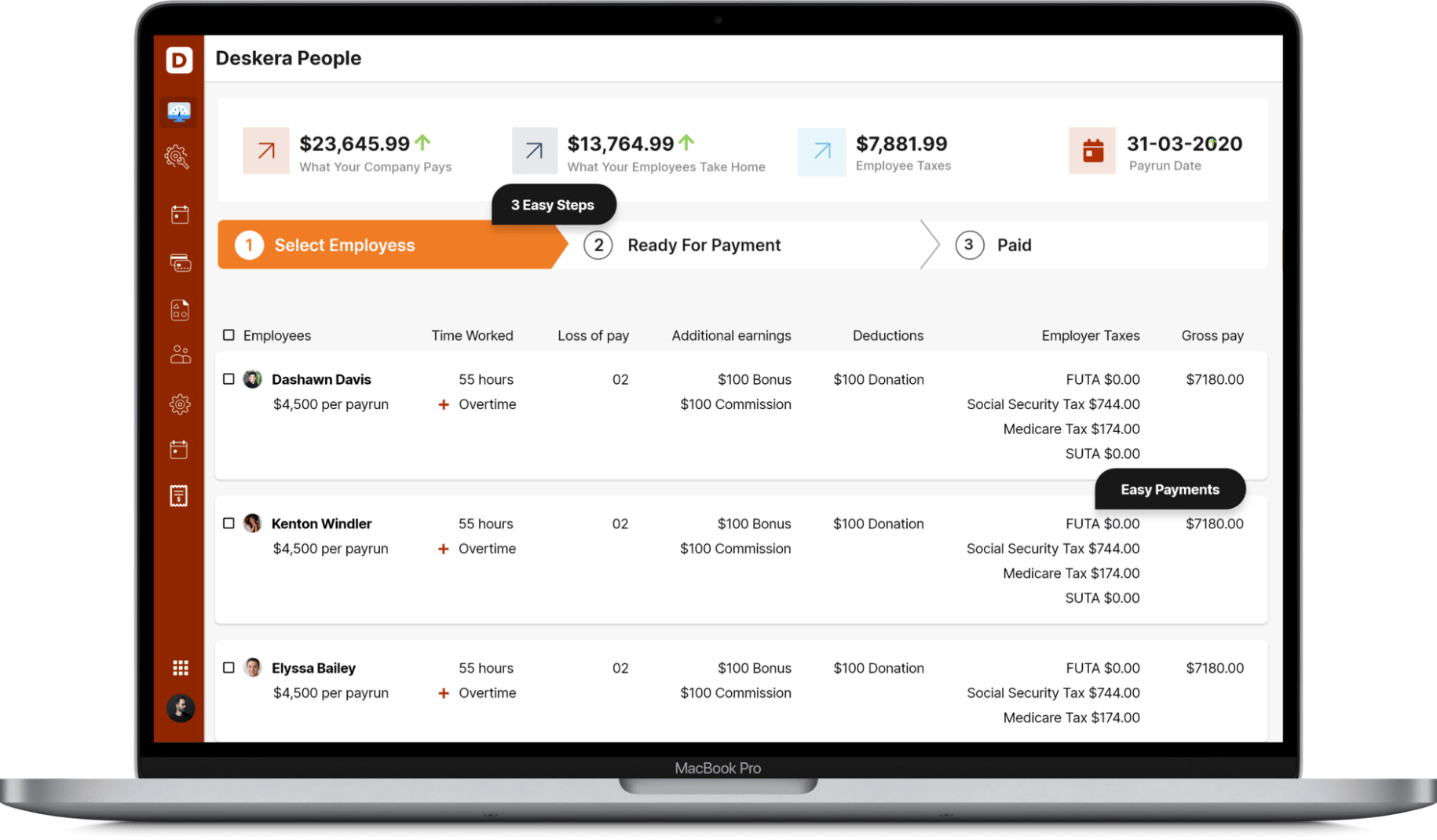

How Deskera Can help You?

Deskera People provides all the employee's essential information at a glance with the employee grid. With sorting options embedded in each column of the grid, it is easier to get the information you want.

Key takeaways

- Association health plans (AHPs) assist small businesses with giving their workers health coverage at reasonable expenses for individuals and at lower rates to workers.

- Association health plans are a sort of medical insurance that is presented by, and custom-made for, individuals with a commonality of interest. Plan individuals should have a similar industry or profession.

- Groups of organizations with a common reason, similar to a trade association or franchise organization, can shape an AHP.

Related articles