Every financial transaction goes through an accounting cycle: a multi-step process that records, summarizes, and organizes your transactions into financial statements.

After most of the cycle is completed and financial statements are generated, there’s one last step in the process known as closing your books.

Closing your accounting books consists of making closing entries to transfer temporary account balances into the business’ permanent accounts.

Now, if you’re new to accounting, you probably have a ton of questions.

What are temporary and permanent accounts? How can you use these accounts to make the appropriate closing entries? Why are closing entries necessary in the first place?

That’s exactly what we will be answering in this guide - along with the basics of properly creating closing entries for your small business accounting.

Here’s what the article covers:

- What Are Closing Entries?

- Temporary vs Permanent Accounts

- Recording a Closing Entry

- Automate Closing Entries with Deskera

- Closing Entries FAQ

What Are Closing Entries?

Closing entries are journal entries made at the end of an accounting period, that transfer temporary account balances into a permanent account.

The purpose of closing entries is to merge your accounts so you can determine your retained earnings. Retained earnings represent the amount your business owns after paying expenses and dividends for a specific time period.

This time period, called the accounting period, usually reflects one fiscal year. However, your business is also free to handle closing entries monthly, quarterly, or every six months.

Temporary vs Permanent Accounts

Temporary accounts include three accounts:

- Revenue

- Expenses

- Dividends

Accounts are considered “temporary” when they only accumulate transactions over one single accounting period. Temporary accounts are closed or zero-ed out so that their balances don’t get mixed up with those of the next year.

Permanent accounts represent balance sheet accounts, which include:

- Assets

- Liabilities

- Owner’s equity (or retained earnings)

These accounts carry balances that extend the one-year period. In other words, they represent the long-standing finances of your business.

When making closing entries, the revenue, expense, and dividend account balances are moved to the retained earnings permanent account. If you own a sole proprietorship, you have to close temporary accounts to the owner’s equity instead of retained earnings.

The Income Summary Account

As mentioned, one way to make closing entries is by directly closing the temporary balances to the equity or retained earnings account.

There is also a second way: creating an intermediate account called the income summary.

The income summary is a temporary account that carries the balances of the income statement accounts: revenue and expenses. Dividend expenses are not included, as they’re directly closed to retained earnings. Why?

Well, dividends are not part of the income statement because they are not considered an operating expense.

Instead, as a form of distribution of a firm’s accumulated earnings, dividends are treated as a distribution of equity of the business.

Thus, the income summary temporarily holds only revenue and expense balances.

Keep in mind, however, that this account is only purposeful for closing the books, and thus, it is not recorded into any accounting reports and has a zero balance at the end of the closing process.

Recording a Closing Entry

Now that we know the basics of closing entries, in theory, let’s go over the step-by-step process of the entire closing procedure through a practical business example.

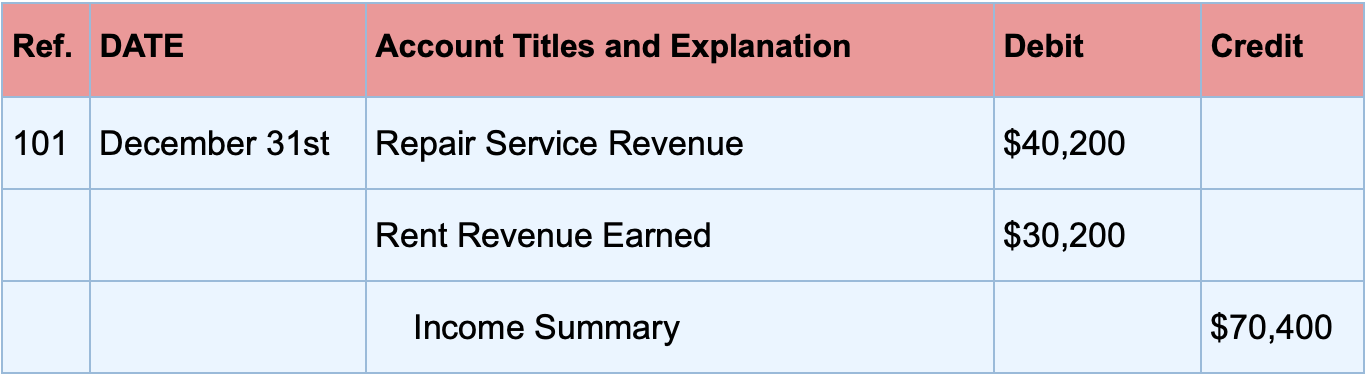

Step #1: Close Revenue Accounts

First, all the various revenue account balances are transferred to the temporary income summary account. This is done through a journal entry that debits revenue accounts and credits the income summary.

To illustrate, let’s assume Company XYZ uses two different revenue accounts: one for repair service revenue and one for rent revenue earned. The repair service revenue account has a credit balance of $40,200, whereas the rent revenue earned has a credit balance of $30,200.

Together, the accounts have a credit balance of $70,400. To close these accounts into income summary, the following journal entry needs to be made:

After this closing entry has been posted, each of these revenue accounts has a zero balance, whereas the Income Summary has a credit balance of $7,400.

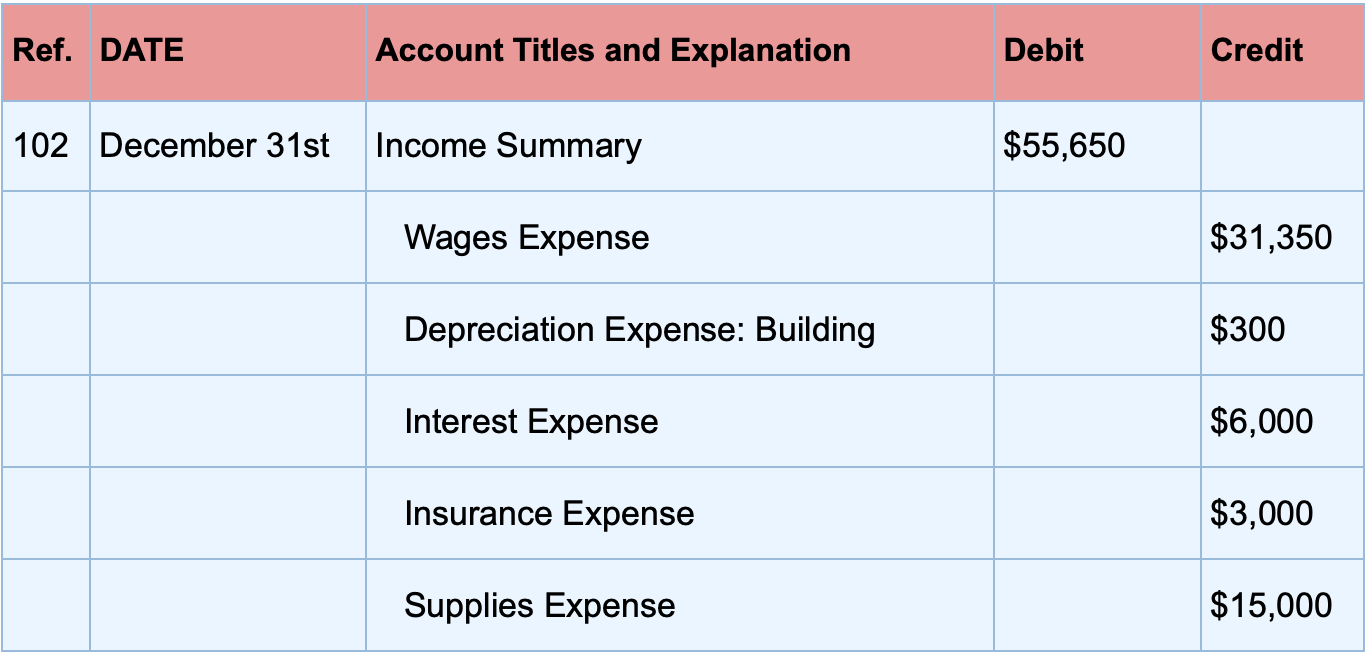

Step #2: Close Expense Accounts

Expense accounts have a debit balance, so you’ll have to credit their respective balances and debit income summary in order to close them.

As an example, let’s assume that Company XYZ has made the following expenses:

- Wages Expense $31,350

- Depreciation Expense: Building $300

- Interest Expense $6,000

- Insurance Expense $3,000

- Supplies Expense $15,000

For these expenses, the appropriate closing entries would be recorded as shown below:

After the posting of this closing entry, the income summary now has a credit balance of $14,750 ($70,400 credit posted minus the $55,650 debit posted).

This amount equals the annual net income for Company XYZ.

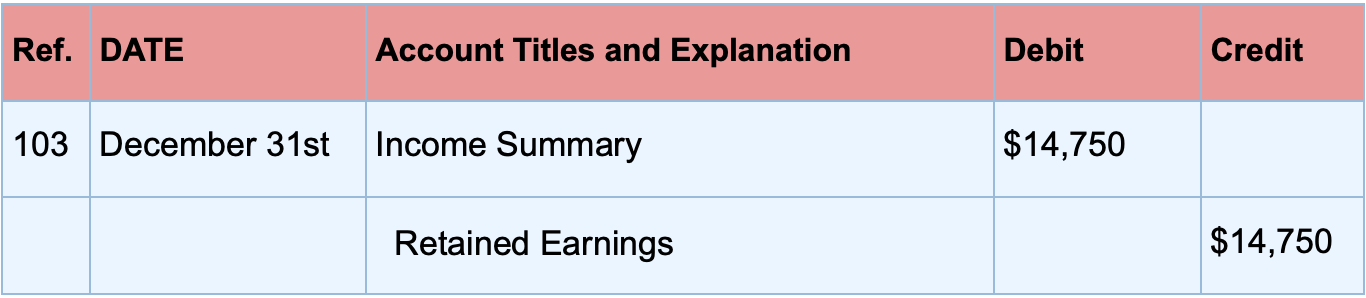

Step #3: Close Income Summary

Now, it’s time to close the income summary to the retained earnings (since we’re dealing with a company, not a small business or sole proprietorship).

The $14,750 credit balance is transferred to the retained earnings account with this closing entry:

Now, the income summary account has a zero balance, whereas net income for the year ended appears as an increase (or credit) of $14,750.

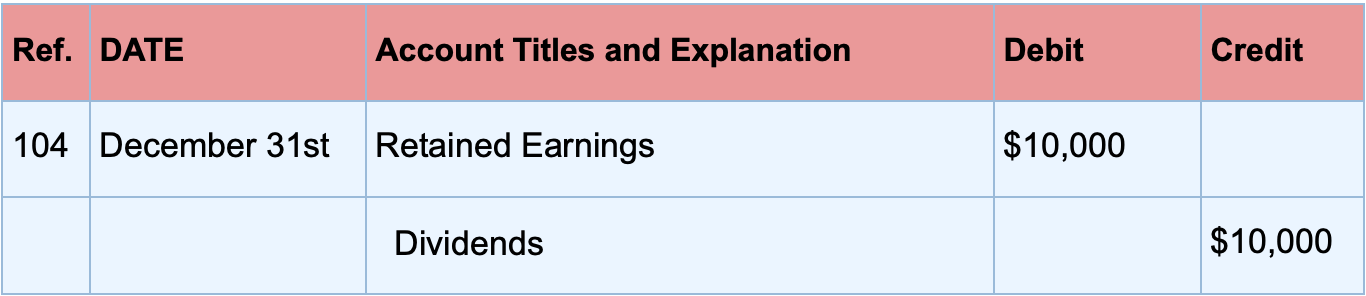

Step #4: Close Dividends

Lastly, if we’re dealing with a company that distributes dividends, we have to transfer these dividends directly to retained earnings.

To continue our example, let’s assume that dividends for Company XYZ equal to $10,000. To close this debit balance to retained earnings, the following journal entry needs to be made:

Now, the dividend account has a zero balance, and the retained earnings will have an ending credit balance of $4,750 (because dividends decrease retained earnings, so $14,750 previous balance minus $10,000 of dividends gives us $4,750).

Do you want to learn more about debit, credit entries, and how to record your journal entries properly? Then, head over to our guide on journalizing transactions, with definitions and examples for business.

Automate Closing Entries with Deskera

Manually creating your closing entries can be a tiresome and time-consuming process. And unless you’re extremely knowledgeable in how the accounting cycle works, it’s likely you’ll make a few accounting errors along the way.

That’s why most business owners avoid the struggle by investing in cloud accounting software instead.

We at Deskera offer the best accounting software for small businesses today. Our program is specifically developed for you to easily set up your closing process and initiate book closing within seconds - no prior technical knowledge necessary.

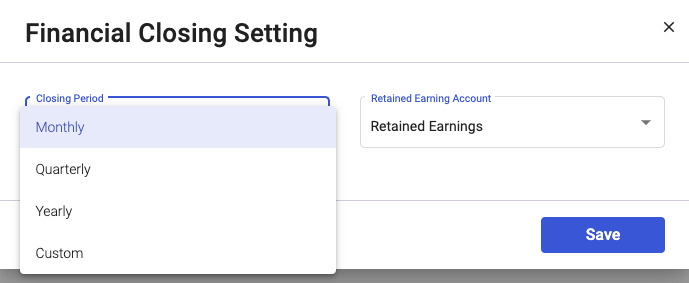

From the Deskera “Financial Year Closing” tab, you can easily choose the duration of your accounting closing period and the type of permanent account you’ll be closing your books to.

Then, just pick the specific date and year you want the closing process to take place, and you’re done! In just a few clicks, the entire financial year closing is streamlined for you.

As all of your financial data will already exist in the system, the account balances will be debited and credited accordingly by the software without you having to lift a finger!

The best part: Deskera is accessible any time, anywhere!

You can close your books, manage your accounting cycle, issue invoices, pay back vendor bills, and so much more, from any device with an internet connection, just by downloading the Deskera mobile app.

Give the software a try out right away, by signing up for our free trial.

Closing Entries FAQ

1. What’s the Difference Between a Closing Entry and an Adjusting Entry?

Adjusting entries are used to modify accounts so that they’re in compliance with the accrual concept of recording income and expenses.

Closing entries, on the other hand, are entries that close temporary ledger accounts and transfer their balances to permanent accounts.

Both entries are typically made at the end of the fiscal year.

2. What Happens If Closing Entries Are Not Made?

Failing to make a closing entry, or avoiding the closing process altogether, can cause a misreporting of the current period’s retained earnings. It can also create errors and financial mistakes in both the current and upcoming financial reports, of the next accounting period.

Key Takeaways

And that’s a wrap! We hope our guide was useful in understanding the closing process, and what steps you need to take to make year-end closing entries for your business.

For a quick recap, here are some of the main points we’ve covered today:

- Closing entries are journal entries created at the end of an accounting period to transfer your temporary account balances into one permanent account.

- The process is done so that you can determine how much retained earnings or owner’s equity you own, after expenses and/or dividends have been subtracted.

- Closing entries can either be made directly by closing temporary balances to the owner’s capital (or retained earnings) or through an intermediate account known as the income summary.

- More specifically, making closing entries through the income summary is a four-step process that includes:

- Closing revenue accounts to income summary

- Closing expense accounts to income summary

- Closing income summary to retained earnings

- Closing dividends to retained earnings

- To avoid the hassle of manually creating closing entries by hand, you can use accounting software like Deskera that lets you automate your entire closing process within seconds.

Related articles