Are you tired of tedious manual finance processes that take up too much time and lead to errors? Have you been looking for ways to streamline your finance department's operations and increase efficiency? Look no further than automation. By leveraging automation, finance departments can create scalable processes that save time and reduce errors.

In fact, according to a report by Accenture, automation has the potential to reduce finance function costs by up to 40%. With the rise of digital transformation, automation has become increasingly crucial for businesses to stay competitive. Finance departments are no exception.

By automating manual processes such as data entry, invoice processing, and financial reporting, finance professionals can free up time to focus on higher-value tasks such as analysis and strategic planning.

This article will explore the benefits of automation for finance departments and provide practical tips for implementing automation in your organization. We will also discuss the latest trends in finance automation and the regulatory landscape for automation in the finance industry.

So, whether you're a CFO or a financial analyst, keep reading to learn how automation can transform your finance department.

Here's what we shall cover in this post:

- Introduction to Automation in Finance Departments

- Benefits of Automation in Finance Departments

- Overview of Scalable Processes in Finance Departments

- Types of Automation Tools and Technologies for Finance Departments

- Best Practices for Successful Automation in Finance Departments

- Common Mistakes to Avoid When Implementing Automation in Finance Departments

- Integration of Automation With Existing Finance Systems and Processes

- How Deskera Can Assist You?

- Conclusion

- Key Takeaways

Introduction to Automation in Finance Departments

Automation has become a buzzword recently, and finance departments have not been left behind. Finance departments are embracing automation to improve their efficiency, reduce manual errors and improve their overall financial performance.

Automation in finance departments refers to using technology to streamline financial processes, eliminate manual tasks, and optimize financial operations.

- Automation in finance departments involves using technology to automate repetitive, time-consuming financial tasks such as data entry, reconciliation, and report generation. This technology can be in the form of software or hardware, and it is designed to increase efficiency and reduce errors.

- Automation is vital in finance departments because it improves efficiency, reduces errors, and frees up staff time to focus on more important tasks. Automation also provides real-time insights into financial data, enabling businesses to make informed decisions based on accurate data.

- Some examples of automated finance tasks include accounts payable and receivable management, bank reconciliation, financial statement preparation, budgeting, and forecasting. Automated finance tasks can also include fraud detection, compliance monitoring, and risk management.

Benefits of Automation in Finance Departments

Automation in finance departments is becoming increasingly popular as businesses seek to improve efficiency and reduce errors. Here are some benefits of implementing automation in finance departments:

Increased Efficiency and Productivity

Automation helps finance departments to carry out their tasks more efficiently and accurately. It eliminates the need for repetitive manual tasks, such as data entry, which can be prone to errors.

Automation software can perform these tasks much faster and more accurately, allowing finance employees to focus on more value-added tasks. This leads to increased productivity and efficiency in the finance department.

Cost Savings

Automation in finance departments can lead to significant cost savings. By automating repetitive manual tasks, companies can reduce the number of employees required to perform these tasks, thereby reducing labor costs.

Automation also reduces the likelihood of errors, which can result in additional costs such as fines and fees.

Improved Accuracy and Compliance

The use of automation in finance departments can significantly improve accuracy and compliance. Manual processes are prone to errors, but automation reduces the risk of human error.

This ensures that financial data is accurate and up-to-date. Automation also helps companies to comply with regulatory requirements by ensuring that data is complete, accurate, and easily accessible.

Faster Processing Time

Automation in finance departments can significantly reduce processing time. Automated software can process financial data much faster than manual processes, which leads to faster decision-making and improved cash flow. This is particularly important for companies that rely on real-time financial data to make business decisions.

Improved Data Management

Automation in finance departments can help companies to manage their financial data more efficiently. Automated software can store financial data in a centralized location, making it easier to access and analyze. This leads to better insights and more informed decision-making.

Better Customer Service

Automation in finance departments can also improve customer service. Automated systems can provide customers with real-time information, such as the status of their payments or account balances. This leads to faster response times and improved customer satisfaction.

Scalability

Automation in finance departments can easily scale to accommodate business growth. As the volume of financial data increases, automated systems can handle the increased workload without requiring additional resources. This makes it easier for companies to scale their finance departments as their business grows.

Overview of Scalable Processes in Finance Departments

Scalable processes in finance departments refer to the ability of the financial system to handle a growing volume of work while maintaining or improving its efficiency. Here are some points that provide an overview of scalable processes in finance departments:

- Automation: Automation is a key element of scalable processes. By automating tasks like invoice processing or expense management, finance departments can reduce manual effort, minimize errors, and speed up the process.

- Integration: Integration between different systems and software applications is essential for scalability. When systems are integrated, data can be transferred seamlessly between them, and manual input can be minimized.

- Implementation of ERP systems: Enterprise resource planning (ERP) systems can help finance departments manage large amounts of data more efficiently. These systems provide a single source of truth for financial data, streamlining processes and reducing the risk of errors.

- Improved efficiency: By having scalable processes, financial departments can handle increased workloads without reducing performance and needing additional resources. This can help to improve efficiency and reduce operational costs.

- Standardization: Standardization of processes can improve scalability by making them repeatable and consistent. By having standardized processes, financial departments can reduce the time and effort required to complete tasks and improve accuracy.

- Flexibility: Scalable processes should also be flexible enough to adapt to changing circumstances. By being able to adjust processes to meet new requirements, financial departments can continue to deliver effective and efficient services to the organization.

- Cloud-based solutions: Cloud-based solutions provide additional scalability by enabling finance departments to access resources and data from anywhere, at any time. Cloud-based solutions are also easier to scale than on-premises solutions, which can reduce costs.

- Data analytics and reporting: By using data analytics and reporting tools, finance departments can gain more significant insights into their financial data. This helps them identify trends, make more informed decisions, and optimize their financial performance.

- Continuous improvement: Scalable processes require ongoing monitoring and improvement. By regularly assessing performance and making necessary adjustments, finance departments can continue to enhance their scalability and efficiency.

Challenges Faced in Finance Department Processes

Finance departments are integral to any organization, responsible for managing financial resources and ensuring the company's financial health stability. Despite the importance of finance departments, they often face several challenges that can affect their efficiency and effectiveness.

Here are some of the common challenges faced in finance department processes:

Manual data entry:

Manual data entry is a major challenge finance departments face in many organizations. In simple terms, manual data entry refers to manually inputting data into a computer system, often through spreadsheets or other software applications. While this process can be relatively simple for small amounts of data, it can quickly become overwhelming for larger volumes of data.

- One of the main challenges associated with manual data entry is the potential for errors. When individuals are tasked with manually entering data into a system, mistakes can easily be made, especially if they are dealing with large amounts of data or complex financial information. Even small errors can significantly impact financial statements and lead to costly mistakes down the line.

- Another challenge associated with manual data entry is the time it takes to complete. This is particularly true when dealing with large volumes of data, which can take hours or even days to enter manually. This can be a major drain on resources for finance departments, as it can take away from other critical tasks and leave less time for analysis and other essential activities.

- Additionally, manual data entry can be a highly repetitive and monotonous task, which can lead to boredom and burnout for employees. This can further impact their motivation and performance and lead to higher rates of errors.

- Finally, manual data entry can also present a challenge when it comes to data security. When data is entered manually, there is always the potential for unauthorized access or other security breaches. This can be a particular concern in finance departments, where sensitive financial information is often being processed and stored.

Inefficient workflows:

Inefficient workflows can also pose a challenge in finance department processes. When there are too many manual processes involved, it can lead to delays and errors.

- One of the biggest causes of inefficient workflows in finance departments is the reliance on manual processes. When employees must manually input data, create reports, or perform calculations, it can lead to errors and delays. This can be especially problematic when working with large data sets, as manually input all the required information can be time-consuming.

- Many finance departments rely on multiple tools and systems to complete their work.

- While each tool or system may be designed to address a specific need, this can create inefficiencies when it comes to data entry, data transfer, and reporting.

- Additionally, employees may need to be trained on each tool or system, which can add to the time and costs associated with completing tasks.

Limited visibility:

Limited visibility is a major challenge faced by finance departments as it can cause delays in decision-making, errors, and compliance issues. Limited visibility means that the finance department has limited or no access to critical data that is required for efficient and accurate financial reporting.

This data can include information related to revenue, expenses, cash flow, and other financial metrics.

Lack of integration:

The lack of integration in finance departments refers to the inability of various systems to communicate and share data effectively. For instance, the accounting system may not be integrated with the budgeting system, resulting in manual data entry and reconciliation. As a result, this challenge can lead to a significant waste of time and resources.

Compliance issues:

Compliance is a major challenge faced by finance departments in organizations of all sizes. Compliance regulations and laws are put in place to ensure that companies operate within the legal and ethical boundaries set by the government.

- Failure to comply with these regulations can result in severe consequences such as fines, legal action, and damage to the company's reputation.

- One of the biggest challenges for finance departments is keeping up with the complex regulations related to financial operations.

- These regulations are often vague and subject to interpretation, making it difficult for organizations to ensure they are meeting all the requirements. The regulatory environment is constantly changing, which further complicates the compliance process.

Cybersecurity risks:

Finance departments handle sensitive financial data, and cybersecurity risks can pose significant challenges. Ensuring data security and protecting against cyber threats is critical for the smooth functioning of finance departments.

- Phishing attacks are one of the most common forms of cyber attacks, and finance departments are a prime target. Phishing emails can trick employees into providing sensitive financial information, such as bank account details, credit card numbers, or login credentials.

- Ransomware attacks involve infecting a system with malware that encrypts files and demands a ransom payment in exchange for a decryption key. If finance departments do not have appropriate backup and recovery measures in place, a ransomware attack could result in significant financial losses.

- Malware attacks can infect systems with viruses, trojans, and other types of malicious software. These attacks can disrupt finance department processes, compromise data security, and cause financial losses.

- Insider threats are risks that arise from employees or other insiders who have access to sensitive financial information. This can include intentional actions, such as fraud or theft, or unintentional actions, such as accidental data disclosure.

Inadequate resources:

Finally, inadequate resources can be a significant challenge in finance department processes. Limited budget, staff, or technology can hinder the department's ability to perform their tasks efficiently and effectively.

- With limited resources, finance departments may not have enough staff to handle the workload. This can lead to delays in processing financial transactions, generating reports, and completing other essential tasks.

- Inadequate resources can also result in limited budget allocation for necessary tools and technology, which can hinder the department's ability to operate efficiently and effectively.

- Without adequate resources, finance departments may not be able to provide sufficient training and development opportunities for their staff. This can lead to a lack of skills and knowledge, resulting in errors and compliance issues.

Key Considerations for Implementing Automation in Finance Departments

Automation in finance departments can bring numerous benefits, such as increased efficiency, accuracy, and cost savings. However, it requires careful planning and consideration before implementation.

Here are some key considerations to keep in mind when implementing automation in finance departments:

Evaluate Current Processes: Before implementing automation, it is crucial to evaluate the current finance processes to identify areas where automation can be introduced. This step is essential to identify the areas that need improvement, determine the benefits that can be gained from automation, and ensure that automation is implemented most effectively.

Reviewing the existing processes can help determine which tasks are time-consuming, redundant, or prone to errors and which can benefit from automation.

Define Clear Objectives: Setting clear objectives is critical when implementing automation in finance departments. Define specific goals that you want to achieve with the automation process and ensure they align with the overall business strategy.

Clear objectives help determine the right automation tools and measure the automation process's success.

Select the Right Tools: Selecting the right automation tools is crucial for the success of the automation process. Consider the nature of finance processes and select tools that are designed to meet the specific needs of finance departments.

Some of the commonly used tools include accounting software, robotic process automation, and workflow automation.

Identify Data Sources: The automation process's accuracy and effectiveness depend on the data quality used. Identify the sources of data needed for the automation process, such as internal systems, third-party systems, and spreadsheets.

Ensure the data is accurate, up-to-date, and easily accessible for automation tools.

Develop Robust Security Protocols: Automated processes require the exchange of sensitive financial information, which can be susceptible to cyber threats. Develop robust security protocols that protect the finance department from external and internal threats.

This includes implementing access controls, encryption, and monitoring tools to ensure data privacy and prevent data breaches.

Prioritize Employee Training: Automation can lead to changes in the roles and responsibilities of employees in the finance department. Prioritize employee training to ensure they understand how to use the new automation tools and processes effectively.

This will help maximize the benefits of automation and reduce the resistance to change.

Implement Automation in Phases: Implementing automation in phases can help minimize disruptions and reduce risks. Begin with a small pilot project and gradually scale up to full implementation. This approach can help identify and address any potential issues that may arise in the early stages of implementation.

Measure and Monitor Performance: Measuring and monitoring the performance of the automation process is critical to ensuring that it is achieving the intended objectives.

Establish key performance indicators (KPIs) and regularly evaluate the progress toward meeting the goals. Use this data to identify areas for improvement and optimization.

Types of Automation Tools and Technologies for Finance Departments

Automation tools and technologies are rapidly transforming the way finance departments operate. With the availability of a wide range of tools and technologies, finance professionals are now able to automate various tasks, from data entry to complex financial analysis.

The adoption of automation can help finance departments improve their efficiency, reduce errors, and increase productivity.

Robotic Process Automation (RPA)

Robotic Process Automation (RPA) is a software technology that allows organizations to automate repetitive and rule-based tasks, improving operational efficiency and reducing costs. In finance departments, RPA can automate various manual processes, such as data entry, account reconciliation, and invoice processing.

- In finance departments, RPA can be used to automate a variety of tasks, such as data entry, account reconciliation, and invoice processing. RPA can be used to extract data from various sources, such as emails, invoices, and spreadsheets, and then process this data to complete multiple tasks.

- For example, an RPA tool can extract data from invoices, validate the data against company policies, and then post the data into an accounting system.

- RPA can help finance departments reduce operational costs, improve efficiency, and reduce errors. By automating repetitive and rule-based tasks, RPA frees employees to focus on more complex tasks requiring human expertise. Additionally, RPA can help finance departments improve accuracy by reducing the risk of errors caused by manual data entry.

- One of the challenges of implementing RPA in finance departments is the need for IT support and infrastructure. RPA tools require IT resources to set up and maintain and must be integrated with existing systems and processes. Finance departments must ensure that RPA is used in compliance with regulatory requirements and data privacy laws.

- RPA can be used in a variety of finance department processes, such as accounts payable, accounts receivable, and general ledger accounting. For example, RPA can be used to automate invoice processing, where invoices are extracted, validated, and processed without human intervention.

- Additionally, RPA can be used to automate account reconciliation, where transactions are matched and reconciled automatically.

Applications of RPA in Finance Departments

RPA offers numerous applications within finance departments, streamlining various processes and improving overall operational efficiency. Some key areas where RPA can be deployed in finance include:

Accounts Payable and Receivable: RPA can automate invoice processing, payment processing, and reconciliation tasks. Bots can extract relevant data from invoices, verify it against purchase orders and contracts, and update accounting systems accordingly. RPA can also handle routine accounts receivable tasks, such as sending payment reminders and updating customer records.

Financial Reporting and Analysis: RPA can automate data collection and consolidation for financial reporting and analysis. Bots can extract data from multiple sources, validate it, and populate financial reports or dashboards. RPA can significantly reduce the time and effort required for generating accurate and timely financial reports.

Regulatory Compliance: Compliance processes in finance, such as Know Your Customer (KYC) checks and Anti-Money Laundering (AML) screenings, can be automated using RPA. Bots can collect customer information, perform background checks, and generate compliance reports. RPA ensures adherence to regulatory requirements and reduces the risk of human error.

General Ledger and Account Reconciliation: RPA can automate general ledger entries, journal entries, and account reconciliation processes. Bots can validate data, match transactions, identify discrepancies, and initiate corrective actions. RPA improves accuracy, reduces reconciliation time, and enhances financial control and integrity.

Financial Planning and Forecasting: RPA can automate data gathering for financial planning and forecasting processes. Bots can extract data from various systems, perform calculations, and populate financial models. RPA enables faster and more accurate financial analysis, allowing organizations to make informed decisions.

Artificial Intelligence (AI)

Artificial intelligence (AI) is revolutionizing the way finance departments operate by automating and streamlining various processes. AI is the simulation of human intelligence in machines programmed to learn, reason, and solve problems.

With the ability to analyze vast amounts of data quickly and accurately, AI technology has become an essential tool for finance departments to make data-driven decisions and improve their operational efficiency.

- One of the most significant benefits of AI in finance departments is its ability to streamline accounting processes. For instance, AI-powered tools can automate the invoice processing process, making it faster and more efficient. This includes capturing and verifying invoice data, updating accounting records, and sending out payments.

- Another benefit of AI in finance is improved data analysis. AI can help finance teams analyze vast amounts of real-time data, helping identify trends and make better-informed decisions. For example, AI-powered tools can help finance teams identify patterns in sales data, forecast revenue, and optimize inventory levels.

- AI can also play a vital role in fraud detection in finance departments. Fraud detection algorithms can analyze transaction data to identify anomalies or suspicious activity, alerting finance teams to potential fraud or errors. This can help finance teams take action to prevent losses and ensure compliance with regulations.

- AI can help finance teams manage risks by identifying potential risks and providing real-time insights into market trends. For example, AI-powered tools can analyze financial data to identify potential credit risks, market volatility, and other factors that may impact business performance.

Machine Learning (ML)

ML is a type of AI that enables machines to learn from data without being explicitly programmed. In finance departments, ML can be used for tasks such as credit risk assessment, fraud detection, and financial analysis. ML algorithms can analyze large volumes of financial data and identify patterns and trends that would be difficult for humans to detect.

- Machine learning can help identify potential fraudulent activities in financial transactions by analyzing large volumes of data and identifying patterns and anomalies that could indicate fraud.

- Machine learning algorithms can analyze large amounts of data to identify and quantify risk factors in various financial transactions, which can help financial institutions make informed decisions about lending, investments, and other financial activities.

- Machine learning can help portfolio managers identify opportunities and make better investment decisions by analyzing large amounts of data and identifying trends and patterns that could affect investment performance.

AI offers a wide range of applications within finance departments, enabling organizations to streamline operations, improve accuracy, and drive innovation. Some key areas where AI can be implemented in finance include:

Fraud Detection and Prevention: AI algorithms can analyze large volumes of data in real-time to detect patterns and anomalies associated with fraudulent activities. Machine learning models can learn from historical data and identify fraudulent transactions, potentially saving organizations significant financial losses.

Risk Assessment and Management: AI can analyze historical data and real-time market conditions to assess risks accurately. AI models can predict market trends, evaluate creditworthiness, and provide recommendations for portfolio management. This helps finance departments make more informed decisions and optimize risk management strategies.

Customer Service and Personalization: AI-powered chatbots and virtual assistants can provide personalized customer support, answer inquiries, and assist with basic financial tasks. Natural language processing algorithms enable these AI systems to understand customer queries and provide relevant information promptly.

Investment and Trading: AI algorithms can analyze large amounts of financial data, news, and market trends to identify investment opportunities. AI-powered trading systems can execute trades autonomously, leveraging machine learning models and algorithmic trading strategies.

Credit Scoring and Underwriting: AI can automate the credit scoring process by analyzing various data sources and historical credit data. Machine learning models can assess creditworthiness, predict default probabilities, and support underwriting decisions.

Natural Language Processing (NLP)

NLP is a type of AI that enables machines to understand and interpret human language. In finance departments, NLP can be used for contract analysis and compliance monitoring tasks. NLP can help finance professionals quickly identify and analyze key information from legal documents and regulatory filings.

- NLP is used to analyze the sentiment of financial news articles, social media posts, and other text-based content to help investors make more informed decisions. Sentiment analysis involves analyzing text to determine whether the overall tone is positive, negative, or neutral.

- NLP is used to identify fraudulent activities such as money laundering, insider trading, and other illegal financial activities. By analyzing patterns in large amounts of data, NLP can help identify suspicious behavior and alert authorities to potential fraud.

- NLP can be used to automate financial reporting processes by extracting financial data from documents and converting it into structured data that can be easily analyzed. This reduces the time and effort required to generate financial reports.

NLP offers a wide range of applications within finance departments, enabling organizations to leverage textual data for various purposes. Some key areas where NLP can be implemented in finance include:

Sentiment Analysis: NLP algorithms can analyze customer reviews, social media posts, and news articles to determine sentiment toward financial products, services, and companies. Sentiment analysis helps finance departments understand customer perceptions, identify emerging trends, and make informed decisions based on customer sentiment.

News and Market Analysis: NLP algorithms can analyze financial news articles, press releases, and market reports to extract relevant information. By monitoring news sources in real-time, finance departments can stay updated on market trends, competitor activities, and regulatory changes, enabling them to make more informed investment decisions.

Financial Document Processing: NLP can automate the extraction of key information from financial documents such as invoices, receipts, and contracts. NLP algorithms can extract relevant data points, such as amounts, dates, and vendor information, and populate financial systems, reducing manual data entry and improving accuracy.

Chatbots and Virtual Assistants: NLP-powered chatbots and virtual assistants can provide personalized customer support, answer queries, and assist with financial tasks. NLP enables these AI systems to understand customer intent, extract relevant information, and provide accurate responses, improving customer experiences and reducing the burden on human customer service agents.

Optical Character Recognition (OCR)

OCR is a technology that enables machines to scan text from image files or printed documents and convert it into searchable and editable text. In finance departments, OCR can be used for data entry and invoice processing tasks. OCR can help finance professionals quickly extract data from paper-based documents and reduce errors associated with manual data entry.

- OCR technology works by scanning and analyzing an image of text and identifying the characters within it. The technology then converts the characters into machine-readable text that computer systems can process.

- OCR technology offers several benefits to finance departments, including improved accuracy and efficiency of data entry, reduced manual effort, faster processing times, and better compliance with data security and privacy regulations.

- OCR technology can be used in various tasks in finance departments, such as invoice processing, document management, and data entry. For instance, OCR technology can be used to automatically extract data from invoices and input it into accounting software, reducing the need for manual data entry and minimizing errors.

- OCR software typically includes features such as text recognition, image enhancement, document segmentation, and data extraction. These features enable the software to accurately identify and extract text from documents, even when the text is distorted or difficult to read.

OCR offers a wide range of applications within finance departments, enabling organizations to streamline data entry processes and leverage unstructured data. Some key areas where OCR can be implemented in finance include:

Invoice Processing: OCR can automate the extraction of invoice information, such as vendor details, invoice numbers, and line item details. By converting scanned or photographed invoices into machine-readable text, OCR eliminates the need for manual data entry and speeds up the invoice processing cycle.

Receipt and Expense Management: OCR enables the extraction of key information from receipts and expense documents, such as date, amount, and merchant name. This streamlines the expense management process, eliminates manual data entry errors, and improves reimbursement workflows.

Bank Statement Analysis: OCR algorithms can extract transaction details from bank statements, including dates, amounts, and transaction descriptions. This enables finance departments to analyze transaction data, reconcile accounts, and generate financial reports more efficiently.

Form Processing: OCR can automate the extraction of information from forms, such as customer applications, loan agreements, and tax forms. By converting form data into digital text, OCR eliminates manual data entry errors and improves data accuracy.

Document Digitization: OCR facilitates the digitization of physical documents, such as contracts, agreements, and legal documents. By converting these documents into searchable and editable text, OCR improves document management, enables text-based search, and enhances collaboration.

Workflow Automation

Workflow automation involves the use of software tools to streamline and automate the flow of work within finance departments. Workflow automation can help finance professionals reduce manual tasks and improve efficiency.

Workflow automation tools can be used for tasks such as invoice approval, purchase order processing, and expense management.

- One of the main benefits of workflow automation for finance departments is increased efficiency. By automating manual and repetitive tasks, finance professionals can focus on more value-added activities such as analysis and strategic decision-making. This can also help reduce errors and improve the accuracy of financial data.

- Another benefit of workflow automation is improved visibility into financial operations. Automation tools can provide real-time data and insights into financial workflows, allowing finance professionals to quickly identify and address issues. This can help reduce risk and ensure compliance with regulatory requirements.

- Workflow automation can also help improve collaboration between finance and other departments. By automating invoice processing and purchase order processes, finance professionals can work more closely with procurement and other departments to ensure timely and accurate financial data.

Business Process Management (BPM)

BPM is a discipline that focuses on improving business processes through the use of technology. BPM tools can be used to model, automate, and optimize business processes within finance departments. BPM can help finance professionals identify areas of inefficiency and automate tasks that can be performed more efficiently.

- BPM can help finance departments streamline their processes and eliminate redundancies. By automating routine tasks, such as invoice processing or expense reporting, organizations can free up their staff to focus on higher-value activities. This can result in increased productivity and reduced costs.

- BPM can improve collaboration between different departments within an organization, including finance and accounting. By automating the flow of information and data, businesses can ensure that all relevant stakeholders have access to the information they need to make informed decisions.

- Finance departments are responsible for ensuring that their organizations comply with various regulations and standards. BPM can help finance departments to ensure that their processes are compliant and that all necessary documentation is maintained. This can reduce the risk of fines or other penalties.

Best Practices for Successful Automation in Finance Departments

As automation becomes increasingly prevalent in finance departments, it's important to establish best practices to ensure successful implementation and adoption. Here are some key considerations for implementing automation in finance departments:

Define Clear Goals

It's essential to define clear goals and objectives for automation projects in finance departments. This will help to ensure that the project stays on track and delivers the desired outcomes. The goals should be specific, measurable, achievable, relevant, and time-bound.

Engage Stakeholders

Engaging stakeholders from across the organization is critical for the success of automation projects in finance departments. Stakeholders can help to identify pain points and areas for improvement, provide feedback on prototypes, and ensure the solution meets their needs.

Start Small and Scale Up

Starting with a small pilot project is a great way to demonstrate the value of automation to stakeholders and gain buy-in for larger projects. Once the pilot project has been successful, it can be scaled up to other finance department areas.

Ensure Data Quality

Automation relies heavily on data, so it's vital to ensure that the data being used is accurate, complete, and consistent. Data quality can be improved through the use of data cleansing tools and processes.

Maintain Security and Compliance

Automation can bring significant efficiency gains but also new risks. Ensuring that the automation solution is secure and compliant with all relevant regulations and standards is crucial. This can be achieved through the use of secure coding practices, encryption, and access controls.

Focus on User Experience

Automation solutions should be designed with the end user in mind. The solution should be intuitive and easy to use, with clear instructions and feedback. User experience testing and feedback can help to identify areas for improvement.

Monitor and Measure Performance

Automation solutions should be monitored and measured to ensure they are delivering the desired outcomes. Key performance indicators (KPIs) should be established to track progress, and regular reporting should be provided to stakeholders.

Continuously Improve

Automation is an ongoing process, and there is always room for improvement. Regular reviews and updates to the solution can ensure it remains relevant and effective.

Provide Training and Support

Training and support are essential for the successful adoption of automation solutions in finance departments. Users should be trained on how to use the solution, and support should be provided to address any issues or questions that arise.

Role of Data Analytics and Visualization in Finance Department Automation

Data analytics and visualization have become essential components of finance department automation in recent years. These tools help finance professionals gain insights into their organization's financial performance, optimize processes, and make informed decisions.

Data analytics involves the use of software applications to collect, process, and analyze large datasets, while data visualization refers to the creation of charts, graphs, and other visual representations of data.

Data analytics enables finance departments to make data-driven decisions:

Data analytics provides finance professionals with valuable insights into their organization's financial performance. With data analytics tools, finance professionals can quickly collect and analyze data from various sources, such as financial statements, transactions, and budgets.

These tools enable finance professionals to identify trends and patterns in their data, such as changes in revenue, expenses, and cash flow. By making data-driven decisions, finance departments can improve their financial performance, reduce costs, and increase efficiency.

Data visualization makes data easier to understand:

Data visualization plays a critical role in finance department automation by making complex financial data easier to understand. Data visualization tools enable finance professionals to create charts, graphs, and other visual representations of financial data, making it easier for stakeholders to interpret and analyze.

These tools help finance professionals identify trends and patterns in their data, such as changes in revenue, expenses, and cash flow. By providing a clear and concise view of financial data, data visualization tools enable finance professionals to communicate financial information effectively to stakeholders.

Data analytics and visualization tools enable finance departments to optimize processes:

Data analytics and visualization tools can help finance departments optimize financial reporting, forecasting, and budgeting processes. By analyzing data from various sources, finance professionals can identify inefficiencies and bottlenecks in their processes.

They can then use data visualization tools to create visual representations of this data, making it easier to identify opportunities for improvement. For example, finance professionals can use data visualization tools to identify trends in their spending, enabling them to reduce costs and improve efficiency.

Data analytics and visualization can help finance departments detect fraud:

Data analytics and visualization tools can help finance departments detect fraudulent activity by analyzing financial data for anomalies and inconsistencies. By comparing data from multiple sources, finance professionals can identify transactions that are outside of normal patterns, such as unusual expenditures or discrepancies in financial statements.

By detecting fraud early, finance departments can reduce financial losses and mitigate reputational damage.

Data analytics and visualization tools enable finance departments to comply with regulations:

Data analytics and visualization tools can help finance departments comply with regulations by providing accurate and timely financial reporting.

By analyzing data from various sources, finance professionals can ensure that financial reports are accurate and complete. Data visualization tools enable finance professionals to create clear, concise reports that meet regulatory requirements.

Impact of Automation on Finance Department Staff

Here are some key points to consider regarding the impact of automation on finance department staff:

- Change in Job Roles: With the implementation of automation, some traditional finance job roles may become obsolete. For example, tasks such as data entry and manual calculations can now be automated, reducing the need for human involvement. However, this also opens up new job roles, such as automation specialists, data analysts, and business analysts who can work closely with automated systems to identify opportunities for improvement.

- Increased Focus on Analysis and Interpretation: With automation handling mundane and repetitive tasks, finance department staff can now focus more on analyzing and interpreting data, which is critical to decision-making. This shift can lead to more strategic thinking and better insights for the organization.

- Training and Upskilling: As automation continues to evolve and new tools and technologies are introduced, finance department staff will need to continually develop their skills and knowledge to stay current. Companies will need to invest in training and upskilling programs to ensure that staff can effectively work alongside automation tools and technologies.

- Improved Job Satisfaction: Automation can help reduce the time and effort required to complete certain tasks, which can improve job satisfaction among finance department staff. By eliminating the need for manual data entry and calculations, staff can focus on more challenging and meaningful work, leading to greater job satisfaction.

- Reduction in Errors: With automation handling routine tasks, there is less chance for human error to occur. This can help improve the accuracy and reliability of financial data, which is critical for decision-making and compliance purposes.

- Concerns Over Job Security: With the introduction of automation, some staff may be concerned about the security of their jobs. Organizations need to communicate the benefits of automation and how it can lead to new job opportunities and a more efficient department.

- Need for Change Management: The introduction of automation can be a significant change for finance department staff. Effective change management strategies will be required to ensure that staff are prepared and supported through the transition.

Common Mistakes to Avoid When Implementing Automation in Finance Departments

Not Defining Clear Goals

One of the most significant mistakes that finance departments make when implementing automation is not defining clear goals for the project. Specific business objectives should drive automation; a well-defined strategy is necessary for successful automation.

Without a clear set of goals, the project may not meet the needs of the business, or the expected ROI may not be achieved.

Overlooking the Need for Proper Training

Automation tools and technologies require specific skill sets, and staff must be trained to use them effectively. Failing to provide adequate training can lead to errors, frustration, and even project failure.

Training should be an integral part of the automation project plan, and all employees involved should be trained on the tools they will be using.

Not Involving Stakeholders Early On

Another common mistake is not involving all stakeholders in the automation project from the beginning. Finance departments should engage all stakeholders in the automation process, including employees, vendors, and customers.

This can help identify potential issues, obtain buy-in, and ensure the project aligns with overall business goals.

Choosing the Wrong Automation Tools

Finance departments often choose automation tools based on features or price rather than their ability to address specific business needs.

Choosing automation tools aligned with the company's goals, processes, and systems is crucial. Failing to select the right tools can result in wasted time, resources, and money.

Not Adapting Processes to Suit Automation

Another common mistake is to implement automation without adapting existing processes to suit the new system. Automation can significantly streamline workflows, but it requires an adjustment in processes to achieve maximum efficiency.

Automation projects should thoroughly analyze existing processes to identify areas where automation can add the most value.

Lack of Quality Assurance

Automation can help to reduce errors, but it can also create new ones. Lack of proper quality assurance can lead to inaccurate data and poor decision-making. Automation projects should include quality assurance processes like testing and validation to ensure accurate and reliable data.

Underestimating the Complexity of Integration

Automation tools and technologies need to be integrated with existing systems to work efficiently. Integration can be a complex process and may require specialized expertise.

Underestimating the complexity of integration can lead to significant project delays, increased costs, and even project failure.

Not Maintaining the Automation System

Automation systems require regular maintenance and updates to ensure their continued effectiveness. Failing to maintain automation systems can result in system failures, security breaches, and other issues. Maintenance should be included in the project plan and should be performed regularly to avoid potential problems.

Over-reliance on Automation

Finally, it is essential to recognize that automation is not a panacea for all finance department issues. Overreliance on automation can lead to complacency and a lack of critical thinking, which can result in poor decision-making. Finance departments should use automation as a tool to support and enhance their existing processes rather than as a replacement for them.

Integration of Automation With Existing Finance Systems and Processes

Assess existing finance systems and processes: Before integrating automation, it's crucial to evaluate the existing financial systems and processes to identify potential areas for improvement.

This assessment should include an analysis of data inputs and outputs, workflows, and system integrations. The evaluation will help determine which processes are most suitable for automation and which must be optimized before automation.

Identify the right automation tools: Once you've evaluated the existing systems and processes, it's essential to identify the right automation tools for integration. Some automation tools may not be compatible with existing systems or require significant customization.

Therefore, it's crucial to research and select automation tools that are compatible with existing finance systems and processes.

Develop a comprehensive integration plan: An integration plan should outline the specific steps required to integrate automation with existing finance systems and processes.

It should include timelines, responsibilities, and goals. The plan should also consider any potential challenges or roadblocks that may arise during the integration process and how to overcome them.

Ensure data quality and integrity: Data quality and integrity are critical for the success of finance department automation. Before integrating automation, it's essential to ensure that the data used in the automation process is accurate and complete.

Data quality can be ensured through data cleansing and standardization. Additionally, data integrity can be ensured through proper data validation and verification processes.

Test and validate the integration: Before deploying the automation solution, it's essential to thoroughly test and validate the integration. This step will help to identify any errors or issues before the solution is implemented.

The testing process should include a comprehensive review of data inputs and outputs, workflows, and system integrations. Any problems identified during testing should be addressed before deployment.

Monitor and continuously improve the automation process: Once the automation solution is deployed, it's crucial to monitor and continuously improve the automation process.

This step involves analyzing performance metrics and identifying areas for improvement. Continuous monitoring and improvement will ensure that the automation solution remains effective and efficient over time.

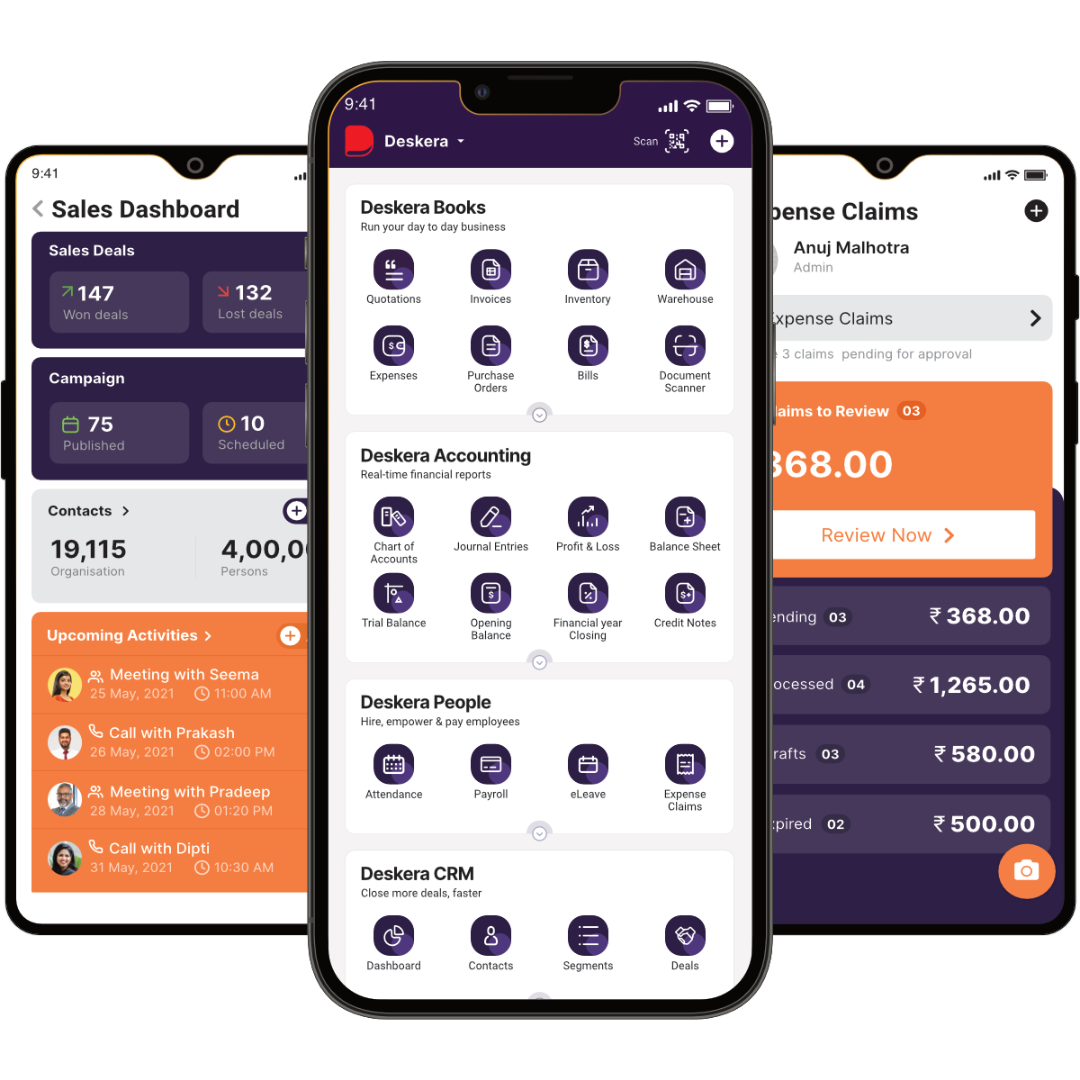

How Deskera Can Assist You?

Deskera ERP and MRP system can help you:

- Manage production plans

- Maintain Bill of Materials

- Generate detailed reports

- Create a custom dashboard

Deskera ERP is a comprehensive system that allows you to maintain inventory, manage suppliers, and track supply chain activity in real-time, as well as streamline a variety of other corporate operations.

Deskera MRP allows you to closely monitor the manufacturing process. From the bill of materials to the production planning features, the solution helps you stay on top of your game and keep your company's competitive edge.

Deskera Books enables you to manage your accounts and finances more effectively. Maintain sound accounting practices by automating accounting operations such as billing, invoicing, and payment processing.

Deskera CRM is a strong solution that manages your sales and assists you in closing agreements quickly. It not only allows you to do critical duties such as lead generation via email, but it also provides you with a comprehensive view of your sales funnel.

Deskera People is a simple tool for taking control of your human resource management functions. The technology not only speeds up payroll processing but also allows you to manage all other activities such as overtime, benefits, bonuses, training programs, and much more. This is your chance to grow your business, increase earnings, and improve the efficiency of the entire production process.

Conclusion

Finance departments can significantly benefit from automation in creating scalable and efficient processes. By leveraging automation technologies such as robotic process automation (RPA), artificial intelligence (AI), and machine learning (ML), finance departments can streamline and automate their routine tasks, reduce errors, and improve accuracy, speed, and efficiency.

Automation can also enable finance departments to access real-time financial data and insights, increase transparency, and enhance decision-making capabilities. Moreover, automation can help finance departments to optimize their resources, reduce costs, and increase productivity, allowing them to focus on strategic tasks and value-added activities.

However, implementing automation technologies requires careful planning, preparation, and execution, including assessing the organization's needs and goals, selecting the appropriate technology, training the workforce, and monitoring the performance and results.

Finance departments must also ensure that their automation processes comply with relevant regulations and standards and maintain the security and privacy of sensitive financial data. With the right strategy, mindset, and tools, finance departments can harness the power of automation to achieve scalable and sustainable success.

Key Takeaways

- Automating financial processes can help organizations achieve greater efficiency and productivity.

- Finance departments can leverage automation to create more scalable and standardized processes, reducing the need for manual intervention and minimizing errors.

- By automating repetitive tasks, finance professionals can focus on more strategic activities that add value to the business.

- Automation can help finance departments save time and money, allowing them to operate with greater agility and respond to changing market conditions more quickly.

- Finance departments can use automation to streamline processes such as invoice processing, accounts payable and receivable, financial reporting, and more.

- Automation can help finance departments meet regulatory compliance requirements by providing a complete and accurate audit trail of financial transactions.

- Finance departments can leverage automation to gain greater visibility into financial data, helping them make better decisions and improve financial performance.

- Implementing automation in finance departments requires a clear understanding of the organization's goals, processes, and technology infrastructure.

- Finance departments can start by automating simple and repetitive tasks and gradually move on to more complex processes as they gain experience.

- Finance departments must ensure that their automation tools integrate with existing systems and can be easily customized to meet the organization's specific needs.

Related Articles

Damini

Damini Deskera

Deskera Saurabh

Saurabh Deskera Content Team

Deskera Content Team