A bank reconciliation is a schedule that explains any discrepancies between the balance on the bank statement and the balance on your business's financial records.

Your business and the bank keep separate records of deposits, withdrawals, checks, and every other cash balance that flows in and out of the business. Hence, at least once a month, you're responsible for preparing a bank reconciliation to ensure that both of these independent sets of records align.

In this guide, we’ll walk you through all of the accounting information and steps you need to know, in order to prepare bank reconciliations for your business’s accounting.

Read along to learn about:

- What Is a Bank Reconciliation?

- Why Do Bank Reconciliations Matter?

- How to Do a Bank Reconciliation: Step-by-Step

- Bank Reconciliation with Deskera Books

- Frequently Asked Questions

What Is a Bank Reconciliation?

Bank reconciliation is the process of comparing your business’s financial records with your bank account statement. It can also be defined as the document or statement that outlines any differences between the transactions in your bank account and the accounts balances in your financial reports.

Either the case, the goal of a bank reconciliation remains the same: identifying accounting errors and fraudulent activity. These issues can be seen in the form of outstanding cash balances, duplicate or forgotten entries, incorrect financial transactions, and so forth.

When it comes to corporations and big companies, there’s usually an accounting department that’s already looking over numbers to make sure accounting reports match reality. In small business accounting, however, the responsibility usually falls upon the owner, who can either take on the job personally, outsource it to a bookkeeper, or automate it through accounting software.

It’s also important to note that you only need to do a bank reconciliation if you’re using accrual accounting. If you’re using cash accounting, it means you record every transaction simultaneously with the bank, so there can’t be any miscalculations and thus no need for reconciliation.

Want to learn which method is best to use, depending on your business’ size, industry, and long-term financial goals? Then, head over to our full guide on the basis of accounting for more.

Why Do Bank Reconciliations Matter?

1. To Keep Financial Reports Accurate

First and foremost, bank reconciliation matters because it helps you get a real view of your business’s finances. When you review your books, it’s important that what you’re reading reflects reality. Otherwise, you could end up spending cash you don’t own, or holding back from potential investments and financial growth. Frequent bank reconciliations confirm your accounts match up, which allows you to properly track your cash flow and as a result, make sensible financial decisions.

2. To Detect Fraud

Although bank reconciliation won’t stop fraud in its tracks, it can let you know whether it’s happened, as well as the when and where.

For instance, it may happen that you make an invoice payment to a supplier by check, and they tamper with it by increasing the withdrawal amount. This type of inconsistency would show up in your bank reconciliation statement.

Fraudulent activity can also happen if you’re in a partnership and share a joint account with your business partner. If, for example, they say they’ll withdraw money to pay for a business expense and take more than they journalize on the books, a bank reconciliation would instantly highlight that.

Pro-Tip:

Another way you can detect fraud within your business is by conducting regular auditing processes. Auditing involves examining and verifying your financial reports by checking receipts, conducting fieldwork testing, collecting information on internal control processes, and more.

Read our full guide on auditing, to learn everything you need to know about the auditing process, and how it can help your business remain credible in the marketplace.

3. To Stay on Top of Your Receivables

Accrual accounting and double-entry bookkeeping can be complex to implement - especially if you’re doing it without the help of software or a qualified professional.

It might happen that after providing a service or finishing a project, a client promises to send a check - so you debit cash, and then forget about their payment altogether. Even though your bookkeeping will show they paid, only through your bank reconciliation will you be able to notice that the client hasn’t sent any payment yet and that there’s a receivable pending. It can also happen that a client pays their dues, but you don’t receive a notification, or simply forget to journalize the transaction altogether.

Frequent bank reconciliations help you spot these types of errors, stay on top of your receivables, and make sure your outstanding invoices and bad debt expenses don’t spiral out of control.

If you want to learn how to prevent unrecoverable and defective payments and create an allowance for these doubtful accounts, check out our guide on bad debt expenses.

How to Do a Bank Reconciliation: Step-by-Step

When you use accounting software to reconcile your books, the software automates most of the work for you, saving you a great deal of time and effort. If you’re handling the process manually, however, you need to verify all of your sales, expenses, and other transactions, through a predefined, step-by-step process.

More specifically, follow these steps to do a bank reconciliation after you receive your financial records from the bank:

1. Compare Deposits

If you often make deposits into your bank account, it’s important that you compare your bank account deposits with those reported into your general ledger. Keep in mind that banks can make mistakes too, so make sure to check both documents for possible errors.

How you can do this is by first making sure that every deposit made during the period appears in both documents. Print out the documents, place checkmarks next to the deposits that agree both in the bank statement and in the company’s general ledger, and take note of any differences.

For whatever’s missing (or possibly duplicated), figure out if it was a sale, interest, refund, or something else, and then either enter it into your system or delete it.

Finally, check whether any amounts have been entered incorrectly. For instance, you could have made a deposit in the amount of $850, but your bank has accidently left off a zero, and recognized it as $85, instead. For any kind of similar mistake that could be on the bank’s behalf, you have to get in touch with them to get the error resolved.

If you can easily account for these discrepancies, there’s probably no need to worry - the bank will respond and fix the issue in a timely manner.

2. Compare Checks

If canceled checks (checks which are processed and paid by the bank) are part of the bank statement, compare them to the general ledger to ensure that both amounts agree. Then sort out the checks numerically and determine if any checks are still outstanding.

Outstanding checks are checks that have been issued by a depositor but have not been paid by the bank on which they are drawn. This happens because some checks can take several days to clear after they are deposited. Compare the check numbers that have cleared the bank with the check numbers issued by the company to determine the outstanding checks.

3. Compare Bank and Credit Memos

Confirm all debit and credit memos in the bank statement.

Debit memos show deductions for items such as service fees, NSF checks, safe-deposit box rent, and notes paid by the bank on behalf of the depositor. Whereas credit memos reflect additional payments for items such as notes collected by the bank for the depositor and wire transfers from another bank.

Verify if the bank debit and credit memos have already been recorded in your general ledger. Then, if necessary, make the appropriate journal entries for any unrecorded items in your company's books.

4. Compare the Balances

Once you’ve checked deposits, checks, and bank and credit memos, and made the appropriate adjusting entries, compare the ending balances in both statements to make sure everything is accurate. The adjusted amounts should be the same - if they are still not equal, the reconciliation process must be repeated.

At the very end, once the balances are equal and there aren’t any issues, you must prepare respective journal entries to reflect the changes to the balance sheet.

Bank Reconciliation with Deskera Books

Manually preparing a bank reconciliation monthly can become exhaustive and time-consuming fast. That’s why most businesses choose to invest in accounting software that automates almost every part of their bank reconciliation process.

With the Deskera Books platform, you’re able to make comparisons between the company’s sales and purchases and your bank record within seconds, without having to lift a finger.

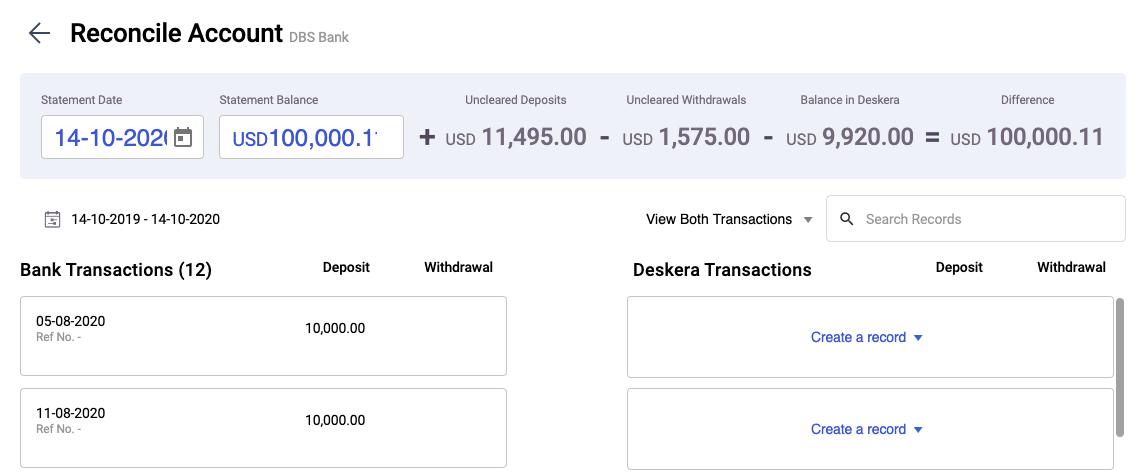

All you have to do is click on the "Bank" icon; and under the bank reconciliation tab, you can match the cash balances on the balance sheet to the corresponding amount of their bank statement, to check the differences between the two.

In the Bank reconciliation screen, you can view the following records on the statement date, statement balance, uncleared deposits, uncleared withdrawals, and the difference between the accounts.

Then, in case all entries are accurate, you can click on the Match button to reconcile the record. If you notice that an entry is missing, you can click on the create button to create a new deposit or payment entry to reconcile the account.

The automation of bank reconciliation is only one of the many features that come with the Deskera Books platform. The software allows you to keep track of your sales and business expenses, fill out invoices, pay bills, generate financial statements, and so much more, in just a few clicks.

You can even manage your entire bank reconciliation and bookkeeping from your phone, by simply downloading the Deskera mobile app.

Still not sure? Just try it out yourself using our completely free trial. No credit card required!

Frequently Asked Questions

#1: How Often Should You Reconcile Your Bank Account?

Ideally, you should perform a bank reconciliation every time your bank sends you a statement. This is typically done monthly, but it can also be done weekly, or even daily (if you’re a huge company that deals with hundreds of transactions per day).

Now, we know performing a reconciliation every single day can be time-consuming and costly to implement, hence, it’s recommended that all businesses do a bank reconciliation once a month.

#2: What Could Go Wrong in a Bank Reconciliation?

The most common types of discrepancies that come up through a bank reconciliation include:

- Accidentally Duplicated journal entries.

- Forgetting to record a transaction, also known as an error of omission.

- Entering a figure with the numbers in the wrong order.

- Debiting an account instead of crediting it, causing a reversal of entry error.

#3: How Many Types of Reconciliations Are There?

Generally, we divide reconciliations into five types: bank reconciliation, customer reconciliation, vendor reconciliation, intercompany reconciliation, and business-specific reconciliation.

Some other common reconciliations can include credit card, balance sheet, and cash reconciliations.

#4: What Are the Risks of Not Doing Bank Reconciliation?

Businesses that do not conduct regular bank reconciliations are vulnerable to fraud, unapproved withdrawals, and bank errors. If left unaddressed, these issues can result in cash flow leaks, which can obstruct business operations and growth.

Wrapping Up

And that’s a wrap!

Let’s recap with some of the main points we’ve covered:

- A bank reconciliation is a document that detects any differences between your bank statement and your accounting books. Its purpose is to keep your financial books accurate, detect fraud, and allow you to stay on top of your receivables.

- Generally, to manually manage bank reconciliation you have to compare the deposits, checks, bank, and credit memos in your general ledger, with those on your bank statement.

- You also have to make any appropriate adjustments, and then compare the ending balances to see if they are aligned.

- If everything equals, you can then prepare the necessary journal entries for any changes made.

- With accounting software like Deskera, you don’t have to worry about manually reconciling your books, as the platform automates almost every part of the process for you.

Related Articles