Complicated, discretionary and burdensome, this is how most of the industry describes the Indian GST system. Inverted Duty Structure is one such component under GST that industries often find difficult to understand.

If you are also one of those who find Inverted Duty Structure slightly complicated to understand, this article will come handy to you. We will tell all you need to know about the Inverted Duty Structure under GST.

This article explores the following:

- What is Inverted Duty Structure?

- How was Inverted Duty Structure in the pre-GST world?

- What is Inverted Duty Structure in the post-GST world?

- Refund system in Inverted Duty Structure.

- How to calculate the maximum refund amount?

- Terms in computation of maximum refund amount you must know about.

- Steps to claim refund for Inverted Duty Structure.

- How to track refund application

Let’s delve right into it!

What is Inverted Duty Structure?

An inverted duty structure comes up in a situation where import duties on input goods are higher than on finished goods. In other words, the GST rate paid on purchases is more than the GST rate payable on sales.

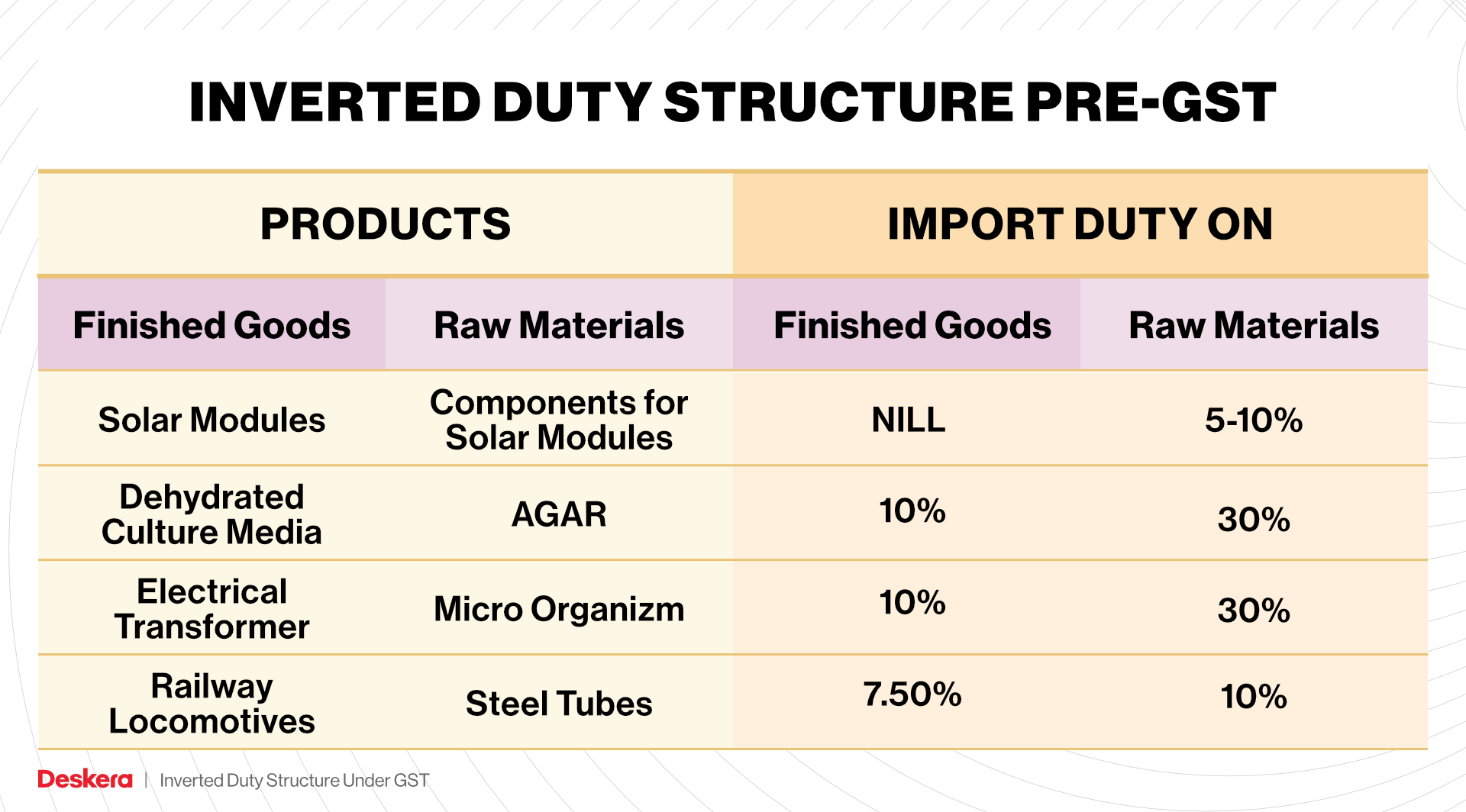

How was Inverted Duty Structure in the Pre-GST World

In the pre-GST world, inverted duty structure where import duty on raw materials that were used in the production of finished goods was higher than the import duty on finished goods itself.

If this was the case before the introduction of GST, let us see what changed in the Inverted Duty Structure after GST.

What is Inverted Duty Structure in the Post-GST World

Where the credit has been collected by virtue of pace of duty on inputs being higher than the pace of assessment on yield supplies, other than nil appraised or completely excluded supplies, with the exception of provisions of labor and products or both as might be informed by the Government on the proposals of the Council.

Refund system in Inverted Duty Structure

A registered individual might guarantee a discount of Input Tax Credit (ITC). The ITC because of transformed duty construction can be guaranteed toward the finish of any expense period where the credit has been collected by virtue of the pace of assessment on inputs being higher than the pace of expense on yield supplies.

As per Section 54(3) of CGST Act, 2017, refund of accumulated ITC will be granted where the credit accumulation has taken place on account of inverted duty structure. However, the Government also has the power to notify supplies where refund of ITC will not be admissible even if such credit accumulation is on account of an inverted duty structure.

In exercise of the powers conferred by this section, the government has issued Notification no. 15/2017-Central Tax (Rate) dated 28.06.2017 wherein it has been notified that refund of unutilised input tax credit shall not be allowed under sub- section (3) of section 54 of the said CGST Act, 2017, in case of supply of services specified in sub-item (b) of item 5 of Schedule II of the CGST Act, 2017.

The supplies specified under item 5(b) of Schedule II are construction services. In respect of goods, the central government has issued Notification no. 5/2017- Central Tax (Rate) dated 28.06.2017 as amended by Notification no. 44/2017-Central Tax (Rate) dated 14.11.2017. The government has notified the following goods in respect of which unutilized ITC will not be admissible as refund: –

It has been clarified by the Government vide Circular no. 18/18/2017- GST dated 16.11.2017, that the aforesaid notification having been issued under clause (ii) of the proviso to sub-section (3) of Section 54 of the CGST Act, 2017, restriction on refund of unutilised input tax credit of GST paid on inputs will not be applicable to zero rated supplies, that is (a) export of goods or services or both; or (b) supply of goods or services or both to a Special Economic Zone Developer of special Economic Zone Unit.

Accordingly, as regards export of fabrics, it has been clarified that subject to provisions of Section 54(10) of the CGST Act, 2017, a manufacturer of such fabrics will be eligible for refund of unutilised input tax credit of GST paid on inputs (other than input tax credit of GST paid on capital goods) in respect of fabrics manufactured and exported by him.

Further, Rule 89(2) (h) of CGST Rules, 2017 stipulate that refund claim on account of accumulated ITC (where such accumulation is on account of inverted duty structure) has to be accompanied by a statement containing the number and date of invoices received and issued during a tax period.

Rule 89(3) of CGST Rules, 2017 also provide that where the application relates to refund of input tax credit, the electronic credit ledger shall be debited by the applicant in an amount equal to the refund so claimed.

In Inverted Duty Structure, there are also terms on which you cannot claim refund on the Inverted Duty Structure. Let’s understand what these terms are.

Terms where the refund of the unutilised input tax credit cannot be claimed:

- If the supplier avails duty drawback or refund of IGST on such supplies.

- If the goods exported out of India are subject to export duty.

- Output supplies are nil rated or fully exempt supplies except for supplies of goods or services or both as may be notified by the Government on the recommendations of the GST Council.

- If supplier claims refund of output tax paid under IGST Act.

How to Calculate Maximum Refund Amount?

To calculate the maximum refund amount there is a simple formula. The formula creates a distinction between suppliers having a higher component of input goods than those having a higher component of input services, and must be read down accordingly, must be rejected.

Formula of maximum refund amount

Maximum Refund Amount= (Turnover of inverted rated supply of goods and services X Net input tax credit /Adjusted total turnover)– Tax payable on such inverted rated supply of goods and services

Terms in Computation of Maximum Refund Amount You Must Know About

Here is a list of terms that you must acquaint yourself with for the computation of maximum refund amount.

- Turnover of inverted rated supply of goods

- Net input tax credit

- Adjusted Total Turnover

- Tax payable on such inverted rated supply of goods

- Relevant period

Turnover of Inverted Rated Supply of Goods

The worth of inverted supply of goods and services made during the pertinent period without payment of tax under a bond or letter of undertaking.

Net Input Tax Credit

Net ITC will mean information tax reduction benefited on inputs during the significant period other than the information tax break profited for which discount is guaranteed under sub-rules (4A) or (4B) or both.

Adjusted Total Turnover

Adjusted Total turnover” means the turnover in a State or a Union territory, as defined under sub-section (112) of section 2, excluding the value of exempt supplies other than zero-rated supplies and the turnover of supplies in respect of which refund is claimed under sub-rules (4A) or (4B) or both, if any, during the relevant period.

Tax payable on such inverted rated supply of goods

The tax amount payable on such inverted rated supply of goods under the same head i.e. IGST, CGST, SGST.

Relevant Period

The period for which the claim has been filed.

Now that we have understood almost everything about the refund under Inverted Duty Structure under GST, let us understand how to claim refund for Inverted Duty Structure.

Claiming Refund of ITC Under Inverted Duty Structure

Points to remember while claiming for refund for Inverted Duty Structure:

- GSTR-1 and GSTR-3B have to be filed for the relevant tax period for which you want to file a refund application of the accumulated ITC.

- RFD-01 is the application through an online facility enabled for claims of refund.

- RFD-01 has to be filed within two years from the end of the financial year in which such claim for refund arises.

Steps to Claim Refund Under Inverted Duty Structure:

Step 1: Fill and file RFD-01 on GST Portal. ARN will be generated by the GST Portal.

Step 2: Print the filled application and the Refund application ARN Receipt generated available on the portal.

Step 3: Submit the printed documents with relevant supporting documentation to the jurisdictional authority.

Step 4: A tax official will process the refund application. Once the application is processed, a refund will be disbursed manually.

Step 5: Contact the Nodal officer of the corresponding state/centre in the case where the jurisdictional authority of the state/centre is not yet allotted.

Once you have applied/claimed for refund under the inverted duty structure, you also need to track your application right? Here is how you can do it.

How to Track Refund Application?

You have the following provisions to track your refund claim application:

- Download PDFs of the Filed applications (ARNs) using the My Saved / Submitted Applications option under Refunds.

- Track the status of the Filed applications using the Track Application Status option under Refunds.

We hope this article helped you gain some understanding over the Inverted Duty Structure under GST.

Deskera: One Stop Solution For GST

GST often may seem like a complicated process that you don’t want to get your hands dirty into. However, if you fulfill the criteria of the GST registrations, you don’t have any option but to get your GST registrations which can be a headache. What if you had a software like Deskera Books that can help with a time-saving strategy for managing your work contacts, invoicing, bills and expenses. You can also import opening balances and set up chart accounts through it.

Deskera Books is software that enables you to generate e-Invoices for Compliance with the Indian jurisdiction. It lets you easily create e-invoices by clicking on the Generate e-Invoice button.

Here is a tutorial to guide you through Deskera

Now that you have Deskera, you can easily manage your journals. A single interface gives you access to all remarkable features, including the ability to add products, services, and inventory.

You can automatically generate and send invoices using this accounting software. Further, creating financial statements has become considerably easier thanks to the software, which lets you draft balance sheets, income statements, profit and loss statements, and cash flow statements.

GST and the process related to this can turn out to be troublesome for most people. This is where Deskera can help you. With Deskera blogs, you can understand the topics such as GSTR1, GSTR2A, GSTR 2B, GSTR3B, etc. in a better manner.

You can even manage your business contacts, invoicing, bills, and expenses with Deskera Books. Not only this, you can even import opening balances and create chart accounts through it.

Key Takeaways

- An inverted duty structure comes up in a situation where import duties on input goods are higher than on finished goods.

- As per Section 54(3) of CGST Act, 2017, refund of accumulated ITC will be granted where the credit accumulation has taken place on account of inverted duty structure

- If the goods exported out of India are subject to export duty you cannot claim a refund.

- To calculate the maximum refund amount there is a simple formula. The formula creates a distinction between suppliers having a higher component of input goods than those having a higher component of input services,

- The worth of inverted supply of goods and services made during the pertinent period without payment of tax under a bond or letter of undertaking.

- The tax amount payable on such inverted rated supply of goods under the same head i.e. IGST, CGST, SGST.

- Relevant period is the period for which the claim has been filed.

- GSTR-1 and GSTR-3B have to be filed for the relevant tax period for which you want to file a refund application of the accumulated ITC.

Related Articles