![Small Business Accounting Guide [Step-by-Step]](https://images.unsplash.com/photo-1556740772-1a741367b93e?ixlib=rb-1.2.1&q=80&fm=jpg&crop=entropy&cs=tinysrgb&w=2000&fit=max&ixid=eyJhcHBfaWQiOjExNzczfQ)

When running a small business, you’ll likely find yourself dealing with a ton of day-to-day administrative tasks like accounting.

As a business owner, accounting is probably the last thing you want to worry about.

However, maintaining proper accounting is important for your business to grow and succeed.

After all, a penny saved is a penny earned.

Even if you decide to hire a bookkeeper or a freelance accountant in the near future, it’s useful to know at least the essentials of accounting. This will help you track and run your business more efficiently.

In this guide, we cover everything you need to know in order to do accounting for your small business:

- What Is Small Business Accounting?

- Accounting Terminology & Financial Statements You Should Know

- Most Common Accounting Reports for a Small Business

- How to Do Accounting For Your Small Business (Step-by-Step)

- 9+ Essential Small Business Accounting Tips

- Small Business Accounting FAQ

What Is Small Business Accounting?

Small business accounting involves tracking all the money that flows in and out of your business accounts, summarizing that data into financial statements that can then be analyzed and used to improve the business.

As a small business owner, some of the most typical accounting activities you’ll find yourself doing are:

- Day-to-day bookkeeping

- Creating invoices

- Monitoring cash flow to cover all upcoming expenses.

- Keeping an eye on payables and receivables. It’s important to know whether your customers are paying you on time.

- Preparing financial statements and reports

- Filing for tax returns

Keeping track of all the above using different spreadsheets, or even physical folders can become time-consuming and tedious really fast. That's why many businesses also explore desktop application development services to create tailored accounting solutions that perfectly fit their specific needs.

That’s why most businesses nowadays use accounting software to automate most of their accounting activities.

Accounting software can be found either in the form of a desktop application or as a cloud-based app.

While both types of software help you carry out similar accounting operations, cloud-based accounting software gives you the added advantage of being able to access your accounting data whenever you want, on whichever device you want.

We’ll explain in more detail how you can use cloud accounting software to automate most of the accounting processes for your company. But before that, let’s go over some of the main accounting principles and terminology.

Accounting Terminology & Financial Statements You Should Know

The Accounting Equation

The accounting equation is one of the foundational principles of accounting. It dictates the relationship between the 3 main components of your business: Assets, Liabilities, and Equity.

Assets = Liabilities + Equity

Assets are what your business owns (resources of the business, such as cash or equipment)

Liabilities are what your business owes (i.e: your obligations, like wages, debt, or taxes)

The owner’s equity is what’s left after liabilities are subtracted from assets.

Double-Entry Bookkeeping

Double-entry bookkeeping is the most used method of accounting. In double-entry bookkeeping, for every business transaction that occurs, two entries are created: a debit and a credit entry.

As a result, changes are recorded on both two accounts.

Here’s a table that summarizes all that you need to know about debits & credits and the different account types:

Chart of Accounts

The chart of accounts is a list of all the different accounts, separated by type. Keep in mind that an account in bookkeeping does not signify a bank account.

Instead, an account is a record of all financial transactions for a certain type.

The 5 accounts used in accounting are the following:

- Assets - What your business owns (e.g: cash, inventory, accounts receivable, etc...)

- Liabilities - What your business owes (e.g: loans, accounts payable, etc…)

- Equity - This is what remains after the liabilities are subtracted from the assets (as per the accounting equation mentioned above)

- Revenue - What your business earns (e.g: revenue made through sales)

- Expenses - What your business pays to operate the business (e.g: payroll, rent)

Most Used Small Business Accounts By Types

The table below summarizes most of the accounts (and their types) that you might need to use while doing accounting for your small business. You can find the 8 most common accounts that any small business will have to use for their accounting highlighted in blue.

Most Common Accounting Reports for a Small Business

Recording data correctly is just the first step in doing accounting for your small business.

Then you have to compile all of that data into something more useful that can actually help your business make strategic decisions. That’s where accounting reports come into play.

Here are the most important accounting reports you’ll need to create for your small business.

Balance Sheet

The balance sheet provides a financial snapshot of your business at a specific date. It's the primary financial statement used by most small business owners.

While other financial statements report data for a period of time (a month, a quarter, or a year), the balance sheet reflects the company's financials standing at that specific instant.

In the balance sheet you’ll find the following information listed:

- Assets (what you own)

- Liabilities (what you owe)

- Equity (what's left)

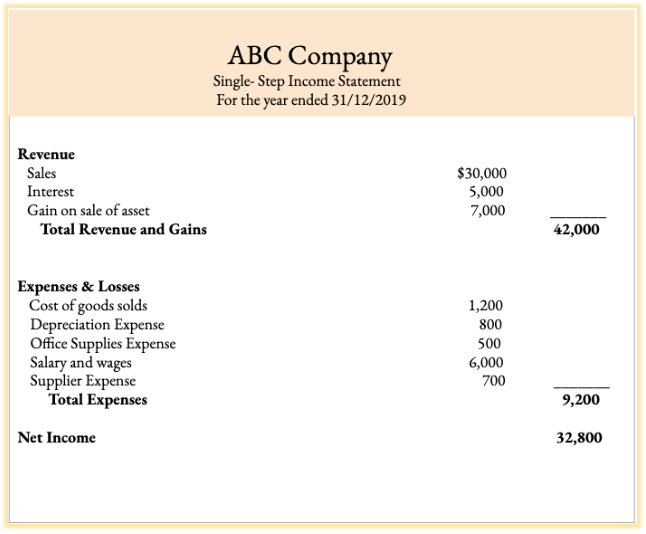

Income Statement (Profit & Loss Statement)

An income statement, also known as a profit & loss (P&L) statement shows you how your business performed during a period of time.

In the income statement you’ll list your:

- Sales

- Cost of sales

- Expenses

- Profit or losses over time

Here’s an example of an income statement:

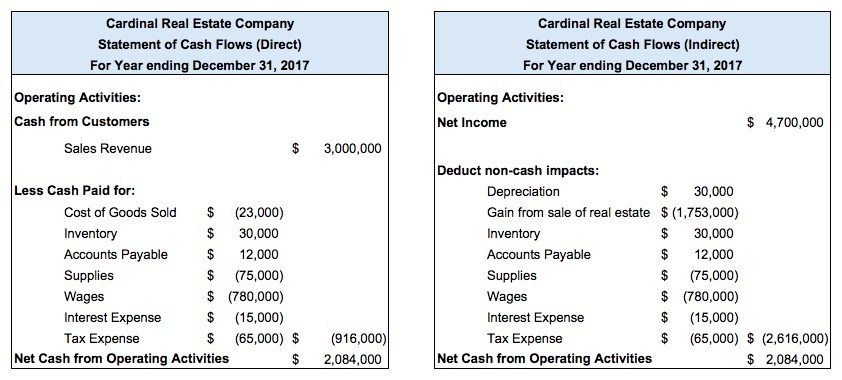

Cash Flow Statement

There are two types of cash flow reports, direct and indirect cash flow reporting.

The cash flow statement is made of three sections for different sets of activities: operating, financing, and investing.

The part of the cash flow statement that deals with direct and indirect cash flows is the operating activities one. Essentially, with direct cash flow reporting, the cash is shown based on the actual cash transactions.

Here’s what a cash flow statement example looks like:

Statement of Retained Earnings

Retained earnings are the sum of all profits and losses for the entire history of the company.

And similarly to the cash flow statement, most small businesses won't ever need to use a statement of retained earnings. Large publicly traded corporations generally rely on this financial statement to decide on things like dividends disbursements, company valuation, etc.

Here’s what a statement of retained earnings usually looks like:

How to Do Accounting For Your Small Business (Step-by-Step)

Choose an Accounting System

The number one thing you need to decide on when doing accounting for your small business is what kind of accounting system you’ll be using. Choosing an intuitive and easy-to-use system can help streamline your entire business accounting process, and save you tons of time.

Funnily enough, though, a lot of business owners think that using a checkbook is still an efficient way to manage their company’s accounting in 2021.

Realistically, it isn’t.

For starters, it can hinder your ability to grow your business. Organizing and maintaining an accurate record of all transactions will become harder and harder once you start scaling.

And if that’s not enough, think about the trouble you’ll have to go through when the IRS comes knocking on your door to collect taxes.

Nowadays, there are three main accounting systems you can use as a small business owner:

- Manual Systems (e.g: paper or spreadsheets) - You can organize the different accounts and financial reports in separate spreadsheets. However, you’ll have to track and input every transaction manually and ensure that everything balances out in the end.

- Automated Accounting Systems (e.g: accounting software) - Using accounting software, you can automate most accounting tasks like recording journal entries, calculating payments, or generating financial reports. Asides from saving your small business a ton of time, it will also increase your accounting accuracy.

- ERP (Enterprise Resource Planning) Software (e.g: SAP) - This type of software solution usually costs upwards of $10,000 monthly depending on your business needs. It’s mostly used by enterprises and is therefore not very relevant to small businesses.

Now you might be asking yourself. Why would anyone go for the manual system (spreadsheets), when one can use online accounting software instead?

Well, manual accounting systems are fine for very small businesses that have few to no employees and don’t deal with inventory. If all you care about is recording money that is flowing into and out of your business, then a simple spreadsheet will do the job.

For any other small business however, going for online accounting software will be the better choice. It will save you time, money, and it will also ensure that your records are always accurate.

One of the best accounting software for small business is Deskera.

Deskera is cloud-based accounting and bookkeeping software that integrates directly with your bank and payment providers.

Since it’s cloud-based, you can access your accounting information at any point in time, from any device that has internet connection. And if your business operations are mainly handled with mobile phones, then you can download the Deskera mobile app and manage all of your accounting from your phone!

Open a Business Bank Account

The first step after you’ve incorporated your business should be to open a business bank account.

It’s important that you separate your business’ finances from your personal finances.

For starters, it will be a lot simpler for you to keep track of how well your business is doing. And you’ll also save yourself a ton of time and nerves for when the time to file taxes comes.

Decide on a Bookkeeping Method

There are two main bookkeeping methods, single-entry bookkeeping and double entry-bookkeeping.

The main difference between the two is that single-entry bookkeeping only requires writing down a single entry for each business transaction you perform. This means that only one account is used.

Double-entry bookkeeping, on the other hand, contains two entries for each transaction, and two accounts are used. One of the accounts is debited and the other one is credited.

Additionally, single-entry bookkeeping is based on the cash-accounting method (it’s main focus is to record money when it is received, and payments when they are made).

Whereas double-entry bookkeeping is based on the accrual-accounting method. The accrual-accounting method records revenue when it is earned, instead of when it is received.

So, you might be wondering…

Which one bookkeeping method do you need for your small business accounting?

You should go for single-entry bookkeeping, if:

- Your business is really really small

- You can’t afford an accountant

- You don’t deal with inventory

- All your transactions are dealt in cash, and there are no sales or purchases done on credit.

That’s because the single-entry bookkeeping is a lot more simple and straightforward than the double-entry one.

However, if:

- You are serious about your business’ growth

- Your small business deals with inventory

- You want to find new ways to improve your business (make it leaner, find new opportunities)

- You want to keep accurate records of your business’ activities

Then you should go for double-entry bookkeeping.

Note: Companies that deal with inventory, that make more than $5 million a year, or that are likely to be audited, are required to follow the accrual-accounting method as required by the GAAP.

Track All of Your Business Expenses

Since the beginning of your business’ activity, you’ll have to track various transactions and expenses.

The most fundamental part of accounting, especially for a small business, is keeping accurate track of any cost that the business incurs.

As a business owner, this will help you to better analyze and monitor the growth of your business.

So, how do you track expenses?

- Keep every receipt in an organized folder or file.

- If you are using accounting software, then just store digital copies of all your receipts.

- Although the IRS says that there is no need to keep track of receipts under $75, it’s a good habit to just hold on to all receipts, with no exceptions.

What counts as a business expense?

- Business meeting in a cafe or restaurant. Requires details on who attended the meeting and for what purpose

- Out of town business travel. Again, requires details on the purpose of the business travel.

- Vehicle/gas expenses.

- Any inventory purchase.

- Office rent.

- Payroll.

- Home-office deductions. If you work from home, you can deduct part of your rent, electricity, internet, phone bill, etc...

All expenses are split in two different types of costs in accounting:

- Direct costs. These costs are directly related to providing your service or producing your product.

- Indirect costs. These are also known as overhead costs. These are costs that are not directly related to creating the product or service, but are needed to keep the company going.

Make Journal Entries

Whenever you make a business transaction, you need to record it. The process of recording all transactions is known as making journal entries.

All of these transactions are recorded in the general journal.

Now, journal entries follow the double-entry bookkeeping method that we described above. What this means is that for each journal entry, two accounts are affected at one time. One account is credited, and the other account is debited.

A journal entry is usually composed of the following columns:

- Reference number - a unique number to identify each transaction. This is also known as a journal entry number.

- Date of the journal entry - the date in which the journal entry was created

- Accounts - the two accounts that were affected by the transaction

- Debit - the amount that was debited

- Credit - the amount that was credited

- Journal entry description - the description of the journal entry. This has to be as descriptive and accurate as possible.

Journal Entry Example

Just for the sake of the example, let’s imagine that you decide to invest $5,000 of your own capital into your business.

In this case, the two accounts being affected are the owner’s equity account and the cash account. The cash account will be debited by $5,000, whereas the owner’s equity will be credited by $5,000.

Here’s what this would look like in practice:

PRO TIP

If you are using cloud accounting software like Deskera, then you can directly integrate your bank accounts and credit cards so that whenever you make an expense, the transaction is recorded automatically.

In practice, a journal entry is created, and it is automatically mapped to the correct ledger account. This way, you don’t even have to worry about manually creating each journal entry.

Setup Payroll

A company is nothing without its employees. Whether from the very beginning, or sometime down the line, you will have to hire employees.

As such, you’ll need to set up payroll.

And while hiring employees might seem easy at first, it's not. There are a ton of laws and regulations that you must learn and adhere to.

Here are the exact steps you need to follow to set up payroll:

- Check minimum wage laws & overtime regulations. Go on the Department of Labor website and on your state's website to check this information.

- Apply for an Employer Identification Number (EIN). Head over to the IRS website in order to apply for your EIN. You can use this number to identify your business to the IRS as a taxpayer and employer.

- Make sure to receive an I-9 Form from each employee before hiring them. The I-9 Form is a document that proves that the employee is legally able to work in the United States.

- Sign up at the Electronic Federal Taxpayer Payment System (EFTPS). This system allows you to pay your payroll taxes online. You have to make the employer tax payments every time you pay your employees - which can be semi-monthly, or monthly.

Keep in mind that if you are paying more than $50,000 in employment taxes in six months, then you have to make semi-monthly payments. - Keep track of the names, addresses, and how much you are paying each independent contractor. If your business is based in the US, you might need to file a form 1099 for each independent contractor at the end of the year.

Employee Benefits

Once you have hired your first employees, you'll need to figure out what kind of employee benefits your business can afford to offer.

Some typical employee benefits are:

- Medical insurance

- Dental insurance

- 401(k) retirement plans

- Disability insurance

Learn What the Different Employment Taxes Are

Types of Employment Taxes

- Federal Withholding Taxes - This is directly withheld from the employee's wage and paid to the IRS based on the wage.

- Social Security and Medicare Taxes - These are both paid to the IRS but calculated at different rates. The exact rates can be found on the IRS website.

- State Withholding Taxes - This depends on the state in which your business is located. Keep in mind that you have to file the necessary paperwork with your state's tax departments to pay employment taxes.

- Local Withholding Taxes - You'll also have to pay a tax (withheld from the employee's wage) based on the city or town where your business operates.

Types of Unemployment Taxes

Under the Federal Unemployment Tax Act, businesses pay unemployment taxes for workers that have lost their jobs.

These types of taxes are different from the above in that they are paid by you, the employer.

- Federal Unemployment Tax - Calculated quarterly and paid to the IRS once the amount reaches the minimum of $500.

- State Unemployment Tax - You need to calculate and pay this every quarter. The payment goes to your state tax department.

- Worker's Compensation Insurance - This is more of an insurance fund rather than a tax. It covers any injuries that may happen to employees at work.

Keep in mind that as an employer, you will likely have to pay both a federal and a state unemployment tax.

Does all of the above seem a bit complicated?

Luckily, you can use online software like Deskera to automate tax calculation for payroll and manage all of your payroll payments through an easy-to-use visual dashboard.

Deskera offers both accounting and HRIS software allowing you to manage your accounting and payroll, all in one place.

Figure Out How To Get Paid

The two main ways to get paid as a small business are either online or offline.

When we talk about offline payments, we are referring to payments done with a check, or cash.

Online payments on the other hand can be done via eWallets, credit cards, payment gateway providers, online bank transfers, and so on.

In this day and age, more and more businesses are switching from receiving payments offline to online.

In North America for example, the preferred payment method is credit cards - with around 34% of payments being carried out with a credit card.

Why do most businesses prefer getting paid online?

That’s because with online payments you can get paid faster, with lower fees, and from any country you deal business with. -

If you want to accept online or credit card payments, you can use either Stripe or Paypal. Stripe allows you to directly integrate any application for tracking invoices, expenses, and more.

However, keep in mind that both these payment providers have pretty high fees - around 3% of any transaction received.

Finally, if you are using Shopify, you can simply use Shopify Payments to receive credit card payments. Depending on your Shopify plan, you’ll have to pay between 2.4% and 2.9% in fees for receiving credit card payments.

Borrowing Money or Raising Funds

When starting your small business, chances are that you will need to borrow money at some point. It can be either to buy inventory, to expand, or whatever else.

As a given, it will be quite difficult to get a loan directly from the bank when you are just starting out.

Initially to raise funds, you might rely more on more accessible options like your borrowing from the owner (you), your close circle of people, your family members, your credit cards, etc.

Whatever the origin of the borrowed money might be, you need to create a legal promissory note stating the amount that was borrowed, any interest that needs to be paid, and the due date for the payment.

If you use your business credit card to make a purchase for office equipment, for example, this counts as a form of borrowing, since you’ll have to pay an interest to the credit card company in case you don’t have enough money to pay off the borrowed amount each month.

Build Business Credit

A ton of small businesses nowadays can benefit from building their business credit, as it can open up a lot of new funding opportunities in the future.

To build your business credit, here’s what you have to do:

- Establish and maintain good relations with vendors. The better your relationship with vendors, the higher the chances of you avoiding to pay upfront for the goods or services.

Your goal should be to establish a line of credit or invoice payment terms like net-30 or net-60 with vendors that report those payments to business financial reporting authorities.

This way you’ll manage to build a positive business credit history. - Get a business credit card. Especially if you own an e-commerce business or a dropshipping store, you have to get a business credit card. You can use the credit card to pay for things like inventory or any other business expenses.

The only thing you need to keep in mind, is to make sure to repay everything on time! - Make sure your personal credit is just as good. When borrowing money from a bank, your personal credit score will matter just as much as your business credit score. Make sure to do all personal credit card repayments on time.

And that’s a wrap!

These are the 10 steps you need to follow in order to successfully do accounting for your small business. Below, you’ll find some frequently asked questions that small business owners have when it comes to accounting.

If you have any other questions which have not been included here, just let us know in the comments section below and we’ll try to respond as soon as possible.

9+ Essential Small Business Accounting Tips

- Create a separate drawer or folder for organizing and storing all of your small business’ legal agreements and financial documents (like invoices, receipts, contracts, etc…)

- Track any cash received from sales. Keep all the sales invoices!

- Track any cash spent on business expenses. Keep all the receipts!

- If you spend any of your personal money (or equipment) on the business, you need some record to verify that you actually contributed.

- Use a separate checking account for your business (separate from the personal one) to minimize the risk of debit card fraud and keep your business finances secure.

- Don’t use your personal credit card for business expenses. Instead, get a business credit card.

- Don’t pay for your personal expenses using your business checking account. In case you do, you’ll have to report it as an owner withdrawal.

- Get a Federal Taxpayer Identification Number (TIN). This way you won’t need to use your Social Security Number every time you are asked for verification.

- Keep and hold on to ALL kinds of invoices and receipts. Yes, even the ones that are under $75. It will be a lot easier to balance your accounts if you keep copies of every transaction.

Small Business Accounting FAQ

Do I need an accountant for my small business?

For most small businesses out there, the answer is no.

If you are a small business, chances are you don’t actually need to hire an accountant. You can use online accounting software to automate most of your accounting tasks, at a fraction of the cost of an accountant or a CPA.

How much does an accountant cost for a small business?

The cost of an accountant for a small business will depend on many factors. However, if you decide to hire an in-house US accountant, based on the US Labor Statistics, you’ll be paying around $70,000 a year.

If you decide to outsource your small business accounting to a contractor or external firm, then you’d still be paying several hundred or thousand dollars a month.

On the other hand, if you use online accounting software, you can automate parts of your accounting process , while retaining full control over it, at a fraction of the cost.

How do you keep accounting records for a small business?

If you are using accounting software like Deskera, then keeping accounting records for your small business will be extremely easy. All you have to do is integrate your bank and payment providers with Deskera.

When your business creates an invoice, the corresponding journal entry is automatically added by the system in the respective ledger for Accounts Receivable, Sales, Sales Tax, etc…

Similarly, whenever you make an expense, the journal entry is automatically created, and it is mapped to the correct ledger account.

When a payment is processed, the bank and the accounts receivable are adjusted automatically by the accounting software.

What’s the best accounting software for small business?

The best accounting software for small business is Deskera Books. Deskera is an intuitive, super easy-to-use cloud-based application - you can access it from any device that has an internet connection.

Deskera allows you to integrate your bank accounts directly in order to track payments and expenses automatically.

When creating an invoice, the software automatically creates the journal entry and maps it to the relevant accounts (accounts receivable, sales, etc.). Without you having to lift a finger.

Invoice creation is as easy as 1-2-3. You can start by using one of our professional templates, and customize it to your liking.

And to top it all off, it comes at a very affordable price - starting at $9 per month! Want to give it a try? Get your free trial now!

Which accounting software is best for a small business?

Most accounting software out there is either too expensive or lacking a ton of basic functionality.

If you opt in for desktop accounting software like SAP for example, you’ll end up paying a ton of money every month (upwards of $1,000-$5,000) for it. And for most small businesses, that’s not a viable option.

On the other hand, online accounting software like Quickbooks lacks some very basic features like dropship management, advanced inventory management, bill of materials, multiple warehouse management, etc.

So, we might be a bit biased, but we think that the best accounting software for a small business is Deskera Books. It starts with as little as $9 per user, per month, and you can have unlimited guests (you only pay for your admin users).

It fosters all of Deskera’s accounting automation functionality, and it even comes with a completely 100% free mobile application.

This way, you’ll be able to access your accounting records from any device.

Not sure yet?

Key Takeaways

And that’s a wrap. If you’ve made it this far, then you might be a bit overwhelmed by the amount of information in this guide.

So, to make your life easier, here are the main points we covered:

- Small business accounting involves tracking all the money that flows in and out of your business accounts.

- It also involves transforming that data into financial statements that can then be analyzed and used to improve the business.

Before jumping into the nits and grits of small business accounting, you should know the meaning of the following terms:

- Accounting equation -> Assets + Liabilities = Equity

- Double-entry bookkeeping -> for each transaction two accounts are affected (one is debited and the other one is credited)

- Chart of accounts -> a list of all the different accounts, split by their type

The most important financial reports you should know are:

- Balance Sheet

- Income Statement

- Cash Flow Statement

- Statement of Retained Earnings

And finally, the steps you need to follow in order to do accounting for your small business, are the following:

- Choose an accounting system

- Open a business bank account

- Decide on a bookkeeping method

- Track all of your business expenses

- Make journal entries

- Setup payroll

- Learn what the different employment taxes are

- Figure out how to get paid

- How to borrow or raise money

- Build business credit

Related Articles