That new car that you have recently purchased to take care of your conveyance while you shuffle between your offices certainly makes your life easier. Yet, IRS Form 4562 is something that is eyeing your new vehicle closely; and also keeping a watch if you have filed it.

IRS Form 4562 is used to represent the Depreciation and Amortization of an asset that you have purchased for facilitating your business operations. The form can be helpful to you in reducing the tax load once you understand the minutes of the form.

This article aims to present the details surrounding the form along with the following terms:

- What Is the IRS Form 4562?

- What are Depreciation and Amortization?

- What is Bonus Depreciation?

- Who Should file Form 4562?

- When Should You file Form 4562?

- What Should You fill out in Form 4562?

- How to fill out Form 4562?

What Is the IRS Form 4562?

IRS Form 4562 is known as the Depreciation and Amortization form which you need to complete while filing your income tax return. There are assets such as land, vehicles, machinery, equipment, and so on, that are purchased by a company for business use. All assets depreciate and their value must be calculated for an accurate accounting process. Therefore, Form 4562 is filed to take into account the depreciation and amortization of these assets used for business purposes.

Companies can also claim Bonus Depreciation using Form 4562.

What are Depreciation and Amortization?

Depreciation refers to the process of writing off the value of a fixed asset or tangible asset over multiple tax years. Whenever an asset is purchased, it may have a huge value that may not be written off in a single year; and therefore, you need to distribute it over a span of a few years.

A tangible asset is one that can be touched and has a physical form. An intangible asset, on the other hand, does not have a physical appearance, nor can it be touched. Examples of intangible assets are patents, copyrights, goodwill, trademarks, and so on.

While tangible assets are depreciated, intangible assets are amortized. Amortization and depreciation are concepts that are quite similar to each other with the difference being in the type of assets that each one addresses.

If you find the concepts too much to bear, taking assistance from a certified and qualified CPA would work well.

What is Bonus Depreciation?

Bonus depreciation is a method of accelerated depreciation and is optional.

Since the Tax Cuts and Jobs Act of 2018, businesses can now deduct 100% of the cost of qualified property from their taxable income in the year it was purchased. This approach is taken instead of amortizing the asset cost over a period of time. From $500,000 to $1,000,000, there has been an increment in the annual limits for these types of deductions.

If a company takes advantage of bonus depreciation, its total expenses will increase in the year the purchase was made and thus shrink its profit. This would result in a lowered total taxable income, thereby reducing its tax obligations.

Who Should file Form 4562?

In case you are carrying out a deduction of a depreciable asset on your tax return, then you must file Form 4562.

As discussed in the previous section, all your tangible or fixed assets need to be depreciated. However, inventory is separate from your fixed assets, and is, therefore, not counted in while depreciation is being carried out. As a result, you are obligated to file Form 4562 every year you depreciate your assets.

When should You file Form 4562?

The form is to be included when you are filing your income tax returns. Importantly, you are required to file it for the year you purchased the asset or the property.

What Should You fill out in Form 4562?

Before you begin filling out the details, you need to gather up all your relevant documents and the information that you need to provide with the form. Once you have done that, jot down these significant data to fill out the details in the form:

- The newly acquired asset’s cost

- The asset’s receipt

- The date when you started using the asset for the business purposes

- The final and total income that is being reported for the year

Apart from these, if you are using the asset for personal use also, you will need to provide:

- A percentage breakdown of how frequently is the asset used for personal and business reasons

- Any other details or document pertaining to the asset

How to fill out Form 4562?

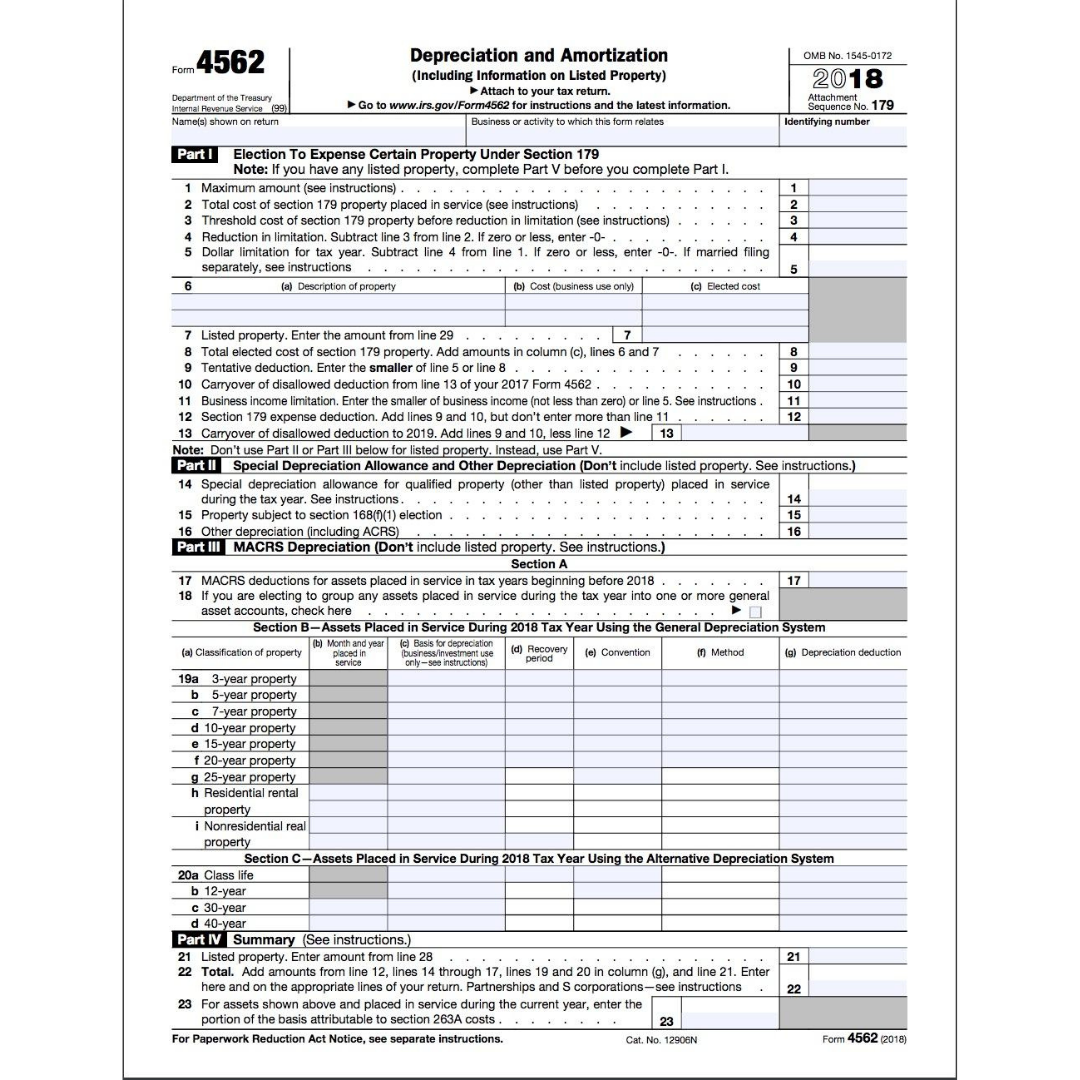

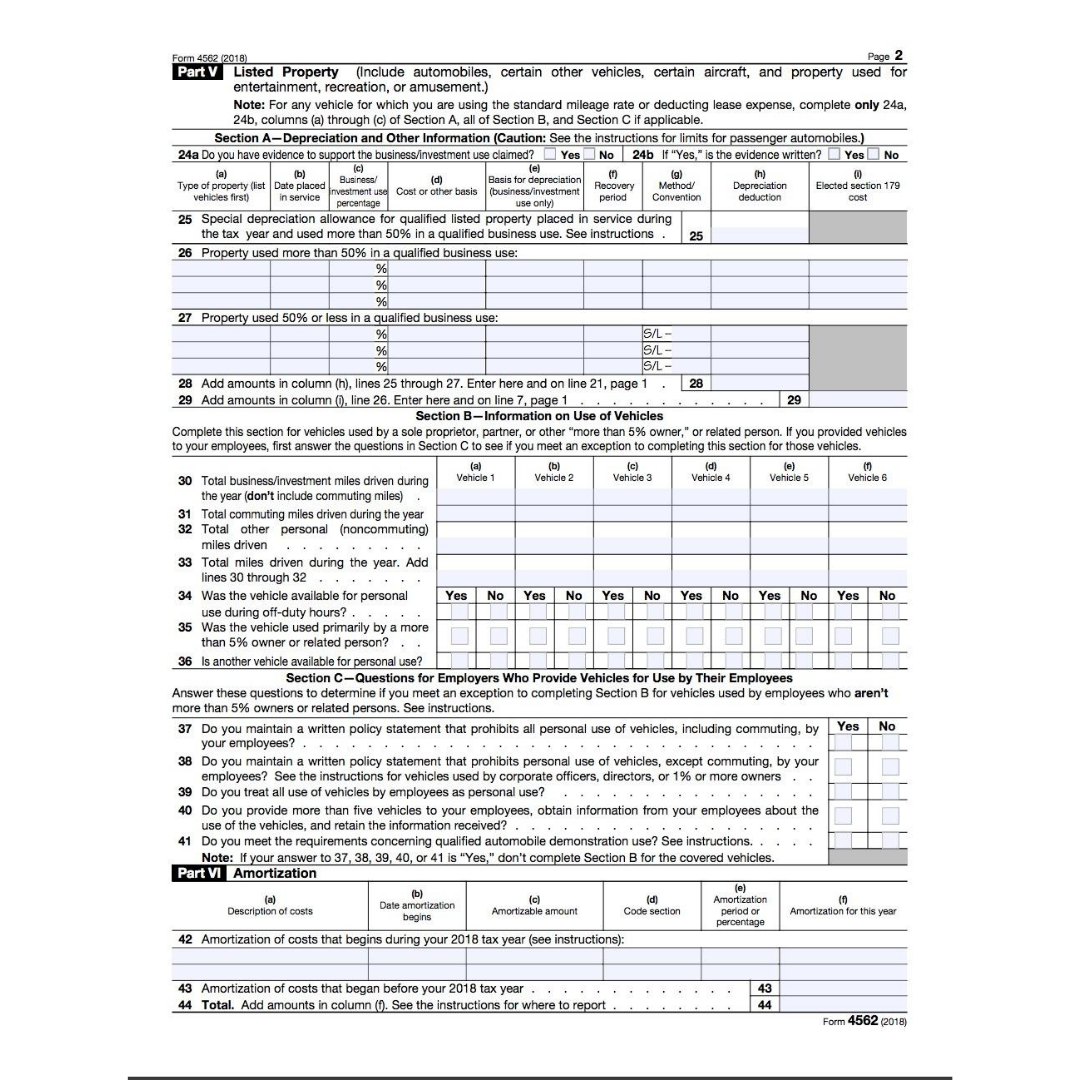

This section elaborately explains the text in the form 4562 as it would make it easier for you to know the sections that are mandatory and the ones you can skip. Here is how the form appears like:

The form consists of 6 parts as depicted from the images above.

Part I: Section 179 Deductions

The section 179 enables you to depreciate the maximum amount of the total amount/price of the asset in its first year. As a matter of fact, you can depreciate the entire asset, and if you are not able to do so, then you may distribute the amount over to the next few years.

When you are determining the asset for Section 179, ensure that the asset is already in use for that year.

Here is a Line-wise break-up of the fields that need to be filled in:

Part II: Special Depreciation Allowance

Special depreciation allowances are only applicable to certain qualified properties. This is important if your business uses "green" technology. Learn more to ascertain your qualification.

Calculating qualified properties can be quite complex and to eliminate complications, it would be wise to seek services and opinions from a CPA.

Part III: MACRS Depreciation

The purpose of this section is for those who plan to depreciate property over several years rather than utilizing Section 179 to write off as much as possible, and then paying later for the remaining part.

The IRS provides Modified Accelerated Cost Recovery System (MACRS) guidance on the period for which you depreciate property. There are different types of properties that depreciate over various years. Some can be depreciated in as less as 3 years and some can be depreciated over a period of two decades.

Part IV: Form Summary

This is a summary of the form 4562 and its contents. You may skip this for now and come back later.

Part V: Listed Property

You can use listed property both for business and for personal purposes. It could be a car that you use for your commute to office or for dropping kids to their school.

Part VI: Amortization

This part includes the details of any assets that are being amortized.

How can Deskera Help You?

No matter the expanse of your business, large or start-up, Deskera Books aims to provide accounting solutions for all. Apart from enabling easy handling of online accounting and invoicing applications, the tool also allows you to access all your financial documents in one place, including invoices, expenses, and all your contacts.

The user-friendly enterprise features of the software will be exceptionally helpful if yours is a start-up. The simplified layout and clear depiction let you surf through the software easily. All your journal entries, debit notes, credit notes, payments, or estimates are just a few clicks away.

Deskera also has templates that are designed to work remarkably well for your business. The effortless application of these templates allows you to create quotes, purchase orders, back orders, bills, and payment receipts.

If you own a drop shipping business, you can now expect to relax a bit as the platform makes it convenient for you to create drop ship orders based on customer orders. Take this video tour to learn more about Deskera’s services in accounting and sales.

Additionally, you can also take a look at Deskera People, a software that aims to expedite your regular tasks. You can now take care of your core business tasks and let the tool handle other actions like hiring, payroll, leaves, attendance for you.

Key Takeaways

Here are the important points from the article:

- All assets depreciate and their value must be calculated for an accurate accounting process. Therefore, Form 4562 is filed to take into account the depreciation and amortization of these assets used for business purposes

- IRS Form 4562 is used to represent the Depreciation and Amortization of an asset that you have purchased for facilitating your business operations

- Companies can also claim Bonus Depreciation using Form 4562, although its optional

- Depreciation refers to the process of writing off the value of a fixed asset or tangible asset over multiple tax years

- Amortization and depreciation are concepts that are quite similar to each other with the difference being in the type of assets that each one addresses

- If a company takes advantage of bonus depreciation, its total expenses will increase in the year the purchase was made and thus shrink its profit, ultimately reduces its tax obligations

- Companies carrying out a deduction of a depreciable asset on their tax return must file Form 4562.

- Assets cost, its receipt, date when it was put to use, and final income for the year are the primary information required to go in to the Form 4562

Related Articles