Did you know? It is required to link your Aadhaar with your EPF account as of June 1st, 2021. The employer's contribution will not be credited to your account if this is not done.

To contribute to the EPF, you and your employer must each transfer 10% or 12% of your basic pay.

For the first three years, however, if you are a woman, you only need to contribute 8% of your basic salary. Your employer's EPF contribution will remain at 12 percent during this time.

First of all you should know what a Provident Fund is!

Table of contents

•What is a provident fund?

•What is the Employees' Provident Fund?

•Universal Account Number

•How does EPF work?

•EPFO Services

•What are the Eligibility Criteria for EPF?

•PF Withdrawal Online

•Procedure to know the EPF number

•New EPF Withdrawal Rules 2022

•When can you use Form 19?

•Reasons for PF withdrawal

What is a Provident Fund?

A retirement savings plan for salaried employees who work for a company with 20 or more employees is known as an Employee Provident Fund (EPF).

All employers are required to contribute a part of their employee's salary to the Employee Provident Fund Organization of India, or EPFO. Employers are also obligated to contribute to the provident fund a part of their earnings.

The primary goal of the EPF system is to ensure that when an employee retires or becomes unable to work due to disability, he or she would have a substantial sum of money.

What is the Employees' Provident Fund?

The term for Employees' Provident Fund (EPF) is Employees' Provident Fund. It's a retirement savings plan in which the employer and employee both contribute equally. Both of them must contribute about 12% of their basic pay to this fund.

An employee receives a lump sum payment plus interest when he or she retires.

EPF contributions are required of both the employee and the employer. Employees' dearness allowance and basic salary are each put into the EPF at a rate of 12%. The contributions made by employees and employers to the EPF are listed below.

In India, the Employees' Provident Fund and Miscellaneous Provisions Act of 1952 is a long-term savings plan. Employees in the organized sector who are eligible for retirement benefits can participate in the program.

It requires an employee to contribute to a provident fund account, as well as an equal contribution from their employer. To withdraw funds from this scheme, you must complete EPF Form 19 and submit it along with additional papers.

EPFO (Employee Provident Fund Organization)

The EPFO (Employees' Provident Fund Organisation) is a non-constitutional organization that encourages employees to save for retirement. The Ministry of Labour and Employment, Government of India, oversees the organization, which was founded in 1951.

Both Indian and international workers can benefit from the organization's programs (from countries with whom the EPFO has signed bilateral agreements).

Universal Account Number

Members of the Employees' Pension Fund (EPF) can access their accounts online and perform functions such as making withdrawals and checking their balance. The Universal Account Number makes it easier to log into the EPFO member portal (UAN).

Each EPFO member is given a 12-digit number known as the UAN. An employee's UAN remains the same even if he or she moves jobs. When a job is changed, the member ID is updated, and the new ID is linked to the UAN. However, before using the online services, employees must activate their UAN.

Your employer can provide you with a UAN. If you are unable to do so, simply login to the UAN site using your member ID and search for the UAN.

Why is UAN important?

All EPF-related services are now available online, thanks to the digitization of the Employee Provident Fund (EPF). To access EPF information and services, you must first obtain a UAN.

Employees can use the UAN to complete a range of EPF-related operations online in a short amount of time, such as EPF withdrawal, EPF transfer from one account to another, checking EPF account statements, accessing EPF account passbooks, and applying for an EPF loan.

How does EPF work?

Step 1: From your salary EPF deductions are made

Everyone who has worked as a salaried employee is aware that our monthly payment is subject to a variety of deductions. The Employee Provident Fund is one such deduction, which is clearly stated on your payslip.

So, what is the PF procedure exactly? According to EPF guidelines, you must contribute 12% of your salary to your provident fund.

Your firm must also contribute the same 12 percent, with 8.33 percent going to the Employee Pension Scheme, or EPS. The remaining 3.67 percent is invested in your EPF account.

Step 2: All EPF funds are pooled

A trust pools the cash collected from you and all other employees and invests them. The pooled funds also earn interest at a rate set by the government, which ranges from 8% to 12%.

Due to your monthly donations as well as the yearly compound interest, this amount continues to grow. The EPF will continue to work until you opt to withdraw it when you retire.

Step 3: Withdrawal of Employee Provident Fund

There are two primary methods for withdrawing your provident fund.

The first is when you reach the age of 58, which is considered retirement age. You can apply to withdraw your Employee Provident Fund through your employer once you've attained retirement age.

The second option is to take money out of your EPF before you reach retirement age. If you've been unemployed for a month, you're permitted to withdraw 75 percent of your provident fund. It should be emphasized, however, that the employer's contribution to the provident fund can only be withdrawn once.

How to update Father Name of EPF UAN Account?

If you have a UAN account, make sure your father's name is spelled correctly. The service isn't available on the internet. A Joint Declaration Form must be completed and signed by the employer and sent to the EPF service office.

If you are unable to withdraw any funds, your next nominee, your father, will be entitled to do so. Your father's name on your PF account must match the name on your proofs to ensure that the process is completed correctly.

If the request is denied by the company, you can write to the UAN email directly.

What is EPF Form 19?

The objective of EPF Form 19 is to withdraw PF funds when you retire or quit your employment. After two months from the date of retirement, an employee can fill out Form 19 to receive the settlement sum. However, if an employee transfers to another company within this time, the PF balance is automatically transferred to the new account.

Claim Form 19 Pf

Claim Form 19 pf is only for employees who do not have a UAN. For all employees who made a PF contribution after 2014, the EPFO has issued a UAN. If an employee has only paid PF contributions before 2014, he or she can apply for a UAN at the nearest EPFO office.

It is also possible to file PF Claim Form 19 without a UAN by simply stating the PF Account Number. However, it is advised that all employees with a PF account establish a UAN to consolidate their accounts.

Attestation of Employer

The employer must attest to the PF claim form 19. In addition, the employee must produce a copy of the canceled check or an attested copy of the first page of their bank passbook to authenticate the bank account from which the PF withdrawal will be made.

The application can be submitted to the local EPFO office once it has been completed and signed by both the employee and the employer.

TDS on PF Withdrawal

Employees can check on the status of their PF claim via the PF website, the UMANG app, or by calling the PF office after applying. If the service is less than 5 years, TDS will be deducted from PF withdrawals at a rate of 10% if the member provides a PAN or 34.60 percent if no PAN is provided. TDS will not be deducted if the total balance is less than Rs. 50,000/-.

EPF e-Nomination

EPFO has made it compulsory for EPF members to file nomination data. Its objective is to ensure that, in the unfortunate case of a member's death, the family receives the proper funds that the individual has accumulated during his or her employment tenure.

This is a task that can be completed both online and off. Members of the UAN who have not submitted their e-nominations will not be allowed to access their passbooks on the internet.

To register an e-nomination, an EPFO member must provide the following information: Aadhaar number, name, date of birth, gender, relation, address, bank account information, and a photograph. The e-Sign facility must then be used to verify the submitted information.

EPFO Services

The EPFO provides a variety of services, which are listed below:

Inoperative Accounts Online Helpdesk - The EPFO established the Inoperative Accounts Online Helpdesk in February 2015 to assist staff in tracking inactive and old inoperative accounts that do not earn interest.

Employees can monitor these accounts and withdraw or transfer funds to the current Member ID. To track inactive accounts, employees must submit basic information about their prior employment.

Online EPF withdrawal - With the use of the UAN, you can quickly withdraw your EPF funds online. Employees who have been unemployed for more than two months may withdraw their EPF funds. However, the employee's Aadhaar and bank account information must be linked to the UAN.

International employees can get a Certificate of Coverage - EPF members working in countries with Social Security Agreements with India can get a Certificate of Coverage (CoC) via the EPFO's newly launched online centralized software.

Establishments can register online using the EPFO portal's Online Registration of Establishments (OLRE). Employees benefit from the online availability of the PF code allotment letter.

Payments to the pension fund must be made electronically by all enterprises. Kotak Mahindra Bank, Axis Bank, ICICI Bank, HDFC Bank, Union Bank of India, Indian Bank, Punjab, and State Bank of India are among the EPFO's current banking partners (SBI).

EPFO members will be able to monitor the status of their claims as well as view and download their EPF passbook via the app.

Members can file a complaint online if they have a problem with their pension, a transfer of PF, or a withdrawal of PF, for example. Grievance resolution is a key priority for the EPFO, and it is handled quickly.

Eighty percent of complaints are resolved within seven days, and ninety percent are resolved within fifteen days. Complaints have decreased from 20,000 to 2,000-3,000 per day as a result of continual monitoring of EPF issues.

What are the Eligibility Criteria for EPF?

The following are the EPF eligibility requirements:

Any business with more than 20 employees is required to register with the Employees' Provident Fund Organisation of India. Companies with less than 20 employees can voluntarily join the Employees' Provident Fund. EPF benefits are available to all salaried employees.

Furthermore, all employees earning less than 15,000 are required to join the EPF. Employees earning more than 15,000, on the other hand, might choose to remain in the EPF plan freely.

What are EPF Tax Rules?

EPF is a tax provision that applies to EEE. As a result, it is tax-free on EPF withdrawals. In addition, contributions and interest received are tax-free. However, EPF is taxable in particular circumstances. These are the following:

If an employer contributes more than 7.5 lakhs to the Employees' Provident Fund in a fiscal year, it is taxed. An employee who earns more than 7.5 lakhs is required to pay tax.

If an employer does not contribute to an EPF account, as is the case for government employees, the interest earned is tax-free up to a limit of 5 lakhs every financial year.

Employees must pay taxes on interest earned on dormant EPF accounts.

Withdrawals from the Employee Provident Fund account are tax-free unless they are made after less than 5 years of continuous service. TDS is applied at a rate of 10% if any withdrawal amount exceeds 50,000.

Withdrawals may be permitted in the event of an employee's illness, the closure of a business, or other factors beyond the employee's control.

Importance of updating the exit date

It's critical to keep your leaving date up to date for claim filings and settlements. If your leaving date isn't updated or is incorrectly stated, your employment won't be considered continuous, and you'll have to pay tax on the interest you earned during that time.

PF Withdrawal Online

Partially withdrawing from the EPF account for the purchase of a home, wedding expenditures, or medical expenses is possible. The amount that can be removed is determined by the cause of the withdrawal. It's worth noting that partial withdrawals have a lock-in period, which varies depending on the reason for the withdrawal.

Under some conditions, the whole PF balance can be withdrawn. Retirement age, resignation owing to permanent total mental/physical disability, permanent relocation to other countries, death of the member are just a few examples.

Some of the reasons why EPF should not be withdrawn before 5 years of service are listed below.

Advantages under Section 80C of the Income Tax Act are not available: If individuals claim benefits under Section 80C of the Income Tax Act and withdraw their PF amount, the interest gained on the employee's contribution must be taxed.

The amount will be taxed: If a PF withdrawal is made within the first five years of employment, the amount is added to the taxable income.

If the amount withdrawn is more than Rs.50,000 and the withdrawal is made within 5 years, the amount is subject to a 10% tax reduction. Individuals are exempt from paying this sum if they file Forms 15G and 15H with the Income Tax (IT) Department.

EPF withdrawal without employer signature

After discovering that obtaining an employer's consent or attestation to assist a PF withdrawal was causing a lot of headaches for many employees, the EPFO bypassed the process and now employees can make withdrawals without their employers' attestation.

This shift was brought about by the introduction of the UAN in the EPF, as employees now only need to link their Aadhaar card to their UAN to make a withdrawal. After that, there are two options for making a withdrawal without the employer's signature: with or without an Aadhaar card.

EPFO digital signature

The EPFO has introduced the digital signature of employers to make the procedure of transfer claims easier and more transparent. Employers can now use their digital signatures to approve claims.

When an employer changes companies, his transfer claim must be attested by either his prior or current employer, which is where the employer's digital signature comes into play. Employers have to fill out Form 13 and get it signed by their bosses before sending it to the regional EPF office.

The procedure has been simplified, and it may now be completed through the EPFO's member site. Employers must apply for a digital certificate, which comprises their personal information such as their name, email address, APNIC account name, public key, and the employer's nationality.

The Certifying authority issues the digital certificate, which comprises this identification key as well as their required details, which will be incorporated in the EPFO's member portal.

EPFO grievance

Employees who want to raise a complaint can do so using the EPFO's member site, which has a specific section for them to fill out a grievance registration form and file a complaint. Employees frequently have complaints about withdrawals, PF settlements, account transfers, and pension settlements, among other things.

How to Transfer EPF Online?

Step 1: Use your UAN and password to log in to the EPFO members' site.

Step 2: Select 'Transfer Request' from the 'Online Services' item on the main menu of the home page to create an online transfer request.

Step 3: A new dashboard will appear, revealing all of your personal information. Verify everything, including your DOB, EPF, and date of hire, to claim the process.

Step 4: After you've verified, proceed to Step 1 and select the choice of past or current employer, then enter the information for the previous employer you want to claim through.

Step 5: An OTP will be sent to the phone number you entered when you submit the information. After verifying your identity with the OTP, the request will be received and an online filled-in form will be generated. You must sign the documentation and return it to your current or previous employer.

Step 6: The EPF transfer request will be sent to the employer via email. The EPFO will handle your claim only if your employer digitally uploads it to the EPFO after validating your employment data.

Important Considerations When Filling Out Form 19

• Only two months after quitting a job or upon retirement can the paperwork be completed

• For the final payout, the employee must submit his mobile phone number

• The form 19 can be completed both online (at the EPF Member Portal) and offline (at the EPF Member Portal)

• PAN is also required for final settlement claims

• The offline settlement method requires the employer's signature and the organization's seal

• The signatures of both the member and the employer are required

• When you need to pay by check, you must fill out an advance stamp receipt. An advance stamp requires you to place a one-dollar revenue stamp on the form 19 and sign across it. You don't need an advance stamp on form 19 if you use the ECS option (electronic credit)

• At the start of the form, the employee must submit his mobile phone number

• Form 19 must be filled out and submitted by anyone who intends to withdraw funds for final settlement. Form 19 can be used for a variety of purposes, including PF final settlement, pension withdrawal benefits, and PF non-refundable advance

• While the first two alternatives can be chosen at the time of retirement or other termination of employment, the third option can be employed at any time throughout service as long as specified restrictions and conditions are met.

Employee PF Account Number

Employees can use their Employees' Provident Fund Account Number to check the status of their EPF, the balance in their EPF account, and so on. For EPF withdrawals, the number is required.

Employees who have not kept track of their monthly contributions to the plan may not be aware of their EPF number. Employers may fail to tell employees of their PF number. Employees should be aware of their PF number while on the job, as obtaining it after they have left the company or retired may be difficult.

Procedure to know the EPF number

The employer is in charge of inputting new employees' information, allocating EPF numbers, and ensuring that EPF contributions are made on time. As a result, the employer plays an important part in the EPF plan, and employees must obtain their EPF account number.

If the employer fails to furnish the employee with his or her EPF number, the employee may receive it through one of the following procedures:

By visiting the EPFO office: Employees can obtain their EPF account number by visiting the EPFO office. The employee must provide all necessary personal information to obtain the account number. The employee must keep proof of identity on them at all times and complete the application.

Employees can acquire their EPF account number on the EPFO portal if they have their UAN number. By logging into the EPFO portal, employees can see all of their PF information.

Employees can get their PF account number by contacting their company's Human Resources department.

Examining the employee's pay stub: The employee's EPF account number is usually included on the payslip.

Format of EPF Account Number

The EPF Account Number is made up of both digits and alphabets. The EPF account number also contains information about the EPF office, which is responsible for all of the employee's EPF account processes, as well as the organization's code.

When can you use Form 19?

If you wish to get your EPF money in the form 19 of a final settlement, you'll need to fill out Form 19. The same form can be used to apply for a non-refundable PF advance as well as to receive pension payments.

The first two alternatives may be considered when quitting a job for any reason other than retirement. The last option, on the other hand, can only be used during service if a series of circumstances are met.

Within two months of leaving the position, form 19 must be filed.

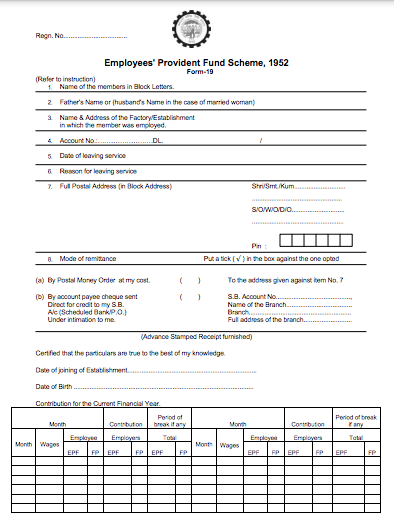

How Does Form 19 Look?

The first page of EPF Form 19 has various fields for you to fill out with your personal and contact information, as well as your preferred payment method.

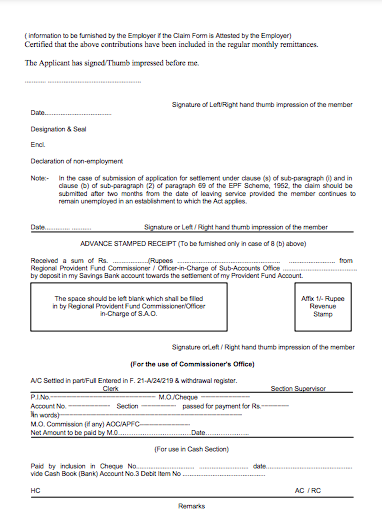

The second page is an advance stamped receipt that must be completed only if you are paying with a cheque and an Rs.1 revenue stamp. Here's an example of the first page of the form 19.

Both the member's and the employer's signatures are required on form 19.

You must fill out an advance stamp receipt when paying by check. You must apply an advance stamp to the form and sign across it with a one-dollar revenue stamp. If you utilize the ECS option, you won't require an advance stamp (electronic credit).

The employee must enter his mobile phone number at the beginning of the form 19.

EPF Form 19 is also known as the Composite Claim Form. The following are the two types of Form 19:

Employees who have their Aadhaar number and bank account information on the UAN website are eligible. Employees must fill out the entire new Form 19 and have a valid UAN.

Non-Aadhaar based: Employees who do not have an Aadhaar number or an active UAN can use this option of filling form 19.

Form 19

How to Fill PF Settlement Form Online

To settle a PF account, the individual must complete and submit Form 19. This form is easy to get and may be obtained on the official website of the EPF. Form 19 must be completed if you want to withdraw your PF balance.

A member must fill out Form 19 to settle his PF account. A member must fill in the necessary information before submitting the form to his or her old employer.

Salaried workers may forget their EPF account numbers for a variety of reasons, in which case they should submit a formal request to their company's human resources department, which will then contact their former employers.

Members can contact their former employers directly to obtain the information they require. In other cases, ex-employers may seal their doors, and paid employees may have left their workplaces under difficult circumstances, making it difficult for them to contact their former employers.

Members can still complete their PF Settlement Form (form 19), which must be attested by their bank manager. Members must provide personal information in addition to confirming their identification on form 19.

Form 19 should next be submitted to the regional PF manager for permission and verification (see the official EPF website's 'establishment search' link for more information).

How can you check the EPF balance of an Exempted establishment?

Because the EPF contribution goes to the company-managed trusts rather than the Employees' Provident Fund Organisation in the case of an exempted establishment or private trust, only the company-managed trust can divulge an employee's PF account balance.

When it comes to EPF accounts kept with exempted establishments, there is no common way for checking PF balance. Members of exempted establishments do not have access to the EPFO's passbook system.

Some employers can run their own PF systems for their employees under the Employee Provident Fund and Miscellaneous Provisions Act, 1952. Large firms with in-house EPF trusts, such as Godrej, HDFC, Nestle, Wipro, TCS, Infosys, and others, are excused from donating their EPF corpus to the EPFO.

The EPF corpus can be managed by certain exempted enterprises through their trusts. These trusts, on the other hand, are likely to outperform the EPFO-managed fund. The same restrictions apply to these trusts as they do to EPF contributions to EPFO.

Employees of these exempted businesses have four options for checking their EPF balance:

Check your PF slip: Most large companies provide salary slips to their employees via email. Employees can check their EPF account balance on their payslips.

In addition to the salary slip, some employers provide an EPF slip. Employees will see their monthly contributions as well as the balance of their EPF account on that slip.

Check the company's employee portal: Most large firms have a website where employees may log in and check the balance of their EPF account under the EPF area. Wipro and TCS are two examples of firms that offer the ability to monitor one's EPF account balance and obtain a PF statement via the internet.

Employees should contact the company's HR department because it handles the employees' PF and is better able to offer the necessary information.

Employees can calculate their annual EPF balance by looking at their pay stubs and keeping track of their monthly payments. Use the EPFO's interest rate when calculating EPF interest. Remember that the EPS account is given a specific quantity of money.

EPF Balance for inoperative Accounts

According to a government notification released in November 2016, even dormant accounts will continue to accumulate interest and will no longer be categorized as inactive. Since 2011, the EPFO has stopped paying interest on dormant accounts.

However, after the new amendment takes effect, all inactive accounts will receive an annual interest rate of 8.5 percent. The contribution will be made until you reach the age of 58, or until you withdraw your money, whichever comes first.

Previously, accounts became inactive due to two factors: the time-consuming formalities required in EPF transfer and employees preferring to register new accounts when changing jobs.

A communication gap between an individual's present and prior employers also plays a significant role in this. Employees who are unable to locate the details of their former inactive accounts can contact the EPFO support desk and request that the balance in those accounts be moved to their current account.

New EPF Withdrawal Rules 2022

In the EPF account, employer and employee contributions are combined. On the other hand, money in an EPF account cannot be withdrawn at any time.

Here are important guidelines to keep in mind while withdrawing from your EPF:

• Money from an EPF account, unlike a bank account, cannot be withdrawn while employed. The Employees' Pension Fund (EPF) is a long-term savings plan for retirees. The savings can only be withdrawn after retirement

• Partial withdrawals from EPF accounts are permitted in the event of an emergency, such as a medical emergency, property purchase or construction, or higher education. Partially withdrawing funds is restricted depending on the reason. The account holder can request a partial withdrawal electronically

• Early retirement is not considered until a person reaches the age of 55, even though the EPF corpus can only be collected after retirement

• The EPF corpus can be withdrawn if a person is laid off before retirement due to lock-down or retrenchment

• After one month of unemployment, EPFO's new rule allows for the withdrawal of 75% of the EPF corpus. The remaining 25% can be moved to a new EPF account once you've found new work

• The old rule allowed for a 100% EPF withdrawal after two months of unemployment

• Withdrawals from an EPF account are tax-free if certain conditions are met. An employee is only qualified for a tax exemption on the EPF corpus if he or she has contributed to the EPF account for five years in a row

• The amount is taxed if there is a five-year gap in contributions to the EPF account. In that case, the whole EPF balance will be deemed taxable income for that fiscal year

• Tax is deducted at the source when an EPF corpus is prematurely withdrawn. If the entire sum is less than Rs.50,000, however, TDS is not imposed. Keep in mind that the TDS rate is 10% if an employee supplies their PAN with the application

• Otherwise, it will be 30% plus tax. Form 15H/15G is a declaration form that declares a person's entire income is not taxable, allowing them to avoid paying TDS

Employees are no longer need to obtain authorization from their employer before withdrawing their EPF funds. It can be done immediately through the EPFO if the employee's UAN and Aadhaar are linked and the employer has accepted it.

Steps to quickly enter your leave date and withdraw your Provident fund

Your Provident Fund (PF) withdrawal may be taking longer than planned because the exit date was not selected. To get around this, the Employees' Provident Fund Organisation (EPFO) has added a function to the Unified Portal that allows employees to manually enter the date of their previous work departure. Employees can now enter their exit date, which was previously only available to the employer.

You can change the exit date by logging into the UAN site with your Unified Account Number (UAN) and password. You must, however, verify the 'Service History' section of the top panel under 'View' to see if the exit date is listed.

Tax-Free Limit for PF Withdrawals

When you withdraw money from your PF account, you may be eligible for tax benefits. However, this only applies if you leave after five years of continuous service. It's also determined by the tax bracket you're in.

However, depending on the circumstances, there may be no tax on EPF withdrawals made before the fifth year.

Online Grievances Portal for PF Withdrawal

You can use the online EPF grievance management system to make a complaint if you are dissatisfied with the EPFO's services. This system allows you to file a complaint, send a reminder, follow the status of your complaint or grievance, submit your grievance papers, and even change your password.

What rules should be followed by employees while withdrawing EPF?

EPFO has outlined a variety of PF withdrawal limits to ensure that employees remain engaged in the plan and do not take funds from their PF accounts to save money for the future or retirement.

• Withdrawals done before five years of continuous service are subject to taxation. Withdrawals from the EPF are tax-free after 5 years of continuous service

• If an employee has been fired or is unemployed due to illness or other reasons, withdrawals will not be taxed

• If an employee withdraws from the plan before completing five years of continuous service, the principal amount, as well as any accrued interest, is liable to tax. The money will, however, be taxed in the current fiscal year

• If the employee does not present his or her PAN to the EPFO authorities before completing 5 years of continuous contributions to the program, he or she will be taxed 30% of the principal amount and interest accrued

• If the employee has provided the EPFO with his or her PAN number, a 10% TDS (tax deducted at source) will be applied

• When money is transferred from a PF account to the National Pension Scheme (NPS), it is not taxed when it is withdrawn

• If an employee changes jobs and opens a new PF account in the process, it will be deemed continuous service to the plan as long as there is no break in contributions.

• Employees must make the Composite Claims Form as easy to use as possible when filing a partial withdrawal or final settlement claim

• If the employee has linked his or her Aadhaar card to their UAN, they can use the Composite Claims Form to make a direct withdrawal from the EPFO without the need for their employer's certification

To make a withdrawal, those who have not seeded their Aadhaar card details with their UAN must submit the Composite Claims Form along with their employer's certification

Provident Fund Withdrawal Procedure

Subscribers to the Employees' Provident Fund Organization (EPFO) no longer need their employer's permission to make a partial or complete withdrawal, thanks to EPFO revisions.

All the subscriber has to do is make sure their UAN is seeded with their Aadhaar card information. In addition, the EPFO has released the Composite Claims Form, which can be used to request a partial or complete withdrawal.

Subscribers can complete the entire withdrawal process online, either through the EPFO member portal or the UAN site.

Provident Fund Withdrawal Claim Forms

The PF Withdrawal Claim Forms that must be submitted to withdraw the provident fund or pension fund differ according to the age of the employee, the cause for the claim, and whether or not the employee is still employed.

Withdrawals were previously made using Form 19, Form 31, and Form 10C. However, the above-mentioned forms have lately been replaced by a composite claim form.

Reasons for PF withdrawal

The circumstances in which you can withdraw money from your EPF while you are still employed

• Medical Treatment

You can take money out of your EPF account to cover the costs of medical care, as long as the following conditions are met:

Any significant procedure performed in a certain facility

More than a month has passed since the patient was admitted to the hospital.

The employee is ill with tuberculosis, leprosy, cancer, mental disease, paralysis, heart issues, and other ailments, and is on sick leave provided by his or her company.

You can withdraw money from your EPF account at any moment during your employment. To be eligible for that money, you do not need to have worked for the company for a set amount of years.

Even if you've worked for your current company for one or two years, you can always use the money for therapy.

You should also keep in mind that the maximum amount you can borrow is six months' pay. This sum may not be large, but it will provide you with some assistance if you find yourself in a crisis.

This benefit is not only available at any time, but it may also be used as many times as you like. As a result, your PF will undoubtedly rescue you.

• Marriage Purposes

If you have already completed seven years of employment, money from your EPF can be withdrawn for a special occasion such as marriage. You can spend up to 50% of the money in your EPF account, and you can take advantage of this benefit a maximum of three times.

Assume you have approximately INR 5 lakhs in your EPF account. When you want to withdraw money for your wedding, you must not compute the total amount. You only need to compute your payment to the EPF, as well as the interest accrued on it.

• Construction of house or purchase of property

When you want to buy a property or build a house, you can take money out of your EPF account. However, you must first learn a few guidelines.

If the property you want to buy is in dispute, it should first be cleared of all pending legal issues. The property must be registered, and documentation of registration must be presented as well.

• Repaying the existing home loan

If you have a home loan and want to pay it off early, you can pull money out of your EPF. To be eligible for this benefit, you must have served for ten years. However, you can only take advantage of this benefit once in your lifetime.

You can also utilize the EPF to either buy a house or property or pay off a current home loan. You won't be able to pay for both of them.

The property you're paying for has to be in your name, your spouse's name, or jointly owned by both of you. Many people have shared mortgages with their parents or siblings.

In such instances, you will be unable to make use of this benefit. The EPF can be used to repay an existing home loan in an amount equivalent to 36 times your monthly earnings.

• Education purposes

You may be able to withdraw some funds from your EPF for educational purposes. This benefit is only available for post-matriculation educational expenses.

This means that if you enroll your child in any institution or college, you will be entitled to withdraw funds from your EPF account. Before you may make use of this perk, you must have served for seven years.

• Alteration or Repairs of your house

After several years in a home, you may believe that it requires some maintenance. Some adjustments may be possible to make things more convenient for you.

However, this is a pricey affair that may easily burn a hole in your wallet. You may be able to use funds from your EPF for this reason. But first, you must understand a few rules.

To manage your costs and expenses you can use many available online accounting software

How can Deskera Help You?

As a business, you must be diligent with employee leave management. Deskera People allows you to conveniently manage leave, attendance, payroll, and other expenses. Generating pay slips for your employees is now easy as the platform also digitizes and automates HR processes.

Related Articles