GAAP, or generally accepted accounting principles, are a set of benchmarks that cover the intricacies, complexities, and technicalities of corporate accounting. It is a set of guidelines and regulations that businesses must adhere to when submitting financial information.

The Financial Accounting Standards Board (FASB) bases its broad selection of certified accounting methodologies on GAAP, also known as generally accepted accounting principles.

The purpose of these general accounting principles is to enhance the clarity, uniformity, and accuracy of financial information correspondence. Its ultimate goal is to make sure that an organization's financial statements are comparable, complete, and consistent.

Regardless of the type of industry that a business is in, these accounting principles reside at the core of all accounting information. Companies use it to compile and analyze financial data into accounting books.

Basics of Accounting Principles

The accounting principles of GAAP are merely a set of standards. Although its principles work to improve the transparency in financial statements, they do not provide any guarantee that a company's financial statements are free from errors or omissions that are intended to mislead investors.

It is for this reason that the Security and Exchanges Commission (SEC) has declared its intention to transition from GAAP to International Financial Reporting Standards (IFRS). However, they differ significantly from GAAP, and advancement in the pursuit of convergence and adoption has been stagnant for a while.

Even though the standards of GAAP are not regulated by the government, they exist as a result of the collaboration of the government and businesses. Although the usage of GAAP is not mandatory, the SEC requires that publicly traded and regulated businesses use and follow GAAP's standards for financial reporting.

The SEC holds businesses that issue stock to this standard, which necessitates annual external audit work by individual bookkeepers, but businesses that do not have external financiers are not required to follow this standard. Despite the mandate, however, the SEC is not responsible for the GAAP principles.

Rather, it is the Financial Accounting Standards Board (FASB) that actively enforces and influences changes in standards used for financial reporting at the corporate level. This responsibility lies with the FASB Advisory Council (FASAC), which advises the FASB on matters that may impact GAAP's accounting principles.

What Are Generally Accepted Accounting Principles?

The generally accepted accounting principles are a collection of authoritative guidelines and mostly unanimously accepted methods of recording and documenting financial information. Its goal is to enhance the clearness, uniformity, and reliability of financial information communication.

These accounting principles help to regulate the realm of accounting by establishing general principles and regulations. It aims to standardize and regulate accounting concepts, suppositions, and methodologies across all industry sectors. Accrual accounting, financial statement classification, and materiality are all covered within these principles.

GAAP's overarching objective is to guarantee that statements of financial position are comprehensive, coherent, and comparable. This makes things simpler for investors to analyze and derive insights from the company's balance sheet, such as historical trend data. It also makes it easier to compare financial data from different companies.

What Are the Principles of Accounting?

The best way to understand what GAAP and its requirements are about is to take a look at the various principles of accounting.

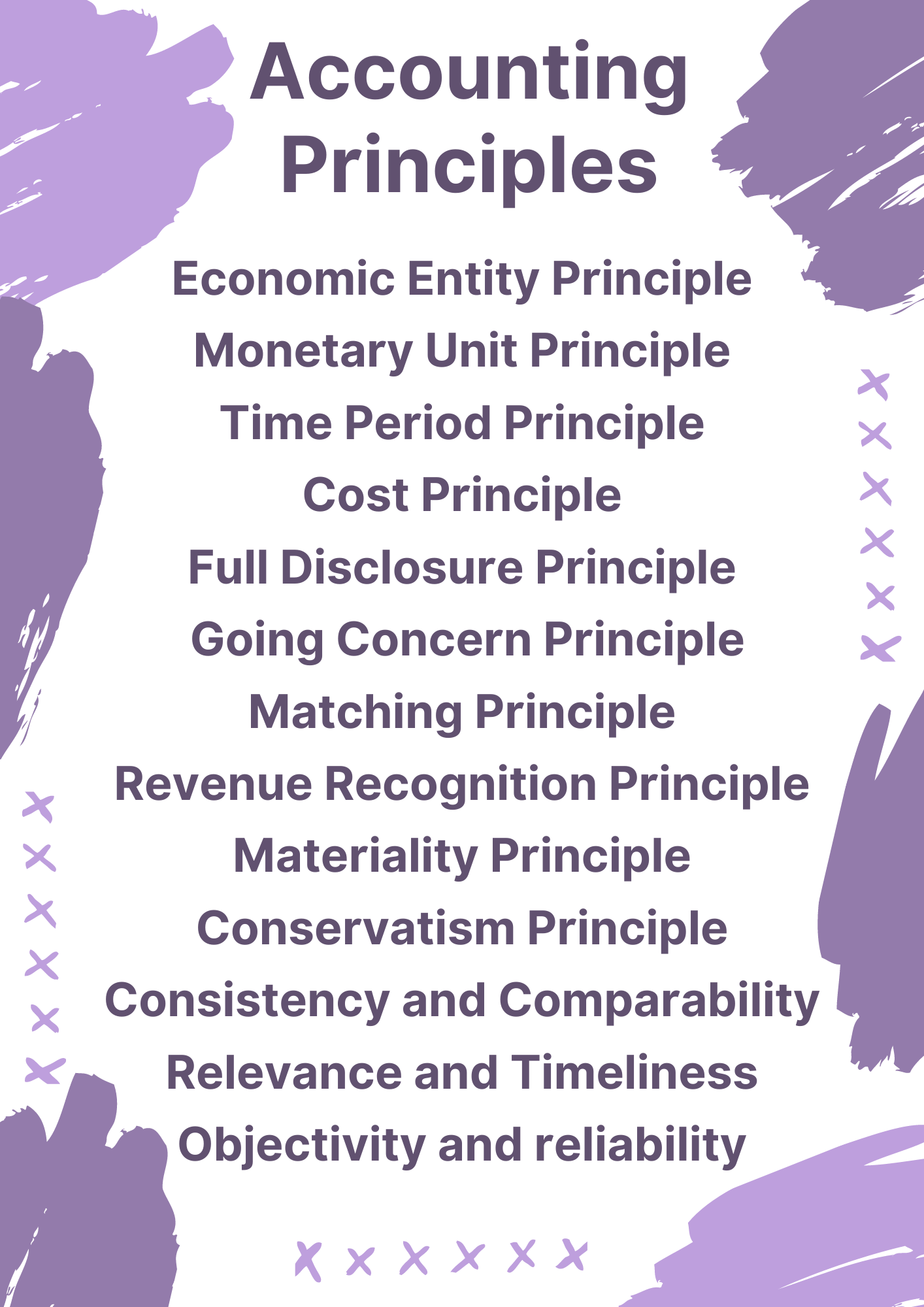

1. Economic Entity Principle

According to the principle of an economic entity, the documented activities of a commercial entity have to be stored separately from the documented activities of its owner(s) or other commercial entities. This indicates that you should maintain separate financial records and banking information for each entity and not combine the liabilities and assets of its owners or business associates with them. Furthermore, each financial transaction must be specifically associated with an entity.

2. Monetary Unit Principle

According to the monetary unit principle, you should only document commercial transactions that can be represented in terms of a monetary unit, such as currency. As a result, a company cannot identify non-quantifiable objects such as employee ability levels, service quality, or the R&D staff's ingenuity. Similarly, a company cannot quantify the financial value of a valuable speech offered to workers on how to participate in innovative activities.

3. Time Period Principle

The concept of the time period principle is that a company must submit the financial statements of its operations over a specified period, which is generally monthly, quarterly, or annually. Once the length of each reporting period has been determined, document transactions in each period in accordance with International Financial Reporting Standards or Generally Accepted Accounting Principles. A high level of commitment to consistency in documenting for the same time periods is required so that a company can generate financial statements that can be equated to previous years' results.

4. Cost Principle

The cost principle is an accrual basis of accounting that mandates the documenting of equity investments, liabilities, and assets on business statements at their original price. As per the cost principle, any monetary transactions should be recorded in accounting transactions at historical cost – that is, the initial purchase price at the time the resource was acquired – instead of its current valuation.

5. Full Disclosure Principle

The principle of full disclosure holds that in the event of a public company's filings, all necessary and pertinent knowledge for realizing a company's financial performance should be included. Financial analysts reading income statements, for instance, need to understand what asset pricing method was used, if any substantial write-downs occurred, how amortization is determined, and other important information for analyzing the financial statements.

6. Going Concern Principle

The going concern principle assumes that an entity will continue to operate for the foreseeable future. This, on the other hand, means that the company will not be compelled to cease activities and declare bankruptcy in the near future. By taking this supposition into account, the accountant is warranted in delaying the acknowledgment of certain expenses until a later period, whenever the entity is probably still in business and is making the best use of its assets.

7. Matching Principle

The matching principle states that any expenses incurred in a period are to be documented in the same timeframe as revenues earned. This principle acknowledges that organizations must incur expenditures in order to generate revenues.

The principle underpins the accrual basis of adjusting and accounting entries. The causality is at the heart of the matching principle. If there is no cause and effect, the auditor will instantly charge the cost to its expense.

8. Revenue Recognition Principle

According to the principle of revenue recognition, any income must be recorded when it is earned and not received. The revenue recognition concept is a component of accrual accounting, which means that when you start creating an invoice for a consumer for goods or services, the invoice amount is documented as revenue at that point, rather than when the transaction with the customer takes place.

9. Materiality Principle

According to the materiality principle, a policy of accounting policy can be neglected if the net effect on the accounting records is so minor that a viewer of the statements would not be misled. If an object is inconsequential, you are not needed to execute the regulations of an accounting standard under generally accepted accounting principles (GAAP). Because this connotation does not offer definitive guidance in differentiating material information from inconsequential information, determining whether a transaction is material requires judgement.

10. Conservatism Principle

The conservatism principle is the basic recognizing of liabilities and as early as possible when the result is ambiguous, but only recognizing earnings and investments once they are certain to be obtained. As a consequence, when given an option between several results with equal likelihood of occurring, you should acknowledge the transaction resulting in lower profit, or at least at the delay of a profit. Similarly, if an option of outcomes arises with an equal probability of impacting an asset's value, you should recognize the transaction resulting in reduced asset valuation.

11. Consistency and Comparability

Comparability is a qualitative feature that improves the usefulness of accounting information by allowing users to contrast performance and financial position across companies and time.

Consistency leads to comparability. Consistency refers to the enactment of accounting policies and standards on a regular basis from one period to the next and from one region to the next is referred to as consistency.

Comparability increases the relevance of accounting statements by allowing users to perform cross-trend analysis, cross-sectional analysis, and common-size analysis. Comparability is attained when organizations convey information in such a manner that the users involved can revise their accounting statements to make them comprehensible to other companies' financial information.

12. Relevance and Timeliness

Relevance refers to the idea that the data derived by an accounting information system should have an influence on the decision-making capabilities of someone who is reading the information. The notion can refer to the contents of the statement as well as its timeliness, both of which can influence decision-making.

Information that is delivered to users more rapidly, in particular, is regarded as having a higher level of relevance. This impact could plainly be to verify a decision that the peruser has already made, such as continuing to invest in companies, or it could be to make a new decision.

13. Objectivity and reliability

The financial reporting rule of the objectivity and reliability principle pertains to a company's financial statements' contents and declares that the information provided in accounting should be the most reliable and accurate information available.

In other words, accounting information must be relevant so that it is meaningful to managers, auditors, and stakeholders. Anything that can be considered valuable, crucial, timely, and comprehensible for decision-making - both internally and externally - is thought of as being relevant.

10 Principles of GAAP

GAAP is an attempt to standardize and regulate the assumptions, methods, and definitions used in accounting across different industries. There are 10 concepts behind the GAAP accounting principles:

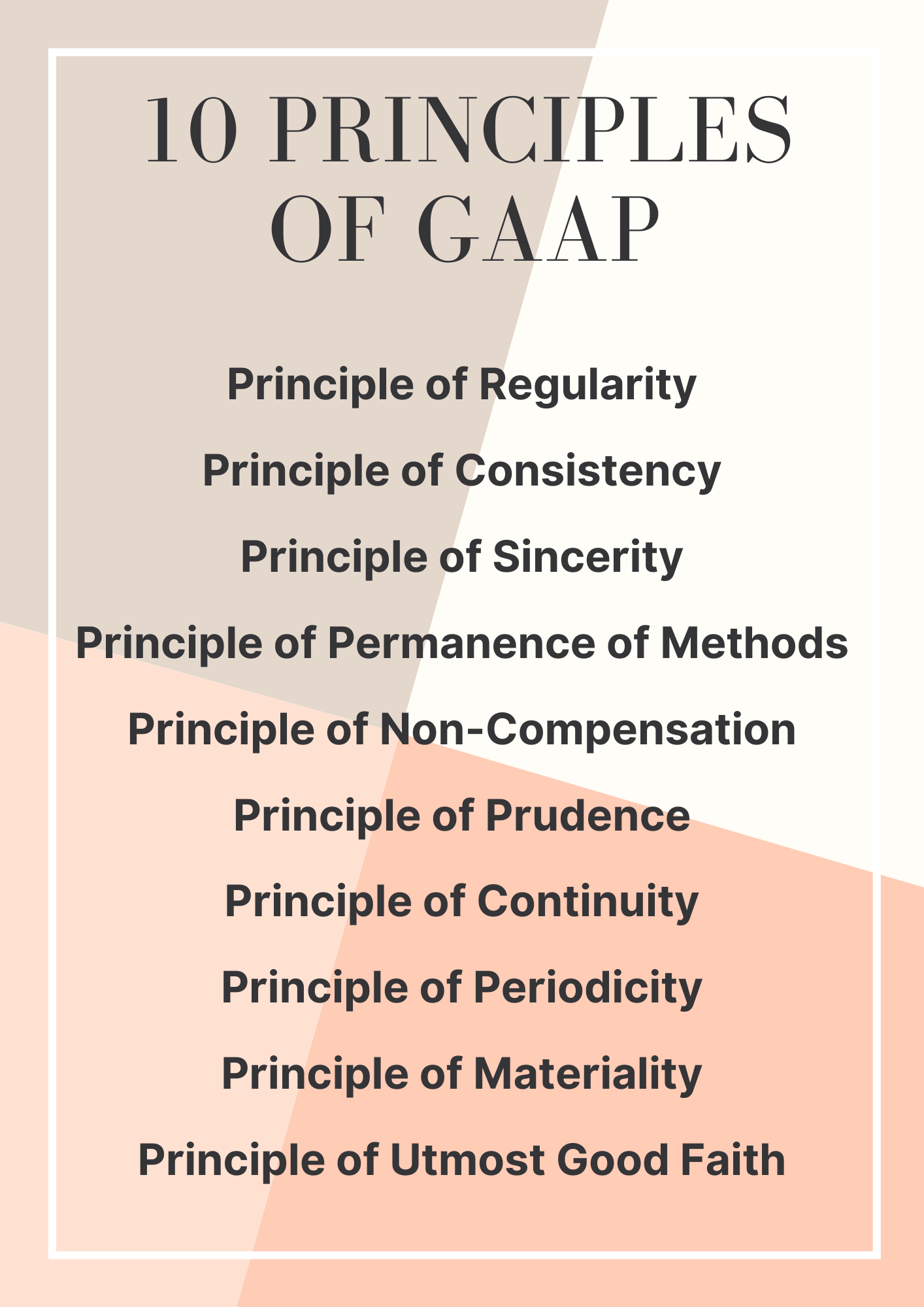

1. Principle of Regularity

This principle means that the accountant has conformed to GAAP's regulations as the standards completely.

2. Principle of Consistency

According to the consistency principle, once you've decided to adhere to an accounting principle or policy, you must stick to it completely and follow that method throughout your financial periods. For example, if you’re going to use U.S. GAAP for one aspect of your reporting, don’t switch to International Financial Reporting Standards (IFRS) later on.

3. Principle of Sincerity

This principle requires accountants to perform their jobs and report financial information with honesty and accuracy to offer an honest and objective representation of a business's financial situation.

4. Principle of Permanence of Methods

This principle states that an accountant's methods should never change and that GAAP should be applied consistently in all circumstances so that a business's accounting records can be easily contrasted to those of other businesses. Financial reporting procedures should be consistent so that the contents of the financial statement can be compared.

5. Principle of Non-Compensation

Accountants must show all positives and negatives of a business's worth in accounting records in order to display a complete picture of its worth. They are not permitted to conceal any information and are not permitted to obtain debt remuneration (compensation in stock or shareholding in a business) from a company.

6. Principle of Prudence

Accounting entries must be founded on facts rather than speculation. Through the methodologies of GAAP, accounting professionals must present a complete picture of a business's current valuation. They may not depend on pro forma accounting processes to forecast a business's future earnings.

7. Principle of Continuity

Accountants must price assets with the presumption that the business will continue to exist. This means that resources can be valued related to historical worth (original cost) instead of their current value (the amount it can be sold for at the present moment).

8. Principle of Periodicity

Accountants must use the accrual accounting method for recognizing revenue rather than the cash basis of accounting when preparing financial statements. The cash-basis process records earnings when it is obtained, whereas the accrual method records income when it is received. This is called the principle of periodicity.

9. Principle of Materiality

This principle allows accountants to deviate from other GAAP accounting regulations when the value in question is deemed inconsequential (makes no effect on the overall accounting picture).

10. Principle of Utmost Good Faith

This principle is derived from the Latin term "uberrimae fidei" is derived from the Latin phrase "uberrimae fidei." It implies that all sides associated with a transaction must be truthful and forthright in their business dealings.

Compliance with GAAP

If an organization's stock is traded publicly, its accounting statements must follow the rules laid down by the Securities and Exchange Commission's rules (SEC). The SEC mandates that publicly traded companies in the United States submit GAAP-compliant accounting statements on a periodic basis in order to continue to stay publicly listed on stock exchanges. An adequate inspector's opinion arising from an independent audit by an accredited accounting (CPA) firm ensures GAAP compliance.

Despite the fact that it is not needed for non-publicly traded companies, GAAP is regarded favorably by lenders and investors. When granting business loans, most institutions and banks will demand annual GAAP-compliant accounting statements as a component of their debt covenants. As a result, the majority of firms in the United States adhere to GAAP.

Investors should exercise caution if a financial report is not organized in accordance with GAAP. Without GAAP, contrasting economic statements of other organizations, even from the same sector, would be exceptionally hard, making direct comparison difficult. When submitting their financial results, some businesses may include both GAAP and non-GAAP metrics. Non-GAAP metrics must be defined in accounting records and other public disclosures, such as press releases, according to GAAP regulations.

The GAAP classification is intended to improve the standards of financial reporting. It is a template for choosing the precepts that accounting professionals should apply when trying to prepare financial statements in accordance with US GAAP. The following is a breakdown of the hierarchy:

- Declarations by the Accounting Research Bulletins and Financial Accounting Standards Board (FASB) and Accounting Principles Board viewpoints by the American Institute of Certified Public Accountants (AICPA).

- AICPA Industry Audit and Accounting Guides and Statements of Position and FASB Technical Bulletins.

- AICPA Accounting Standards Executive Committee Practice Bulletins, positions of the FASB Emerging Issues Task Force and subjects examined in EITF Abstracts Appendix D.

- AICPA Accounting Interpretations, FASB implementation guides, AICPA Industry Audit and Accounting Guides, Statements of Position that haven't been cleared by the FASB, and largely acknowledged and abided accounting practices.

How can Deskera Books Help Your Business

Take your business to the next level with Deskera All-in-One. It is a platform that offers Invoicing, Accounting, Inventory, CRM, HR & Payroll all under one roof. With Deskera books, you can keep track of your business cash flow and revenue using its financial reports.

Accounting can be easily managed Deskera Books and can help you keep track of your balance sheet, profit and loss statement and journal ledger. All this simplifies your accounting and tracking of your financial records, making it easy for your business to get business credit and to secure loans.

With Deskera Books, you can avail of online invoicing, accounting & inventory software to boost your business. It covers all the significant aspects of business such as billing, payments, warehouse management, Credit & Debit Notes, financial reports, an elaborate business dashboard apart from many other features.

Key Takeaways

GAAP is needed for all publicly listed companies in the United States, and it is also regularly followed by non-publicly publicly traded firms. Internationally, the International Financial Reporting Standards (IFRS) are issued by the International Accounting Standards Board (IASB).

The FASB and IASB occasionally collaborate to issue joint guidelines on crucial issues, but the United States has no plans to change to IFRS in the near future. However, while the goal of these GAAP principles is to ensure transparency, there is no assurance that the accounting information of companies adhering to these precepts is free of intended and unintended discrepancies. There have been numerous instances where businesses that adhere to GAAP distort figures in order to mislead stakeholders. Even if a company adheres to GAAP, it is always prudent to examine its financial statements.

Related Articles