Index

- What is a sole trader?

- Advantages and disadvantages of a sole trader business

- Setting up sole trader accounts

What is a sole trader?

{kind=link}

A sole trader is the most simple and minimalistic form of business structure which is relatively inexpensive and easy to set up. If a single proprietor engages in any business activity without a formal organization and keeps the profits for themselves, they are known as a sole trader or sole proprietor. A sole trader is legally responsible for all aspects of their business. A sole trader will generally make all the decisions about starting and running their business and have the liberty to employ people as per their needs. A sole trader can also use a business name other than their legal name. However, they may have to legally trademark their business name if it differs from their legal name. This process may vary depending upon their country of residence.

Being a sole trader comes with its perks and risks. A sole trader bears complete responsibility for the finances and accounting of their business and so it can get very difficult. Very soon, this can even curb the growth of their company. Therefore, most sole trader businesses eventually get bought out by limited companies. These limited companies usually overtake sole trader businesses if they see profitability or if they feel that the sole trader’s company can be a direct competitor to their business.

Advantages and Disadvantages of a sole trader business:

Now that we have a basic idea of who a sole trader is, it’s now time to look at the various pros and cons that are associated with running a sole trader business.

{kind=link}

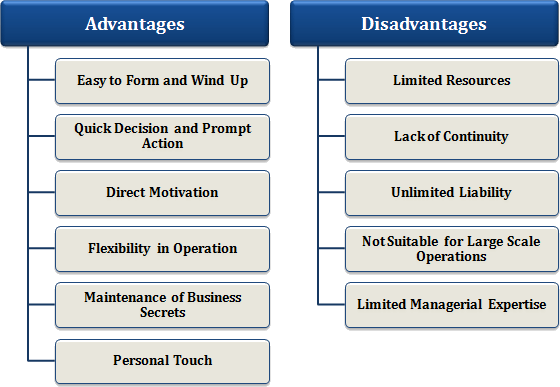

Pros of being a sole trader business:

A sole trader business gives the proprietor advantages like ease of setting up or shutting down a business at any time. As the sole trader will be the only decision-maker, executing plans will be quick and hassle-free. Business operations for a sole trader are completely private, so their competitors will not be able to learn how much they earn. Their business will also have a personal touch and will not be shadowed by the burden of being a corporate entity. In addition to that, the paperwork and accounting for a sole trader business is fairly simple, so they can easily start their business in a matter of days.

Cons of being a sole trader business:

One of the biggest disadvantages of being a sole trader is the personal liability. With limited finances, the need to borrow money for the business often arises, for which a bank may require personal property as collateral. Sometimes banks are reluctant to lend to sole traders or charge them a higher interest rate because of a general lack of business longevity in sole trader businesses, which can be mainly due to owners becoming incapacitated due to age, health, or death. A limited leadership experience may also create hurdles while trying to ensure that business operations run smoothly.

Setting up sole trader accounts.

If you decide to be self-employed and begin a sole trader business, you will need to set up your sole trader account to record your expenses and income.

To do this, you will need to be aware of tax regulations, basic accounting, and bookkeeping.

Here’s a quick guide on setting up sole trader accounts.

1. Open a separate bank account.

Legally, a sole trader is not separate from his business, so a separate business bank account may not be required to run a sole trader business.

However, it is always advisable to keep your business and personal finances separate: because:

- If you only have a personal bank account you will have to be careful while specifying personal and business-related expenses.

- Recording expenses and income takes more time when you have to classify each expense.

- Having a separate business bank account, allows you to easily record business expenses and income. Thus, completing your annual accounts and assessing your taxation becomes less time-consuming.

2. Keep a tab on the taxation regulations.

As a sole trader, you will be required to set aside money for your taxations each year, which will have been self-assessed. It, therefore, becomes necessary to be aware of income tax thresholds and the National Insurance Contributions (NICs) you will be required to pay.

Failure to monitor your taxes as a sole trader can severely impact your business. With each country having a separate set of laws to deal with tax defaulters, your inability to pay taxes on time, can lead to fines and in some cases even a prison sentence. Read why auditing is important for all businesses including that of a sole trader.

3. Bookkeeping.

Bookkeeping for a sole trader is fairly simple and minimal when compared to a limited company. Your primary goal as a sole trader will be to track monthly income and expenditure. For doing so, you must keep records of all your invoices and receipts.

{kind=link}

It’s also advisable to keep receipts of any work-related transactions. If you own an office, or if you work from home, you may be able to claim rent and bills back from your national tax body as a business expense. You can check out our blog to learn the basics of bookkeeping.

Alternatively, you can also use bookkeeping software or an online accounting facility to record your business expenses and income.

These bookkeeping software packages can help you save valuable time by cutting out duplication and are hence becoming more and more popular with sole trader businesses. To know more or to find the best bookkeeping software for your needs, check out Deskera's bookkeeping section.

{kind=link}

As a sole trader, you’re responsible for managing your company accounts – it’s therefore important to have the right tools for keeping on top of your finances.

Deskera provides an intuitive and easy to use software, which not only helps sole traders in their responsibilities of accounting but also in CRM, invoicing, payroll, financial reports & more.

Want to know more about the various nuances of the business world? Stay updated with the latest business developments through Deskera’s insightful blogs.