Amortization could apply in two situations: while taking a loan or in a business where intangible assets are concerned. If you happen to fall in either of the categories, then this article is for you.

From this article, we shall be learning about:

- Understanding amortization

- Calculating amortization

- Formula and examples of amortization

- Types of Amortization

- Amortization Rate and Expense

What is Amortization in Simple Terms?

Amortization applies to two situations: intangible assets and paying off a loan

Let’s consider the first situation. The intangible assets have a finite useful life which is measured by obsolescence, expiry of contracts, or other factors. A company needs to assign value to these intangible assets that have a limited useful life. This process is called amortization.

Like the wear and tear in the physical or tangible assets, the intangible assets also wear down. Owing to this, the tangible assets are depreciated over time and the intangible ones are amortized.

In simple terms, amortization in accounting decreases the value of an intangible asset gradually and presents an expense in the revenue/ income statement to recognize the change on the balance sheet for the given period.

The second situation, amortization may refer to the debt by regular main and interest payments over time. A write-off schedule is employed to reduce an existing loan balance through installment payments, for example, a mortgage or a car loan.

What Does Amortized Mean?

In general, to amortize is to write off the initial cost of a component or asset over a certain span of time. It also implies paying off or reducing the initial price through regular payments.

Financially, amortization can be termed as a tax deduction for the progressive consumption of an asset's value, in particular an intangible asset. It is often used with depreciation synonymously, which theoretically refers to the same for physical assets.

At times, amortization is also defined as a process of repayment of a loan on a regular schedule over a certain period.

How Do I Calculate Amortization?

To access information on calculating amortization, we need to consider both the scenarios -

- When you know the loan amount

- When you do not know the loan amount

For scenario A:

Calculation of amortization is a lot easier when you know what the monthly loan amount is. So, here’s a step-by-step guide to calculating amortization.

- In the first month, multiply the total amount of the loan by the interest rate.

- In the case of monthly installments, divide the result of step 1 by 12 to get the monthly interest amount.

- Next is to subtract the interest from the monthly installment amount; the remaining amount goes as the principal.

- For the second month, repeat the process; but start with the remaining principal amount from the first month’s calculation. Remember not to start with the original amount of the loan.

- Continuing with this calculation, your principal will be zero by the end of the loan term.

For Scenario B

In the case, where you do not know your monthly amount for repayment. Let’s see the steps you’ll take then:

- From your loan amount and the rate of interest, you can easily get the monthly amount to pay.

- After this, the steps would be the same to calculate the amortization schedule.

- You may either lay your hands on a calculator to do this or you may also do it from scratch, all by yourself.

Business Perspective

In the course of a business, you may need to calculate amortization on intangible assets. In that case, you may use a formula similar to that of straight-line depreciation. These assets can contribute to the revenue growth of your business. You may expense them against the future revenues. An example of an intangible asset is when you buy a copyright for an artwork or a patent for an invention.

Calculating Amortization for a Patent:

Assume that you purchase a patent for $115,000 with a useful life of 10 years. From the formula:

Original Price / Useful Life = Amortization per Year

We get,

$15,000 / 10 = $1500 per year.

Why is it Good to Know Your Amortization Schedule?

In a loan amortization schedule, this information can be helpful in numerous ways. It's always good to know how much interest you pay over the lifetime of the loan. This helps you decide if you want to make main payments sooner. Your additional payments will reduce outstanding capital and will also reduce the future interest amount. Therefore, only a small additional slice of the amount paid can have such an enormous difference.

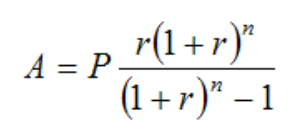

What is the Formula for Amortization?

Before taking out a loan, you certainly want to know if the monthly payments will comfortably fit in the budget. Therefore, calculating the payment amount per period is of utmost importance.

Here it goes:

Here,

A = payment amount

P = initial loan amount or Principal

r = rate of interest

n = total number of payments

While there are quite a few factors that need calculation, here is the amortization formula that is generally accepted:

What is an Example of Amortization?

Consider the following examples to better understand the calculation of amortization through the formula shown in the previous section.

Amortization calculation for a Vehicle/ Car

You want to calculate the monthly payment on a 5-year car loan of $20,000, which has an interest rate of 7.5 %. Assuming that the initial price was $21,000 and a down payment of $1000 has already been made.

So here,

P = $20,000

r = 7.5 % per year / 12 months

= 0.00625

n = 5 years * 12 months

= 60 total periods

By using the formula, A or Payment Amount, is $400.76 per month.

In this way, you can estimate the amortization period and the monthly payment amount.

Amortization Calculation for an Intangible Asset

For this case, we assume a company that develops a particular software for its internal use. As they do not intend to sell it, the software will be an intangible asset.

So, to calculate the amortization of this intangible asset, the company records the initial cost for creating the software. This cost is recorded in the balance sheet.

Cost of Software = $10,000

Useful life of software = 3 years

Due to uncertain and continuous technological advancements, the software does not have a remaining value. So, its salvage value is zero.

(Initial cost - Salvage value) / useful years

(10,000 - 0) / 3 = $3,333

Consequently, the company reports an amortization for the software with $3,333 as an amortization expense.

What Does a 20 Year Amortization Mean?

The purchase of a house, or property, is one of the largest financial investments for many people and businesses. The heavy asking price usually requires a mortgage in most cases. This mortgage is a kind of amortized amount in which the debt is reimbursed regularly. The amortization period refers to the duration of a mortgage payment by the borrower in years.

Buyers may have other options, including 25-year and 15-years mortgages, the most preferred being the mortgage for 30 years. The amortization period not only affects the length of the loan repayment but also the amount of interest paid for the mortgage. In general, longer depreciation periods include smaller monthly payments and higher total interest costs over the life of the loan.

With the lower interest rates, people often opt for the 5-year fixed term. Although longer terms may guarantee a lower rate of interest if it’s a fixed-rate mortgage.

Even if you can afford to buy a shorter amortization, buying a longer one can be beneficial for cash flow. Let's say you have an amortization period of 25 years at 2 percent of $500,000 mortgaging. The monthly payment amount comes to $2,117.26. But it would be $2,527.46 if you had it for 20 years. Generates a difference of $410.20 a month.

Let’s say, it's the 25-year loan you can take, but you should fix your 20-year loan payments (assuming your mortgage allows you to make prepayments). You could just change your monthly payments without a penalty for 25 years if you are ever faced with financial difficulties.

This way, taking a 20-year amortization could prove to be beneficial as compared to a 25-year amortization in this situation.

What is Amortization Period?

The amortization period is defined as the total time taken by you to repay the loan in full. Mortgage lenders charge interest over the loan or the mortgage amounts and therefore, it implies that the longer the loan period more is the interest paid on it. With an amicably agreed interest rate, the amortization period can also provide the amount that will be paid as the monthly installment.

The amortization period is based on regular payments, at a certain rate of interest, as long as it would take to pay off a mortgage in full. A longer amortization period means you are paying more interest than you would in case of a shorter amortization period with the same loan.

Let’s see this example for a firmer understanding:

Mr. Andrews has a $200,000 mortgage with a 5% interest rate and a monthly payment of $1067.38. The mortgage would be paid off in 360 months, or 30 years, assuming $1067.38 was paid every month for the term of the loan.

So, the amortization time here is 360 months.

What are the Two Types of Amortization?

To learn about the types of amortization, we shall consider the two cases where amortization is very commonly applied.

Case 1: Real Estate:

Here we shall look at the types of amortization from the homebuyer’s perspective. If you are an individual looking for various amortization techniques to help you on your way to repay the loan, these points shall help you.

Full Amortization: In this type, you pay the full amortization amount which eventually makes the outstanding balance zero at the end of the term.

Partial Amortization: When you make a partial payment of your amortization amount, your monthly amount gradually reduces. However, you will be left with an outstanding balance when your loan term ends.

Interest Only: In this type, you pay only the interest without including any payments of amortization. In this case, you will have the principal intact (the same amount as when the term started) at the end of the term.

Negative Amortization: This requires you to pay monthly amounts that are even lower than the interest rate. It means you pay less than what you paid in the ‘ interest only’ type of amortization. However, the deficit amount gets added to the overall loan amount each month. So, you may end up with a larger amount than the principal at the end.

For clarity, assume that you have a loan of $300,000 with a 30-year term.

- With full amortization type payments, your loan will be completely paid off at the end of the term which is 30 years.

- With partial type, you would have some outstanding balance which would be a bit less than the principal, $300,000.

- Under the Interest Only type, you would be paying some amount monthly but at the end of the term, you will still be left with the original amount of $300,000.

- With the negative amortization, you will owe the lender an amount much greater than $300,000.

Let’s move on to the next case where amortization is an integral part.

Case 2: Corporate or Business

Within the framework of an organization, there could be intangible assets such as goodwill and brand names that could affect the acquisition procedure. As the intangible assets are amortized, we shall look at the methods that could be adopted to amortize these assets.

Straight-line: This is also known as linear amortization. It implies distributing the entire interest amount equally throughout the loan. The simplicity of this method makes it a preferable method concerning accounting.

Annuity: In this method, the loan is amortized with equal amounts being paid at equal intervals.

There are two types of annuity:

- Ordinary annuity: Here, the payment is made at the end of the interval.

- Annuity Due: In this case, the payments are made at the start of each interval.

The different annuity methods result in different amortization schedules.

Declining Balance: This method expedites the process of amortization. In this, the regular interest payment reduces but the principal repayment rises. Each payment made is more than the interest, the balance amount of the loan slowly declines. This decline results in a lower interest amount and therefore, the principal repayment is expedited.

Bullet: In this type, there are periodic payments that only include the interest amount. This results in a large amount to be paid at the end which leads to complete repayment of the principal.

Negative Amortization: This is similar to the type we saw in case 1. As previously seen, the balance amount increases over time and is repaid at maturity.

With this, we move on to the next section which clears out if amortization can be considered as an asset on the balance sheet.

Is Amortization an Asset?

Amortization is a technique to calculate the progressive utilization of intangible assets in a company. Entries of amortization are made as a debit to amortization expense, whereas it is mentioned as a credit to the accumulated amortization account.

To know whether amortization is an asset or not, let’s see what is accumulated amortization.

What is accumulated amortization?

A cumulative amount of all the amortization expenses made for an intangible asset is called accumulated amortization. It gets placed in the balance sheet as a contra asset under the list of the unamortized intangible. When these intangible assets get consumed completely or are eliminated, then their accumulated amortization amount is also deleted from the balance sheet.

In other words, amortization is recorded as a contra asset account and not an asset.

What is an Amortization Rate?

The amortization rate can be calculated from the amortization schedule. The percentage of each interest payment decreases slightly with each payment in the amortization schedule; however, in the process the percentage of the amount going towards principal increases.

What are Amortization Expenses?

The cost of long-term fixed assets such as computers and cars, over the lifetime of the use is reflected as amortization expenses. When the income statements showcase the amortization expense, the value of the intangible asset is reduced by the same amount. This continues till the asset is sold or substituted.

Coincides an example where a firm purchases a computer for $2000. The amortization may be calculated in one of the methods below:

Straight-line method: The cost of the computer is divided by the number of years it is expected to be useful. Say 4. So, the firm subtracts $500 every year for 4 years from its taxable income.

Declining Balance method: This method applies to assets that lose a major chunk of their value in the earlier stages. The amortization amount, therefore, goes on decreasing every year with the decreasing value of the computer or car.

Accounting Impact of Amortization

To understand the accounting impact of amortization, let us take a look at the journal entry posted with the help of an example.

Let's say that XYZ LTD spends $50,000 to acquire a license that will expire and be be sold in five years.

Since a license is an intangible asset, it needs to be amortized over the five years prior to its sell-off date.

Annual amortization in this case will be:

Amortization = $50,000/ 5 years = $10,000/year

The accountant, or the CPA, can pass this as an annual journal entry in the books, with debit and credit to the defined chart of accounts.

The bookkeeping double entry would be:

Debit Amortization Expense - $10,000

Credit Accumulated Amortization - $10,000

The expense would go on the income statement and the accumulated amortization will show up on the balance sheet.

Luckily, you do not need to remember this as online accounting softwares can help you with posting the correct entries with minimum fuss. You can even automate the posting based on actual amortization schedules.

Key Takeaways

This post helped us understand the key components associated with Amortization. Let’s conclude the post with these key points:

- Fundamentally, amortization is all about writing off the value of either an intangible asset or a loan.

- Amortization schedules are important for the borrower as well as the lender to draw a chart of the repayment intervals based on the end date of the term.

- Amortization helps businesses to record expensed amounts for an intangible asset like software, a patent, or copyright.

- The amortization period is the end-to-end period for paying off a loan.

- Amortization is a contra asset.

- Amortization expense denotes the cost of the long-term assets which gradually decline over time.