Covid in 2020 changed the face of the industry. There employees being laid off, companies were getting shut, companies were going online which meant laying off ground level workers and economy overall was hit. To help the people, the Government came up with PPP loan.

There was a first draw of PPP loan which was for the first year of the Covid wave, then by second year of Covid there was a second draw of PPP loan to help the people. In this article we will discuss a little about second draw PPP loan and the form 2483- SD that is to be filled for the second draw PPP loan.

This article covers the following:

- What is a Second Draw PPP Loan?

- How should you use Second Draw PPP Loan?

- Documents required to fill Second Draw PPP Loan application.

- How to fill form 2483-SD?

- FAQs

- How can Deskera assist you?

What is a Second Draw PPP Loan?

In 2020, the federal government’s Paycheck Protection Program (PPP) provided forgivable loans to more than 5 million U.S. businesses to help them make it through the coronavirus crisis.

A forgivable loan is a type of loan that allows borrowers to have the balance of their loan either partially or forgiven if they meet certain conditions. In 2021, many of those same businesses also got the opportunity to apply for a forgivable second-draw PPP loan, which can provide more short-term assistance.

How Should You Use Second Draw PPP Loan?

Businesses must spend at least 60% on payroll costs to get a second-draw PPP loan forgiven. The other 40% can be spent on the following non-payroll expenses:

- Qualifying rent or mortgage interest payments.

- Utility costs.

- Operations expenses: cloud computing services, business software, human resources, and related expenses.

- Supplier costs: payments that go to suppliers who provide essential goods.

- Worker protection expenses: expenses to employees safer during COVID-19, including personal protective equipment (PPE), drive-thru windows, sneeze guards and outside dining enclosures.

- Property damage costs: costs related to civil unrest that occurred in 2020 that were not covered by insurance.

List of Documents Required to Fill Second Draw PPP Loan

- Copy of photo ID for all owners who own 20 percent of the business or more

- 2019 and 2020 profit and loss statements to show revenue loss during 2020

- 2019 business tax returns; 2020 returns if available

- For partnerships include IRS Form 1065 and Schedule K-1

- For sole proprietors include IRS Form 1040 Schedule C

- Articles of incorporation

- Payroll reports with a list of gross wages paid time off, and taxes assessed for all employees for all 12 months of 2020

- 2020 employer IRS documents (including one of the following for all four quarters of 2020):

- Form 941: Employer's Quarterly Federal Tax Return. Learn how to fill the form 941 here.

- Form 944: Employer's Annual Federal Tax Return (for smallest employers)

- Form 940: Employer's Annual Federal Unemployment (FUTA) Tax Return

- Form W-3: Transmittal of Wage and Tax Statements

- Documentation to support health insurance and retirement expenses incurred as a part of payroll expenses (for example, a statement from insurance or retirement company)

How to Fill Application form 2483-SD

Here is your stepwise guide to fill your form 2483 SD:

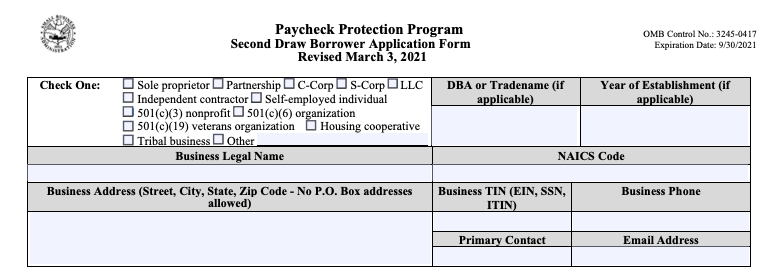

Step 1: Fill Your Basic Information

In this section, you have to start by selecting the business structure that best represents your business. Try to be as specific as possible. For example, choosing “Sole Proprietor” is going to be better than “Self-Employed Individual” as even though both could be correct, one conveys more information.

You are required to provide both your Business Legal Name and your DBA or Trade Name if applicable. Your Business Legal Name is found on any government form. A DBA or Trade Name is what appears on bank statements or invoices if it’s different from your Business Legal Name. Your Business Address is also found in these documents.

If you are not a self-employed individual or contractor, you will have to provide the year your business was established. This must be consistent with the documents you filed to make the business official.

You can find your NAICS code on a website like NAICS.com. NAICS codes are self-assigned, meaning you pick the code that best suits your business rather than having one assigned to you. Start by searching keywords of what you do or look up a similar business’s NAICS code.

Your EIN (Employer Identification Number), TIN (Taxpayer Identification Number), or Social Security Number (SSN) is found on previous tax returns. If you’re having trouble finding this info, follow the IRS’s steps to finding your EIN. Note that an SSN should only be provided if you do not have a business EIN or TIN.

Finally, provide the name, business phone, and email address of the primary contact for the application. This will be who all future communications are directed to.

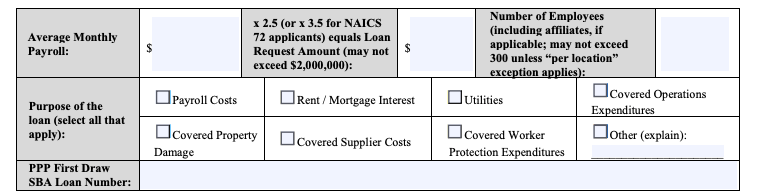

Step 2: Update Loan Amount Calculation

Your loan amount calculation starts with finding your average monthly payroll costs. Your average monthly payroll costs can be calculated using one of the following:

- the one year period before the loan application

- the calendar year of 2020

- the calendar year of 2019

Here is how you can do the calculation:

Step 1: Add up the payroll costs for all employees whose principal place of residence is in the United States. Payroll costs include:

- Salaries, wages, commissions, or tips

- Employee benefits including paid leave, allowance for separation or dismissal, and healthcare benefits including insurance premiums and retirement benefits

- State and local taxes

If you are including your net or gross income as reported on a Schedule C, use form 2483-SD-C.

Step 2: Subtract any compensation paid to an employee over $100,000. For example, if you have two employees earning $120,000 over the year, subtract $40,000 from your payroll total.

Step 3: Divide the total amount from Step 2 by 12 and put it in the Average Monthly Payroll box.

Once you have your average monthly payroll costs, finding your loan amount is as easy as multiplying it by 2.5 or 3.5.

Most businesses will use 2.5, the same calculation used in 2020.

But for businesses in the food and accommodation industry, you are eligible for 3.5 times your average monthly payroll costs. You are in the food and accommodation industry if your NAICS code (which you’ve provided already on this application) starts with 72.

Loan amounts are capped at $2 million. Put the lesser of your calculated loan amount and $2 million dollars in your loan request amount box.

Add up all employees across all locations and affiliates. There are three main cases where your business and another business would be considered affiliates:

- If your business controls or has the power to control another business

- If another business controls or has the power to control your business

- If a third party controls your business and another business

Check all boxes that apply. Businesses that do not run payroll but are still eligible for a PPP loan should check “Payroll Costs.” Self-employed individuals are eligible to take the PPP to cover their self-employment income. This is called owner compensation replacement or OCR and is still considered a payroll cost.

The purpose of PPP loans is to protect paychecks. If you do not select “Payroll Costs” in this section, your application may be denied.

The PPP loan you received in 2020 is considered your first draw PPP loan. You can find this number on the loan offer you received.

If you cannot find your loan offer, reach out to your previous lender. Most lenders will have this information available in an online portal you can access.

Step 3: Reduction in the Gross Receipts

A new eligibility requirement for second draw PPP loans is showing you experienced a 25% reduction in gross receipts.

For loan amounts of $150,000 or less, this section can be left blank. However, you will be asked to provide this information either when you apply for forgiveness or beforehand.

To calculate the reduction in gross receipts, you can use:

- Any quarter in 2020 and compare it with the same quarter in 2019

- Compare your annual 2020 and 2019 gross receipts

If you choose to use annual numbers, put “Annual” in the 2020 quarter and reference quarter boxes.

If your business opened in 2020 but was operational on February 15, 2020, you must use Q1 2020 as the reference quarter. The 25% reduction in revenue must be shown by comparing either Q2, Q3, or Q4 2020 with Q1 2020.

Step 4: Ownership

List all members of the ownership that hold 20% or more of the business. If you have more owners than spaces on the application, attach them as a separate sheet.

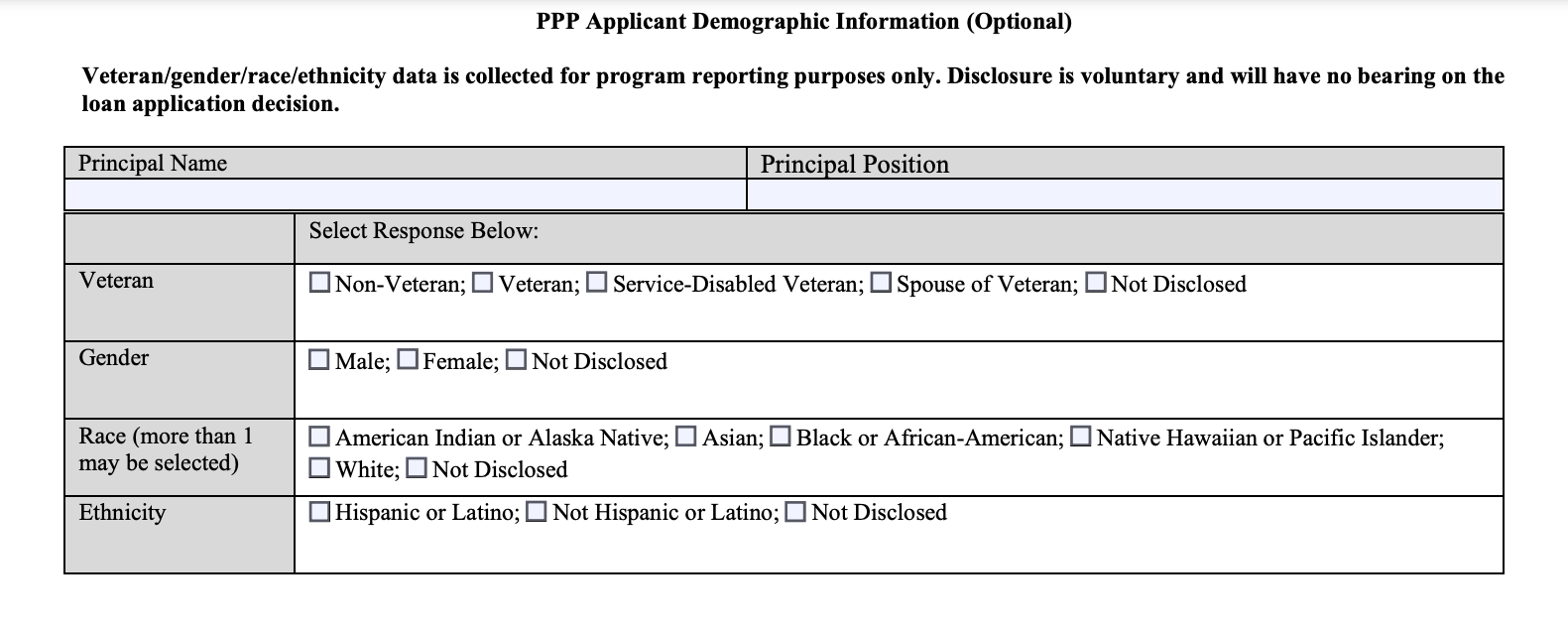

Step 5: Update Your Demographic Information

This section is completely voluntary and will be used for reporting purposes only. Any information you provide here will not impact your loan application.

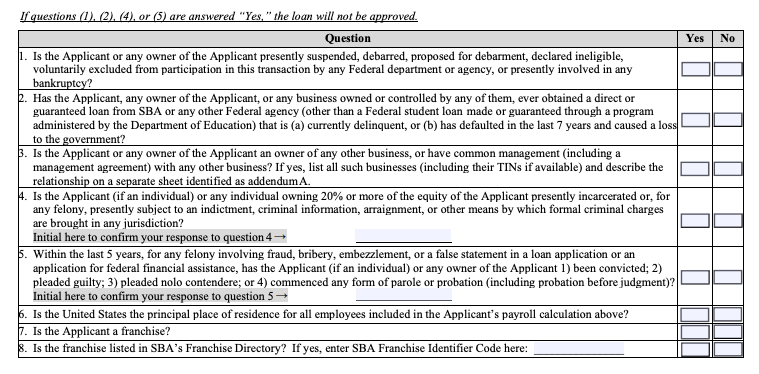

Step 6: Fill the Questionnaire

Answer each question and initial where indicated. Answering yes to questions 1, 2, 4, or 5 will mean you are ineligible for a PPP loan.

Step 7: Certification

On pages three and four of the application form, there are 15 statements. Each must be signed to certify that you are applying in good faith that these statements apply to your business. Be sure to read through each. Signing on any of these statements later found untrue can result in penalties through imprisonment or fines.

FAQs

If I received previous PPP funds, EIDL grants, unemployment benefits, or other government grants, are these funds to be included in my gross receipts when calculating my eligibility for a second PPP loan?

PPP funds and other state and federal government grants are not included in gross receipts.

How are the 2.5 months' worth of payroll expenses calculated?

Applicants will calculate the loan amount by taking the total payroll costs for 2019 or 2020, divided by 12, to identify the average monthly payroll for the calendar year. This value for the average monthly payroll is multiplied by 2.5 to calculate the loan amount. Industries assigned to NAICS code 72 (lodging and restaurants) may receive loans up to 3.5 months of average monthly payroll costs.

How should an applicant demonstrate they had a 25% reduction in gross receipts to be eligible for a second draw loan?

It is not required to provide documentation evidencing the applicant experienced a 25% reduction in gross receipts. This is a certification made by the applicant. The SBA may request documentation supporting this certification during a PPP loan audit.

How should independent contractors and sole proprietors calculate their loan amount? What documentation is required?

Independent contractors and sole proprietors may calculate their loan amount based on 2.5 months worth of income from 2019 or 2020, subject to a cap of an annualized salary of $100,000. The 2019 or 2020 Schedule C tax filing should be provided.

Do applicants have the choice of using either 2019 or 2020 payroll documentation to calculate their loan amount?

Yes, the loan amount may be based on either 2.5 months' worth of payroll from 2019 or 2020.

Most borrowers have applied for the forgiveness of their first PPP loan before applying for a second PPP loan?

You can receive a second draw loan after your first loan has been fully used, and you do not need to have the first loan forgiven before the second loan.

My business began operations in 2019. Our 2020 gross receipts are greater than 2019 due to being in operation in 2019 for only a few months, but still, need a PPP loan to support our operations. Do we qualify for a second PPP loan?

SBA guidance states that a business is eligible for a second draw PPP loan if the business experienced at least a 25% decrease in gross receipts for any quarter in 2020 relative to the same quarter in 2019.

What is included in gross receipts?

Per SBA guidance on second draw loans, gross receipts include all revenue in whatever form received or accrued (in accordance with the entity's accounting method) from whatever source, including from the sales of products and services, interest, dividends, rents, royalties, fees, or commissions, reduced by returns and allowances.

Would an applicant qualify for a second PPP loan if employees were laid off or furloughed in 2020?

Eligibility for a second draw loan is not based on relative FTE counts. However, to achieve full forgiveness of a second draw loan, at least 60% of the loan amount must be spent on eligible payroll expenses.

Is a business eligible for a second draw PPP loan if the business began in early 2020, prior to February 15, and cannot perform the 2019 gross receipts comparison?

SBA guidance states that a business is eligible for a second draw PPP loan if the business experienced at least a 25% decrease in gross receipts for any quarter in 2020 relative to the same quarter in 2019. If a business does not have 2019 gross receipts to compare to, they are ineligible for a second draw loan.

Is owner draw also included in eligible payroll costs when calculating the loan amount?

Owner draw is included in payroll when calculating the loan amount.

What time period do second draw PPP funds cover?

To achieve loan forgiveness, second draw funds must be spent on eligible payroll and non-payroll costs during the Covered Period. The Covered Period will begin for these loans on the date the Second Draw loan is disbursed into the borrower's account.

How do I calculate the 25% reduction in gross receipts?

The revenue reduction is calculated by taking 2020 gross receipts/2019 gross receipts. If the calculated value is 0.75 or less, the 25% reduction is met.

Is it correct that NAICS code 72 businesses are eligible for a loan amount of 3.5 months worth of payroll?

Yes, industries assigned to NAICS code 72 (lodging and restaurants) may receive loans up to 3.5 months of average monthly payroll costs for their second draw PPP loan.

Can the second draw loan amount be different than the first draw, or must the amounts be the same?

The amounts may differ if an applicant chooses to base the loan amount calculation on 2020 payroll costs versus 2019 payroll costs used to calculate the first loan amount.

What are “gross receipts” for the purpose of determining eligibility for a Second Draw PPP Loan?

For a for-profit business, gross receipts generally are all revenue in whatever form received or accrued (in accordance with the entity’s accounting method, i.e., accrual or cash) from whatever source, including from the sales of products or services, interest, dividends, rents, royalties, fees, or commissions, reduced by returns and allowances but excluding net capital gains and losses.

These terms carry the definitions used and reported on IRS tax return forms. Gross receipts do not include the following: • taxes collected for and remitted to a taxing authority if included in gross or total income, such as sales or other taxes collected from customers.

Amounts collected for another by a travel agent, real estate agent, advertising agent, conference management service provider, freight forwarder or customs broker.

Does my First Draw Loan need to be forgiven before I can receive a Second Draw Loan?

No. However, the funds from a First Draw Loan do need to be used up entirely on permissible expenses before the Second Draw Loan is disbursed.

Note that if the Applicant has a First Draw Loan that is currently under review by the SBA (including a loan of $2 million or more that triggered an automatic review), it will not receive a loan number or funds for a Second Draw Loan until the issue related to the First Draw Loan is resolved.

How much am I eligible to receive for a Second Draw Loan?

In general, eligible Applicants can receive up to two and a half months of the Applicant’s average monthly payroll costs (which are calculated in the same manner as for First Draw Loans), capped at a maximum of $2 million.

The new rule also provides maximum loan amount calculations for seasonal employers, Applicants who were not in operation during the one-year period prior to February 15, 2020, Applicants operating with a NAICS code beginning 72, farmers and ranchers, partnerships, and those who are self-employed. While the calculations vary slightly, these types of Applicants are all capped at maximum loans of $2 million.

Note that businesses that are part of a single corporate group will be capped at an aggregate amount of $4 million in Second Draw Loans.

The SBA’s instructions regarding loan calculations for different types of applicants.

Note, however, that since these instructions were published, the rules have been changed to allow sole proprietors, independent contractors, and self-employed individuals to use gross income rather than net income when calculating the eligible loan amount.

For all entity types (e.g., for-profit businesses and nonprofit organizations), do “gross receipts” include PPP Loan proceeds that are forgiven (or EIDL advances)?

No. The amount of any forgiven First Draw PPP Loan or any EIDL advance, which are not subject to federal income tax, is not included in the calculation of “gross receipts”.

What reference periods can be used to determine whether the Applicant can demonstrate at least a 25 percent gross receipts reduction in order to qualify for a Second Draw PPP loan?

The appropriate reference periods depend on how long the Applicant has been in business.

What documentation do I need to provide to corroborate that my entity sustained at least a 25 percent reduction in gross receipts?

The following are the primary sets of documentation Applicants can provide to substantiate their certification of a 25 percent gross receipts reduction (only one set is required).

Quarterly financial statements for the entity. If the financial statements are not audited, the Applicant must sign and date the first page of the financial statement and initial all other pages, attesting to their accuracy. If the financial statements do not specifically identify the line item(s) that constitute gross receipts, the Applicant must annotate which line item(s) constitute gross receipts.

Quarterly or monthly bank statements for the entity showing deposits from the relevant quarters. The Applicant must annotate, if it is not clear, which deposits listed on the bank statement constitute gross receipts (e.g., payments for purchases of goods and services) and which do not (e.g., capital infusions).

Annual IRS income tax filings of the entity (required if using an annual reference period). If the entity has not yet filed a tax return for 2020, the Applicant must fill out the return forms, compute the relevant gross receipts value (see Question 5), and sign and date the return, attesting that the values that enter into the gross receipts computation are the same values that will be filed on the entity’s tax return.

If I use my entity’s annual income tax returns to demonstrate a gross receipts reduction of at least 25 percent, what amounts do I use to calculate gross receipts?

The amounts required to compute gross receipts varies by the entity tax return type:4 • For self-employed individuals other than farmers and ranchers (IRS Form 1040 Schedule C): sum of line 4 and line 75.

For self-employed farmers and ranchers (IRS Form 1040 Schedule F): sum of lines 1b and 9. For partnerships (IRS Form 1065): sum of lines 2 and 8, minus line 66.

For S-Corporations (IRS Form 1120-S): sum of lines 2 and 6, minus line 47.

For C-Corporations (IRS Form 1120): sum of lines 2 and 11, minus the sum of lines 8 and 9.

For nonprofit organizations (IRS Form 990): the sum of lines 6b(i), 6b(ii), 7b(i), 7b(ii), 8b, 9b, 10b, and 12 (column (A)) of Part VIII.

For nonprofit organizations (IRS Form 990-EZ): sum of lines 5b, 6c, 7b, and 9 of Part I. LLCs should follow the instructions that apply to their tax filing status in the reference periods.

I am applying for a Second Draw PPP Loan amount greater than $150,000. When do I need to provide the documentation to substantiate the reduction in gross receipts?

For a Second Draw PPP Loan amount greater than $150,000, the applicant must provide documentation substantiating the reduction in gross receipts with its Second Draw Borrower Application Form (SBA Form 2483-SD or lender’s equivalent form). The documentation must support the amounts provided in the application.

I am an applicant for a Second Draw PPP Loan amount of $150,000 or less. When do I need to provide the documentation to substantiate the reduction in gross receipts?

For a Second Draw PPP Loan amount of $150,000 or less, the borrower must provide documentation substantiating the reduction in gross receipts before or at the time the borrower seeks loan forgiveness (or upon SBA request).

The documentation must clearly identify both of the reference quarters (if not using annual comparison), must contain the gross receipts amounts for both quarters, and support the amounts provided.

Can I document my reduction in gross receipts with income tax returns if my entity files taxes on the basis of a fiscal year that differs from the calendar year?

Entities that use a fiscal year to file taxes may document a reduction in gross receipts with income tax returns only if their fiscal year contains all of the second, third, and fourth quarters of the calendar year.

I am a self-employed individual who is eligible to use gross income from both Schedule C and Schedule F to calculate loan amount, how do I calculate the percentage reduction in gross receipts for a Second Draw PPP Loan?

Add the gross receipts for your Schedule C business with the gross receipts for your Schedule F business together and compare this sum against the sum of your gross receipts for your Schedule C and Schedule F business gross receipts for the reference period you choose (either quarterly or annually).

I am self-employed and have no employees. How do I calculate my maximum Second Draw PPP Loan amount if I use net profit?

Step 1: Find your 2019 IRS Form 1040 Schedule C line 31 net profit amount. 9 If this amount is over $100,000, reduce it to $100,000. If this amount is zero or less, you are not eligible for a PPP loan.

Step 2: Calculate the average monthly net profit amount (divide the amount from Step 1 by 12).

Step 3: Multiply the average monthly net profit amount from Step 2 by 2.5.

I am self-employed and have employees. How do I calculate my maximum Second Draw PPP Loan amount (up to $2 million) if I use net profit?

The following methodology should be used to calculate the maximum amount that can be borrowed if you are self-employed with employees, including if you are an independent contractor or operate a sole proprietorship, and you use net profit.

I am a self-employed farmer or rancher who reports my income on IRS Form 1040 Schedule F. What documentation must I provide in place of Schedule C and how should my maximum Second Draw PPP Loan amount be calculated.

Self-employed farmers and ranchers (i.e., those who file IRS Form 1040 Schedule F and then report Schedule F income on IRS Form 1040 Schedule 1) should use IRS Form 1040 Schedule F in lieu of Schedule C.

How do partnerships apply for Second Draw PPP Loans and how is the maximum Second Draw PPP Loan amount calculated for partnerships?

Step 1: Compute 2019 payroll costs by adding the following: o 2019 Schedule K-1 (IRS Form 1065) Net earnings from self-employment of individual U.S.-based general partners that are subject to self-employment tax, multiplied by 0.9235,13 up to $100,000 per partner; 14.

Compute the net earnings from self-employment of individual U.S.-based general partner that are subject to self-employment tax from box 14, Code A of IRS Form 1065 Schedule K-1 and subtract (i) any section 179 expense deduction claimed in box 12; (ii) any unreimbursed partnership expenses claimed; and (iii) any depletion claimed on oil and gas properties.

If this amount is over $100,000 for a partner, reduce it to $100,000; • if this amount is less than zero for a partner, set this amount at zero; o 2019 gross wages and tips paid to employees whose principal place of residence is in the United States (if any), up to $100,000 per employee, which can be computed using.

2019 IRS Form 941 Taxable Medicare wages & tips (line 5ccolumn 1) from each quarte.

Plus any pre-tax employee contributions for health insurance or other fringe benefits excluded from Taxable Medicare wages & tips.

Minus (i) any amounts paid to any individual employee in excess of $100,000, and (ii) any amounts paid to any employee whose principal place of residence is outside the United States; o 2019 employer contributions for employee (but not partner) group health, life, disability, vision, and dental insurance, if any (portion of IRS Form 1065 line 19 attributable to those contributions).

2019 employer contributions to employee (but not partner) retirement plans, if any (IRS Form 1065 line 18); and o 2019 employer state and local taxes assessed on employee compensation, primarily state unemployment insurance tax (from state quarterly wage reporting forms), if any.

Step 2: Calculate the average monthly payroll costs.

I am an LLC owner. Which set of instructions applies to me?

LLCs should follow the instructions that apply to their tax filing status in the reference period used to calculate payroll costs (2019 or 2020)—i.e., whether the LLC filed (or will file) as a sole proprietor, a partnership, or a corporation in the reference period.

What other documentation can an applicant provide for the purpose of substantiating payroll costs used to calculate the applied-for Second Draw PPP Loan amount?

An applicant may provide IRS Form W-2s and IRS Form W-3 or payroll processor reports, including quarterly and annual tax reports, in lieu of IRS Form 941. Additionally, very small businesses that file an annual IRS Form 944 or agricultural employers that file an annual IRS Form 943 should rely on and provide IRS Form 944 or IRS Form 943 in lieu of IRS Form 941.

If I used payroll costs from the prior 12 months when computing my First Draw PPP Loan amount, can I continue to use those figures to compute my Second Draw PPP Loan amount?

No, payroll costs from the precise 12-month period prior to the First Draw PPP Loan cannot be used to compute the Second Draw PPP Loan amount.

Any borrower that used payroll costs from the prior 12 months when computing its First Draw PPP Loan amount can calculate the amount for its Second Draw PPP Loan amount using calendar year 2019 or calendar year 2020 payroll costs. 25 A borrower that used calendar year 2019 for its First Draw PPP Loan amount may continue to do so.

Can I enter NAICS code 72 on my Second Draw PPP Loan application if the business activity code line was left blank on my business’s most recently filed income tax return?

If an entry for this line is missing from your tax return, you should report the industry code that is most applicable to your business’ primary business activity. If your business is in the Accommodation and Food Services sector (e.g., a hotel, restaurant, bar), you can only report a NAICS Code beginning with 72 if you can substantiate this with alternative documentation, such as permits or licenses issued by local governments that are unique to this sector.

In addition to pre-tax employee contributions for health insurance, what are the other pre-tax employee contributions for fringe benefits that may have been excluded from IRS Form 941 Taxable Medicare wages & tips that is part of employee gross pay?

Employee contributions and deductions from pay for flexible spending arrangements (FSA) or other nontaxable benefits under a section 125 cafeteria plan, qualified transit or parking benefits (up to $270 a month), and group life insurance (for up to $50,000 of coverage) may have been excluded from IRS Form 941 Taxable Medicare wages & tips.

However, pre-tax employee contributions to retirement plans are included in Taxable Medicare wages & tips and should not be added to that figure to arrive at gross pay.

How Can Deskera Assist You?

With all this data, you need software that can help you manage it. With Deskera, you get a dedicated bookkeeper and powerful reporting software for a clear view of your financial health.

Key Takeaways

- A forgivable loan is a type of loan that allows borrowers to have the balance of their loan either partially or totally forgiven if they meet certain conditions.

- Steps to fill application 2483-SD, fill your basic information, update loan amount calculation, reduction in the gross receipts, ownership, update your demographic information, fill the questionnaire, and certification.

- Businesses must spend at least 60% on payroll costs to get a second-draw PPP loan forgiven.

- PPP funds and other state and federal government grants are not included in gross receipts.

- You can receive a second draw loan after your first loan has been fully used, and you do not need to have the first loan forgiven before the second loan.

- Industries assigned to NAICS code 72 (lodging and restaurants) may receive loans up to 3.5 months of average monthly payroll costs for their second draw PPP loan.

- PPP funds and other state and federal government grants are not included in gross receipts.

- You can receive a second draw loan after your first loan has been fully used, and you do not need to have the first loan forgiven before the second loan.

- Eligibility for a second draw loan is not based on relative FTE counts.

Related Articles: