In bookkeeping every financial transaction, whether it’s a sale of merchandise, purchase of equipment, or capital investment, affects the accounts of a business.

These specific changes in accounts from financial activity, are collected into one document called the general ledger.

By definition, the general ledger is the main record-keeping system of a company’s financial transactions. The document holds crucial information needed to prepare financial statements at the end of the year.

This guide will provide you with a detailed definition of the general ledger, how it works, why it’s important, and everything else you need to know to create a general ledger for your small business accounting.

Read along to learn about:

- What Is a General Ledger?

- Why Is a General Ledger Important?

- General Ledger vs General Journal

- How Does a General Ledger Work?

- General Ledger Examples

- Automate Your General Ledger with Accounting Software

- General Ledger FAQ

What Is a General Ledger?

The general ledger is a record-keeping system of all the financial transactions of a business, organized into accounts.

These accounts aren’t related to bank accounts, savings accounts, or other types of accounts used to manage liquid assets.

Accounts in bookkeeping, commonly known as t-accounts, refer to the records in the general ledger, which keep track of the increases and decreases in assets, liabilities, owner’s equity, revenue, and expenses.

So, in other words, the general ledger keeps track of what is going on with every transaction of the business. This is exactly why the document is also considered the principal book of the accounting system and is used as a basis for the creation of accounting reports.

Want to learn how to streamline the step-by-step process of creating financial statements for your small business? Then, check out our complete guide on the accounting cycle.

Why Is a General Ledger Important?

Keeping an accurate summary of all your business’s transactions through a general ledger is one of the most crucial and beneficial practices in accounting.

First, a general ledger keeps tabs on all your profits, losses, and business’ overall health, providing you with real-time updates and helping you keep track of your business performance.

Secondly, this regular and well-organized documentation is extremely useful in spotting accounting errors, unusual transactions, or possible fraud. You can also use the report to reconcile the business’ accounts before creating financial statements, and ensure everything has been accurately recorded and is free of error.

This brings us to our third reason - the generation of financial statements. The general ledger summarizes key financial data that is later used to create the trial balance, as well as accounting reports at the end of an accounting period. These reports include the balance sheet, income statement, cash flow statement, and owner’s equity statement.

Lastly, once you have all of your revenue and expenses compiled into one document, filing for tax returns becomes twice as easy. When it’s time to complete tax forms, you can check your invoices against the general ledger to ensure everything is prepared correctly.

General Ledger vs General Journal

Transactions don’t immediately enter the general ledger when they occur. First, they’re translated into journal entries and posted into a company book called the general journal.

The general journal, or the book of original entry, keeps track of the raw business transactions by following a double-entry bookkeeping method. Through this method, for every recorded transaction, two accounts are simultaneously affected: one is debited and the other is credited.

Debit and credit are simply words that describe the double-sided nature of financial transactions. Debits are cash that flows into an account, whereas credits cash that flows out of it. You can learn how to use them to journalize your transactions, through our debit and credit guide.

Journal entries will also contain the date of the transaction, a reference number, and a description explaining what type of financial activity took place.

Once these entries are input into the journal, they can be posted into the general ledger. The general ledger summarizes and organizes the data by account.

So, there isn’t any date, detailed description, or reference number attached to each transaction. The debit and credit balances are simply organized according to their type of account.

How Does a General Ledger Work?

Every business has its own chart of accounts, depending on the type of financial activities it engages in, and how detailed it wants its ledger to be.

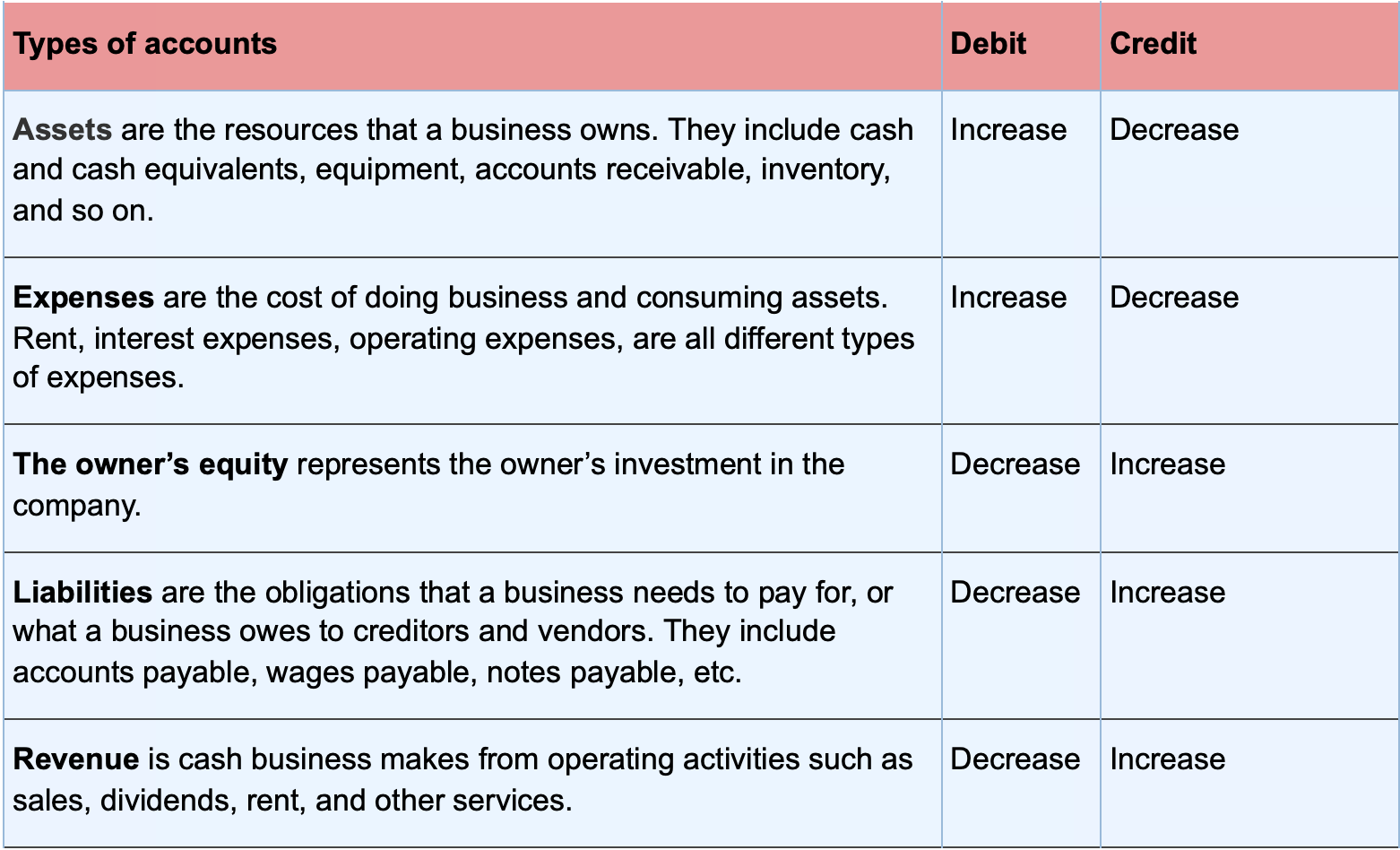

With that being said, the main account categories of the general ledger are five and include assets, expenses, the owner’s equity, liabilities, and revenue.

For easy access, we’ve made a cheat sheet describing each category, what sub-categories they typically include, and their corresponding debit and credit entries.

After you’ve assessed what debit and credit entry applies to each specific account and journalized your transactions, it’s time to create the general ledger accounts.

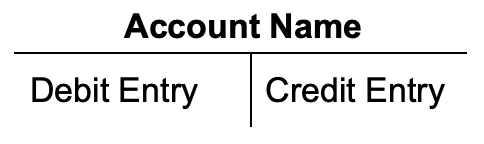

A ledger account, or T-account, visually look like the letter T and only has three main elements:

- The account name at the top of the letter T

- Debit entry on the right side

- Credit entry on the left side

To illustrate, this is how these account elements look like on the general ledger:

To better understand both debit and credit rules and how posting into the ledger is done, let’s check out a few practical business examples.

General Ledger Examples

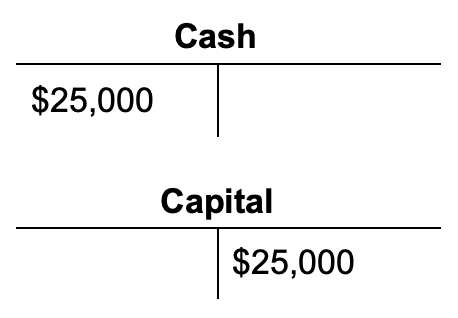

1. Owner’s Investment in the Business

Let’s assume the owner of a construction company invests $25,000 into his business.

This transaction causes a change into the ledger accounts:

- An increase in cash of $25,000

- An increase in the company capital of $25,000

Now, as cash is an asset - and we know from the debit and credit rule table that debits increase assets - the cash account will be debited for $25,000. Capital, on the other hand, is part of the owner’s equity and increases when credited, so it will be credited for that same amount.

The general ledger entries for these changes would look like this:

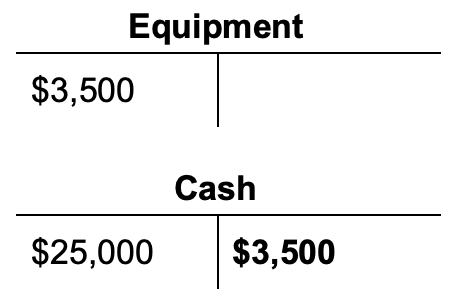

2. Purchase of an Asset

Now, the business owner purchases and pays for $3,500 worth of equipment.

The changes in accounts for this transaction are as follows:

- $3,500 increase in equipment or inventory

- $3,500 decrease in cash

Both accounts are assets, and as debits increase assets, and credits decrease them, equipment will be credited for $3,500, whereas cash will be debited for $3,500.

T-accounts would look as follows:

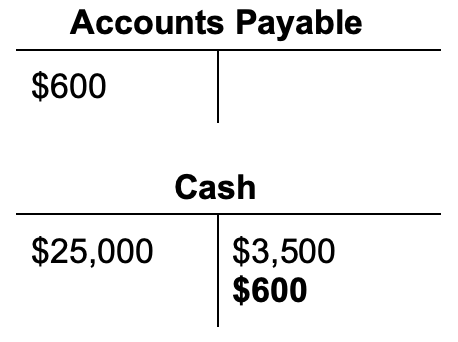

3. Payment of an Accounts Payable

Two weeks ago, the company purchased $600 worth of tools on account, with a net 30 payment term. Ten days later, the owner paid back the sales invoice.

In this financial transaction, we’re dealing with:

- A decrease in cash

- A decrease in accounts payable

Accounts payable is a liability account, meaning it decreases from a debit. Cash is an asset, and so it decreases from a credit.

So, the ledger accounts would be as follows:

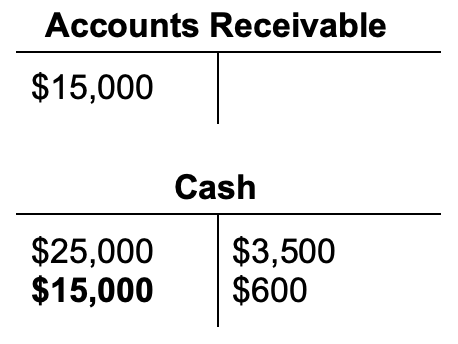

4. Collection of an Accounts Receivable

A month ago, the company renovated and remodeled a client’s apartment, for $15,000. They sent the invoice and offered the client 45 days to deposit the payment.

30 days later, the client made the complete invoice payment.

This transaction changes two asset accounts:

- Accounts receivable decreases by $15,000

- Cash increases by $15,000

As we already know, credits decrease assets, and debits increase them, so the two T accounts posted in the ledger would look like this:

For a more detailed guide and more examples on debit and credit entries, you can check out our post on journalizing transactions.

Automate Your General Ledger with Accounting Software

Manually journalizing transactions and updating the general ledger can easily turn time-consuming and tedious. Manual work is also prone to error, especially if you’re not a qualified accountant with sufficient knowledge of how bookkeeping is done.

That’s why most small businesses use accounting software to automate their general ledger and many other time-consuming financial procedures.

Now, we know what you may be thinking: isn’t accounting software complex and hard to understand on its own?

Well, that’s true for most of the accounting software online.

However, we at Deskera offer an intuitive and user-friendly platform for small business owners, that can be handled without any prior technical knowledge.

As you are creating invoices, making sales, paying back your vendors, Deskera instantly debits and credits the transaction values into mapped ledger accounts and updates your General Ledger in real-time. Without you having to lift a finger!

The software also gives you peace of mind by eliminating human error, and notifying you anytime there’s an imbalanced account or any other accounting errors.

The best part? Automation doesn’t end with the general ledger.

As the transaction data merges into the ledger accounts, their values will also automatically circulate to the respective financial reports. No more worrying about creating accounting reports at the end of an accounting period.

Deskera automatically generates your trial balance, income statement, balance sheet, and other financial documents instantly.

Deskera is accessible at any time, anywhere, from any device with an internet connection.

All you have to do is download the Deskera mobile app and sign up for the pricing plan that’s right for you.

You can even give the software a try out right away, with our completely free trial.

General Ledger FAQ

#1. How Many Types of Ledgers Are There?

There are three main types of ledgers in accounting, and they include the sales, purchase, and general ledger.

A sales ledger, or debtor’s ledger, groups all accounts related to credit sales and accounts receivable. A purchase ledger, or creditor’s ledger, accumulates all accounts’ payable balances.

Whereas the general ledger, as we’ve explained throughout our guide, is a centralized collection of all ledger accounts of a business. It contains assets, liabilities, revenues, expenses, and so on.

Now, keep in mind that if you’re running a small business that deals with few transactions, the accounts on the sales and purchase ledgers can be represented within the general ledger, without needing to be separate.

#2. What Is General Ledger Reconciliation?

A general ledger reconciliation is a process that involves reviewing your ledger to ensure transactions have been recorded and arranged correctly. This process is part of the year-end closing procedures and helps businesses cross-check for errors as well as submit accurate, legally compliant accounting reports.

If you want to learn more methods of preventing and managing mistakes in accounting, then head over to our guide on accounting errors.

Key Takeaways

And that’s a wrap! We hope you found our guide useful in understanding the accounting basics of the general ledger, and what steps you can take to create ledger accounts for your own business.

For a quick recap, here are some of the key points we’ve covered:

- The general ledger is a record-keeping document that summarizes the financial transactions of a business by account.

- The report is useful as it keeps track of the overall financial health of your business, eliminates error, aids in preparing financial statements, and makes tax filing twice as easy.

- Before a ledger is created, transactions are recorded as journal entries into the journal. Then, the entries with their debit and credit entries are posted into the ledger, according to their account.

- Every business has a different chart of accounts, however, the main account categories in bookkeeping include assets, liabilities, expenses, owner’s equity, and revenue.

- Each account, or T-account, has three main elements: an account name, debit entry on the right side, and a credit entry on the left.

- By automating your accounting with software like Deskera, you can generate your general ledger and overview your finances within seconds.

Related Articles