Introduced by the Indian Government, GSTR-6 is a type of GSTR form that helps to reduce tax evasion or corruption.

The GSTR-6 stands for Goods and Service Tax Return 6. It is a document/ statement that requires to be filed by organizations every month. Moreover, these organizations are also Input Service Distributors and need to furnish invoices details of form GSTR-6 on the GST Portal.

In addition, these returns must cover the crucial details of inward supplies received or purchased from other registered taxpayers (B2B). In addition, the input tax credit details must be distributed among organizations’ branches.

To learn about GSTR-6 thoroughly, we have curated this guide that will clear all your concepts related to GSTR-6. We’ll cover:

- Significance of GSTR-6

- Understanding Input Service Distribution (ISD)

- Prerequisites for filing GSTR-6

- GSTR-6 Due Dates

- Who Needs to File GSTR-6?

- How can you Revise GSTR-6?

- Significance of GSTR-6

- Details Required to Fill in GSTR-6

- Understanding GSTR-6A

- Frequently Asked Questions (FAQs) on GSTR-6

Significance of GSTR-6

GSTR-6 plays a significant role in preserving the tax system. Further, it covers all important details of the Input Tax Credit issued for distribution, as well as the method of distribution and the tax invoice on which credit has been received. Besides, even if it is a nil return, every ISD is required to file GSTR 6.

Understanding Input Service Distribution (ISD)

Input Service Distributor (ISD) is a GST-registered company that accepts invoices for services provided by its branches or other state units. In exchange, it issues ISD invoices outlining the division of taxes paid by each branch in proportion to the goods and services it receives.

Credit for central tax (CGST), state tax (SGST), integrated tax (IGST), or union territory tax (UTGST) on goods and services given by a supplier to a certain branch is among the tax credits offered.

However, the GSTINs of the branches can be different, but they must have the same PAN as the ISD.

Moreover, the return information is shared with the specific branch/recipient as a segment in the GSTR-2A return form. Furthermore, to claim credits, the receivers or the branch must submit these facts in the GSTR-2. It's also worth noting that ISD isn't required when submitting annual returns.

Prerequisites for filing GSTR-6

Check the following prerequisites required for filing GSTR-6. It includes:

- You must be a GST registered taxpayer with a GSTIN of 15 digits depending on your PAN.

- Your company's total revenue should be higher than 20 lakh rupees.

- This return is for all GST-registered input service distributors who have not chosen the Unique Identification Number (UIN) or composition scheme. Non-resident taxpayers are likewise exempt from filing this form.

- You must keep track of any taxable purchases implemented on behalf of your other establishments/branches by you (the ISD/head office). In addition, you must also document how you allocated the input tax credit you received on your purchases among your branches.

GSTR-6 Due Dates

The GSTR 6 form is due on the 13th of October 2021 for the month of September 2021. On the official GST Portal, Input Service Distributors (ISDs) can now fill out Form GSTR 6.

Who Needs to File GSTR-6?

An Input Service Distributor files GSTR 6, a monthly return form. Moreover, Input Service Distributors must fill out any information connected to ITC they have received and disbursed. GSTR 6 is a due date form with 11 components.

The Input Service Distributor includes the following:

How can you Revise GSTR-6?

There is no provision in the GST law for GSTR 6 to be revised. Any errors in the return can be fixed when you file GSTR 6 the following month.

Understanding GSTR-6A

GSTR 6A is a form that is automatically prepared based on the information submitted by an Input Service Distributor's suppliers in their GSTR 1. Moreover, the GSTR-6A form is a read-only version. Any adjustments to GSTR-6A must be made while filing GSTR-6.

Note that taxpayers are not required to file GSTR-6A. Also, it is a document that can only be read. GSTR-6A can be viewed by going to the GST Portal's Return Dashboard and clicking on the GSTR6A tile that says "PREPARE ONLINE."

Details Required to Fill in GSTR-6

The GSTR 6 format collects information on inward supply and ITC. Let's take a closer look at each section.

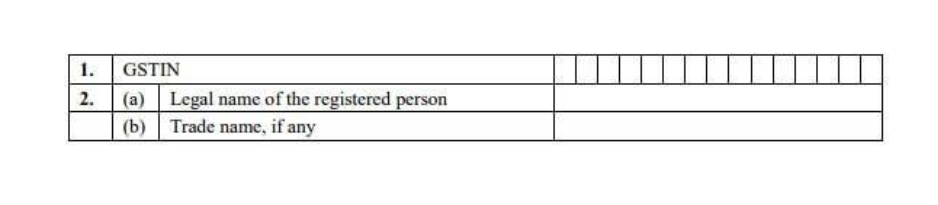

Table 1& 2: Information of the taxpayer

GSTIN – Enter your unique 15-digit Goods and Services Taxpayer Identification Number, which is based on your PAN (GSTIN).

Name of the Taxpayer — This form should contain the name of your company's registered taxpayer.

Period – (Month – Year) — Indicate the time period for which the GSTR-6 is being filed.

Table 3: Input tax credit received for distribution

ISD enters the data of the supplies received and the credit amount from a registered taxpayer into the system. Furthermore, the majority of the information, particularly inward supply details, is auto-populated from the counterparty's GSTR-1 and GSTR-5.

Moreover, the person must fill out all of the CGST/SGST and IGST credits. If the supplies were received in more than one lot, the taxpayer just needs to include the last lot information.

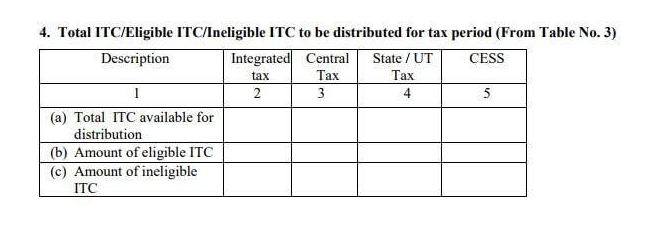

Table 4: Total ITC/Eligible ITC/ Ineligible ITC to be distributed for the tax period

In this segment, Table-3 auto-populates the information and fills in all of the information about the input tax credit, whether it's eligible or not.

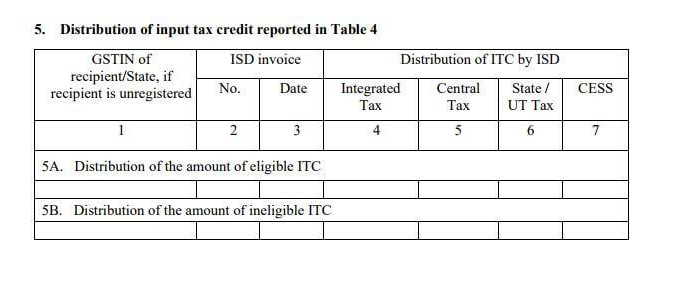

Table 5: Distribution of input tax credit reported in Table 4

This section contains information about available credit under the CGST, SGST, and IGST. Further, the information in this section pertains to the ITC listed in table-4. To fill in the fields, we must first fill in the invoice data.

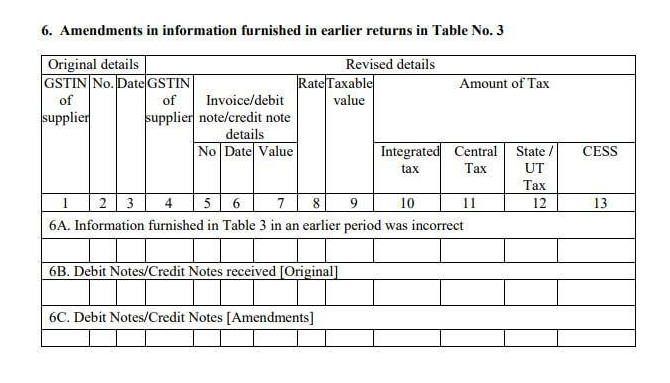

Table 6: Amendments in the information furnished in earlier returns in Table No. 3

It is possible to fix any errors in the invoice details for inward supplies provided in prior returns here. This is where you'll enter the details of any invoice adjustments you'll be making.

However, if there is any modification or alteration to the previous tax period, the taxpayer furnishes changed and revised invoices and information, as well as CGST/SGST and IGST charges.

Table 7: Input tax credit miss-matches and reclaims to be distributed in the tax period

This chart can be used to make modifications to the total ITC due to mismatch or the ITC regained due to mismatch correction.

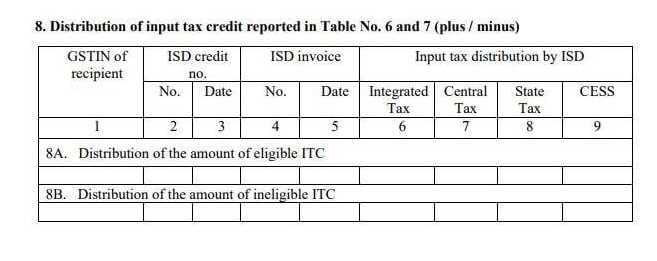

Table 8: Distribution of input tax credit reported in Table No. 6 and 7 (plus/minus)

Modification to the amount of credit issued to suppliers as a result of the information entered in Tables 6 and 7 can be implemented here.

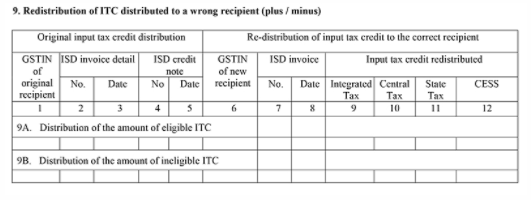

Table 9: Redistribution of ITC distributed to a wrong recipient (plus/minus)

Modifications to the amount of credit given to suppliers as a result of data in Tables 6 and 7 can be made here.

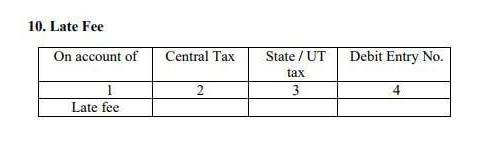

Table 10: Late Fees

If a late charge is due or has been paid, it is noted individually under this heading. If there is a late fee, the taxpayer puts in the details in the form.

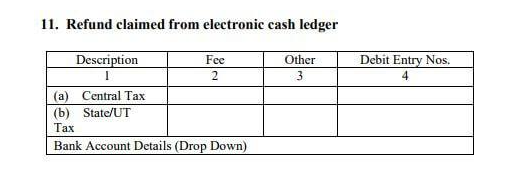

Table 11: Refund claimed from electronic cash ledger

It comprises the return amount as well as information from the electronic cash ledger, as the headline suggests.

Consequences of Delayed Filing of GSTR-6

If you file GSTR-6 late, you will be penalized with interest and late costs:

- Interest: You will be charged an additional 18 percent interest on top of the total tax amount owing for the month. The interest rate will increase by 4.93 percent for each delayed day.

- Late Fees: From the due date till the actual filing date, the taxpayer will be charged Rs. 50 each day. If you file your NIL return late, you will be penalized Rs. 20 each day.

Frequently Asked Questions (FAQs) on GSTR-6

Check the following frequently asked questions based on GSTR-6:

1. Is GSTR-6 mandatory?

Yes, it is compulsory to file GSTR-6 for those taxpayers who are registered as Input Service Distributors (ISD).

2. How Can I file the GSTR-6 form?

The GSTR-6 form is available through the GST Portal after logging in to the Returns Dashboard. Take a look at the following method:

3. Is there any offline method to file GSTR-6?

Yes, an offline mode is available to file GSTR-6.

4. Can the GSTR-6 filing date extend?

Yes, the Government is responsible to extend the filing date of GSTR-6 through notification.

5. What are the next steps after filing GSTR-6?

Check the following parts that come after the filing of GSTR-6:

- An ARN is generated after the completion of the GSTR-5 filing.

- The applicant receives the email or SMS on his/her registered mobile number for acknowledgment.

- If any addition or modifications are required to be made in GSTR-6 Form, then these details are auto-populated in the GSTR- 1/5 Form for correlative suppliers.

6. What includes different modes to file GSTR-6?

You have the choice to file GSTR-6 through EVC or DSC:

- Electronic Verification Code (EVC)

At the GST Portal, the Electronic Verification Code (EVC) is used to authenticate the user's identification. Further, EVC accomplishes this by producing a one-time password (OTP). Note that the OTP is sent to the Authorized Signatory's registered mobile phone number, which is listed in Part A of the Registration Application.

- Digital Signature Certificate (DSC)

The digital versions of paper or physical certificates signify Digital Signature Certificates (DSC). A digital certificate could be used to establish one's identity when provided online. It can also be used to access information or services available on the internet, as well as to digitally sign specific papers.

7. Do I have the option to preview the GSTR-6 before submission?

Yes, On the GST Portal, you can preview the GSTR-6 Form before submission

How Deskera Can Guide You?

Discover how you can combine accounting, finances, inventory, and much more, under one roof with Deskera Books. It's now easier than ever to manage your Journal entries and billings with Deskera. The remarkable features, such as adding products, services, and inventory, will all be available to you from one place.

Experience the ease of implementation of the tool and try it out to get a new perspective on your accounting system.

With the guiding and informative videos on how to manage and set up India GST, you can learn about and familiarize yourself with the process in just a few minutes.

Deskera Books is a time-saving strategy for managing your work contacts, invoicing, bills and expenses. In addition, opening balances can be imported and chart accounts can be created through it.

Deskera Books can handle every aspect of the organization, including inviting colleagues and accountants.

Key Takeaways

We have summarised the crucial key points from this comprehensive guide. Let’s have a look:

- GSTR-6 is a type of GSTR form that helps to reduce tax evasion or corruption.

- It is a document/ statement that requires to be filed by organizations every month.

- The GSTR 6 form is due on the 13th of October 2021 for the month of September 2021.

- An Input Service Distributor files GSTR 6, a monthly return form.

- There is no provision in the GST law for GSTR 6 to be revised.

- GSTR 6A is a form that is automatically prepared based on the information submitted by an Input Service Distributor's suppliers in their GSTR 1.

- Input Service Distributor (ISD) is a GST-registered company that accepts invoices for services provided by its branches or other state units.

- If you file GSTR-6 late, you will be penalized with interest and late costs.

Related Articles