The life of a business is divided into accounting periods, which is the time frame (usually a fiscal year) for which a business chooses to prepare its financial statements.

At the end of each accounting period, businesses need to make adjusting entries.

Adjusting entries update previously recorded journal entries, so that revenue and expenses are recognized at the time they occur.

For example, let’s assume that in December you bill a client for $1000 worth of service. They then pay you in January or February - after the previous accounting period has finished.

At first, you record the cash in December into accounts receivable as profit expected to be received in the future. Then, in February, when the client pays, an adjusting entry needs to be made to record the receivable as cash.

This type of adjusting entry is known as an accrued revenue.

In this guide, we will go through the details of all the different types of adjusting entries, their importance, and everything else you need to know about making adjusting entries for your small business accounting.

Read on to learn about:

- What Is an Adjusting Entry?

- The Importance of Adjusting Entries

- Types of Adjusting Entries

- 5+ Examples for Adjusting Entries

- Automate Adjusting Entries with Accounting Software

What Is an Adjusting Entry?

A crucial step of the accounting cycle is making adjusting entries at the end of each accounting period.

An adjusting entry is an entry made to assign the right amount of revenue and expenses to each accounting period. It updates previously recorded journal entries so that the financial statements at the end of the year are accurate and up-to-date.

To understand adjusting entries better, let’s check out an example.

Assume an automobile service shop offers their clients repair services in October, which they agree to pay for after three months.

In October, cash is recorded into accounts receivable as cash expected to be received. Then when the client sends payment in December, it’s time to make the adjusting entry.

The adjusting entry in this case is made to convert the receivable into revenue.

Now you may be wondering: why go through all this hassle? Why can’t businesses record cash once, when the client sends it?

There’s an accounting principle you have to comply with known as the matching principle. The matching principle says that revenue is recognized when earned and expenses when they occur (not when they’re paid).

This principle only applies to the accrual basis of accounting, however. If your business uses the cash basis method, there’s no need for adjusting entries.

If you haven’t decided whether to use cash or accrual basis as the timing of documentation for your small business accounting, our guide on the basis of accounting can help you decide.

The Importance of Adjusting Entries

When you make adjusting entries, you’re recording business transactions accurately in time.

This is extremely helpful in keeping track of your receivables and payables, as well as identifying the exact profit and loss of the business at the end of the fiscal year.

If you create financial statements without taking adjusting entries into consideration, the financial health of your business will be completely distorted. Net income and the owner's equity will be overstated, while expenses and liabilities understated.

That’s why using the accrual basis and adjusting entries is so important, and recommended by accounting and tax experts.

Types of Adjusting Entries

The amount of adjusting entries a business makes depends on their number of financial transactions. However, we divide adjusting entries into three main types: accruals, deferrals, and non-cash expenses.

Accruals

A business may earn revenue from selling a good or service during one accounting period, but not invoice the client or receive payment until a future accounting period. These earned but unrecognized revenues are adjusting entries recognized in accounting as accrued revenues.

You record accrued revenues by:

- Debiting the accounts receivable account and,

- Crediting the service revenue account.

Another type of accrual in accounting is the accrued expense. Accrued expenses are expenses made but that the business hasn’t paid for yet, such as salaries or interest expense.

They are recorded as an adjusting entry by:

- Debiting the expense account

- And crediting accounts payable.

If you want to learn more on how to pay back expenses owed to your suppliers in a timely manner, check out our business guide on invoice payments.

Deferrals

When your business makes an expense that will benefit more than one accounting period, such as paying insurance in advance for the year, this expense is recognized as a prepaid expense.

These prepayments are first recorded as assets, and as time passes by, they are expensed through adjusting entries.

The adjusting entry for prepaid expenses includes:

- A debit to the expense account (insurance expense, for example)

- A credit to prepaid expense account previously recorded.

The other deferral in accounting is the deferred revenue, which is an adjusting entry that converts liabilities to revenue.

More specifically, deferred revenue is revenue that a customer pays the business, for services that haven’t been received yet, such as yearly memberships and subscriptions.

When cash is received it’s recorded as a liability since it hasn’t been earned yet by the business. Over time, this liability is turned into revenue until it’s fully earned.

This change is done by recording the following adjusting entry:

- Debiting the unearned revenue account

- Crediting the service revenue account

Non-Cash Expenses

The most common method used to adjust non-cash expenses in business is depreciation.

By definition, depreciation is the allocation of the cost of a depreciable asset over the course of its useful life. Depreciable assets (also known as fixed assets) are physical objects a business owns that last over one accounting period, such as equipment, furniture, buildings, etc.

In simpler terms, depreciation is a way of devaluing objects that last longer than a year, so that they are expensed according to the time that they get used by the business (not when you pay for them).

For instance, if a company buys a building that’s expected to last for 10 years for $20,000, that $20,000 will be expensed throughout the entirety of the 10 years, rather than when the building is purchased.

And since depreciation doesn’t involve any actual cash exchange, it’s purely an estimate of how much a physical asset gets used in one accounting period. The most commonly used formula to estimate depreciation is by the straight-line method in which:

Depreciation (per accounting period) = Cost of the asset / Estimated Useful Life

The adjusting entry to record the depreciation expense includes:

- A debit to the depreciation expense account

- A credit to the accumulated depreciation account

Other methods that non-cash expenses can be adjusted through include amortization, depletion, stock-based compensation, etc.

5+ Examples for Adjusting Entries

Now that we know the different types of adjusting entries, let’s check out how they are recorded into the accounting books.

For the sake of our example, Company XYZ adjusts their accounts at the end of every month through the double-entry bookkeeping method. For the month of December, this is the information available to prepare adjusting entries:

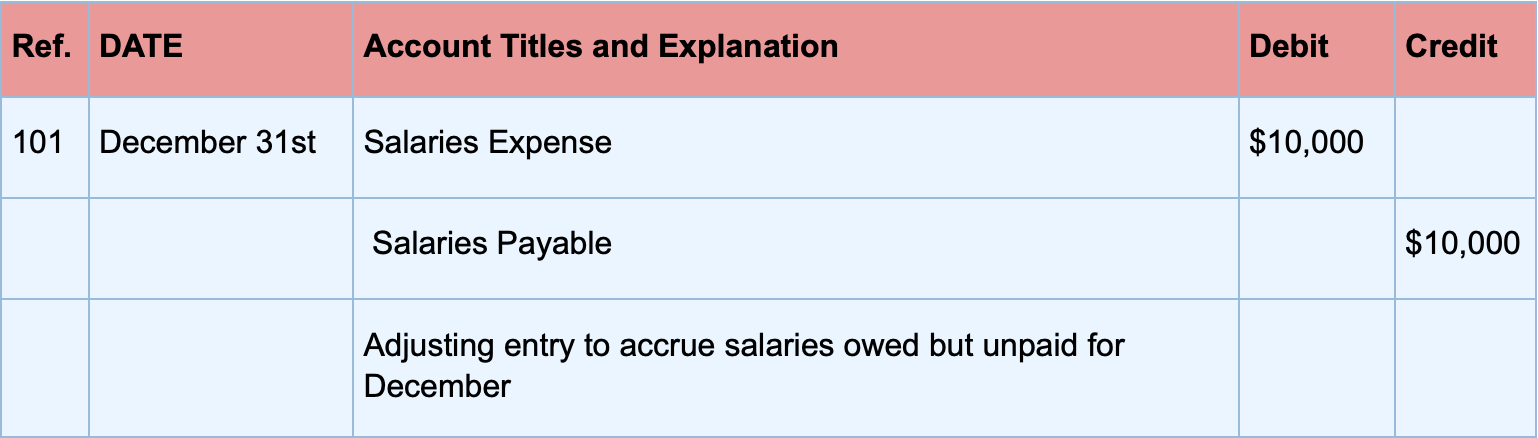

1. Salaries earned by the HR department employees that haven’t been recorded or paid yet, amount to $10,000. This is an accrued expense for which the following adjusting entry is made:

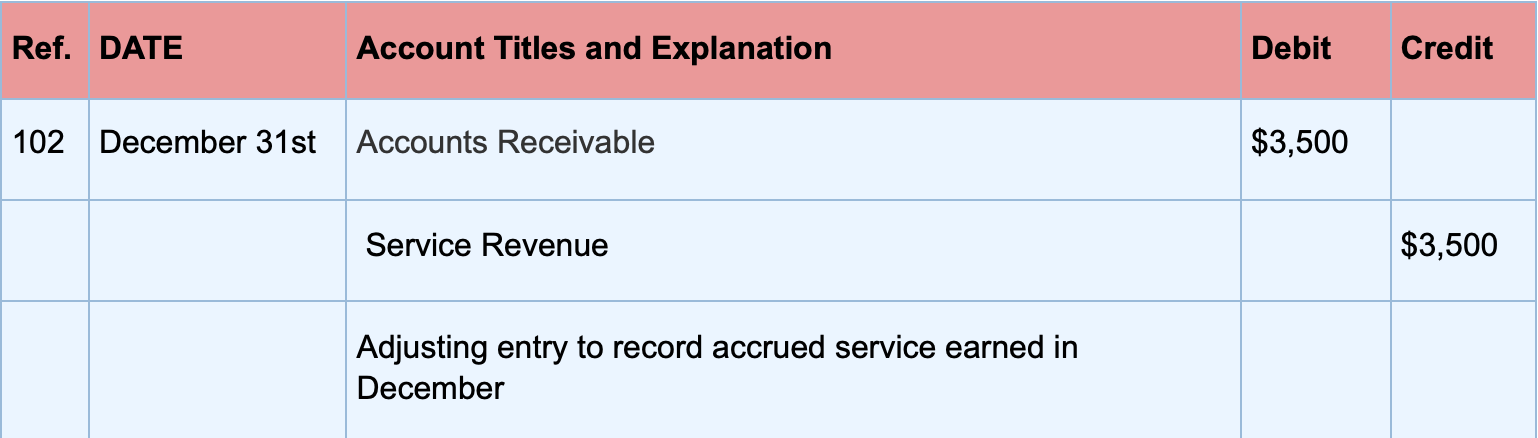

2. At the beginning of December, the company provided $3,500 worth of service that the customer will pay for next month. To record this accrued revenue, the resulting adjusting entry is made:

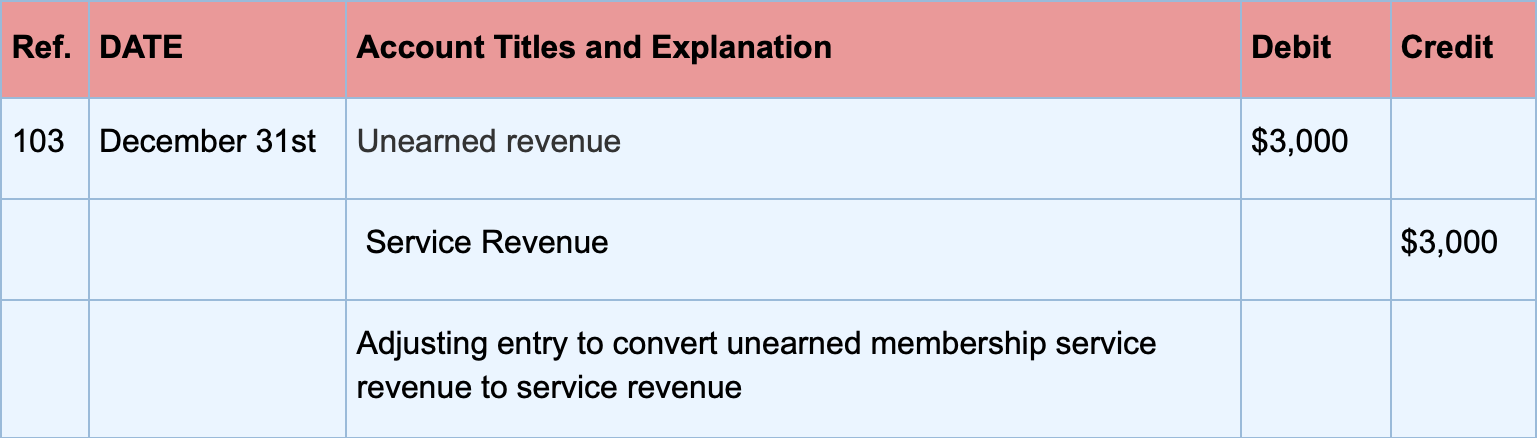

3. $3,000 of previously unearned fees from memberships in November have been earned. To convert this liability into revenue the following adjusting entry gets made:

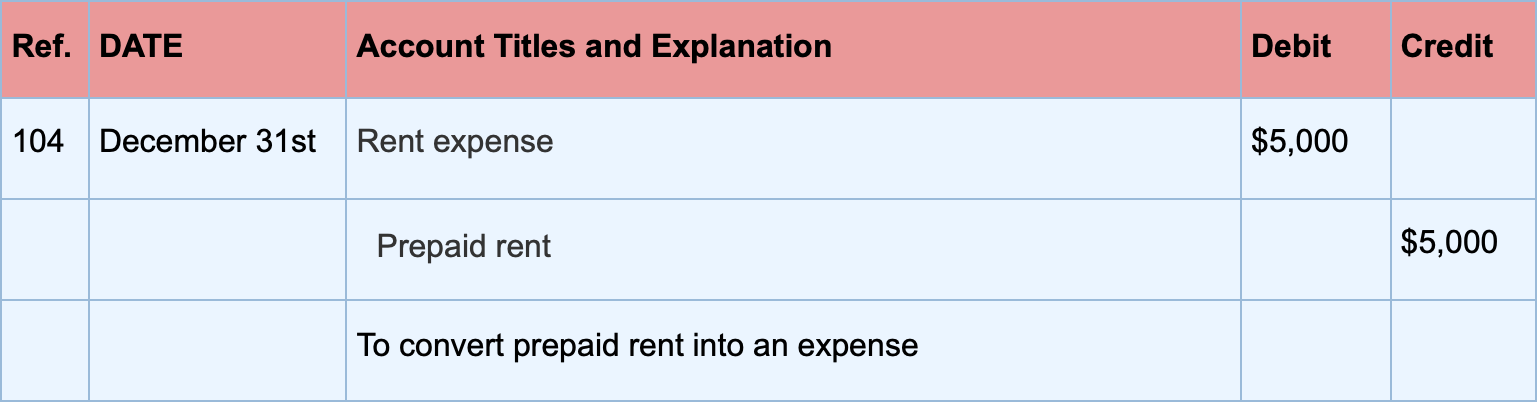

4. The company pays rent for their offices in advance on a quarterly basis for $15,000. For the month of December, rent expense would be $5,000 ($15,000/3 months). The following adjusting entry is made to convert prepaid rent for the month of December into an expense:

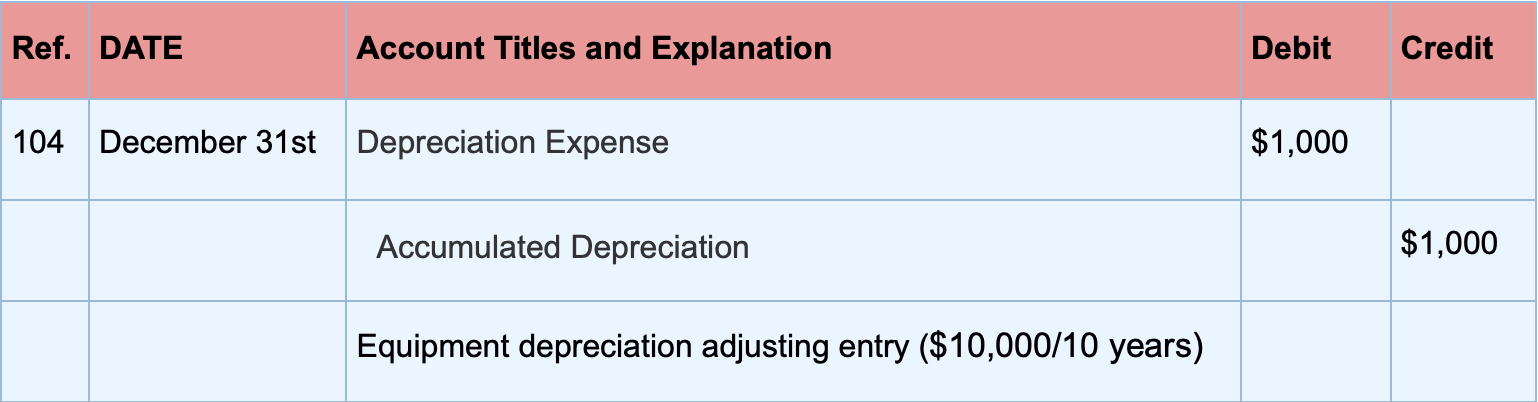

5. The original cost of the company’s equipment was $10,000, with an estimated 10-year life. Depreciation is recorded annually with the straight-line method, so on December 31st, the depreciation expense would be $1,000 ($10,000/10 years):

Want to learn more about recording transactions as debit and credit entries for your small business accounting? Head over to our guide on double-entry bookkeeping.

Automate Adjusting Entries with Cloud Accounting Software

Manually creating adjusting entries every accounting period can get tedious and time-consuming very fast. At the same time, managing accounting data by hand on spreadsheets is an old way of doing business, and prone to a ton of accounting errors.

That’s why most companies use cloud accounting software to streamline their adjusting entries and other financial transactions.

We at Deskera offer an intuitive, easy-to-use accounting software you can access from any device with an internet connection.

With the Deskera platform, your entire double-entry bookkeeping (including adjusting entries) can be automated in just a few clicks. Every time a sales invoice is issued, the appropriate journal entry is automatically created by the system to the corresponding receivable or sales account.

And through bank account integration, when the client pays their receivables, the software automatically creates the necessary adjusting entry to update previously recorded accounts.

The same process applies to recording accounts payable and business expenses.

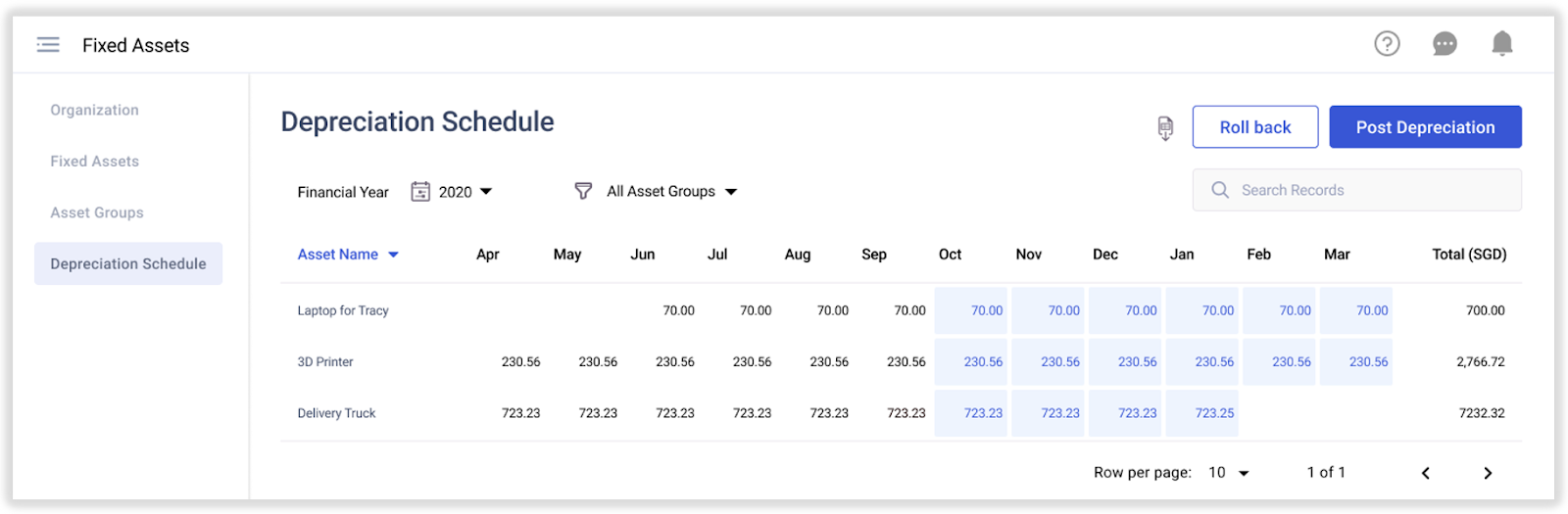

Deskera also allows you to automate non-cash expenses, with a Depreciation Schedule feature. All you have to do is select the asset name, method of depreciation, time period, and you’re done!

Press Post and watch your fixed assets automatically depreciate and adjust on their own.

Not convinced Deskera is the right choice for your business?

Luckily, you can check out the software yourself, by signing up for our free trial right away. No credit card details required!

Key Takeaways

And that’s a wrap!

For a quick recap, let’s go through the main points we’ve covered:

- Adjusting entries update previously recorded journal entries to match expenses and revenues with the accounting period that they occur. These entries are only made when using the accrual basis of accounting.

- There are three main types of adjusting entries: accruals, deferrals, and non-cash expenses.

- Accruals include accrued revenues and expenses.

- Deferrals can be prepaid expenses or deferred revenue.

- Non-cash expenses adjust tangible or intangible fixed assets through depreciation, depletion, etc.

- Use accounting software Deskera to automate your adjusting entries within seconds.

Related Articles