Businesses involve the use of complex calculations and lots of numbers. Whether it is maintaining the log about the different products in the inventory or clearing the salaries of employees, the business owners are responsible for having hands-on knowledge about how to do accounting. If you are a small business owner or a budding entrepreneur it is very important to have a sound understanding of these principles.

This blog will help you delve deep into the basics with the following topics -

- What is accounting?

- What are the different accounting basics?

- GAAP Principles

- What are the basic accounting terms?

- How to do accounting for small businesses?

- Conclusion

- Key Takeaways

What is Accounting?

According to subject matter experts, accounting can be defined as the process of systematically recording, doing analysis and interpreting the financial information of a business. Business owners use this method to keep a track of the financial operations of their company and even meet legal obligations. It helps entrepreneurs make wise and stronger business decisions. Hence, it is considered to be a crucial part of the organization’s project lifecycle if the employer wants to run the business successfully.

A business owner can either choose to do this himself or even outsource it to a third party if he has not employed an accountant in the office.

What are the different accounting basics?

Irrespective of who handles the accounting of the business, every professional involved in this profession should have an understanding of its basics. If an individual can read and understand these basic documents proficiently, he will have a better understanding and full knowledge of the performance of the business. Moreover, he can know about the financial health of the company which is necessary for making further decisions to have control over the functioning of the company.

Let us understand which documents and calculations a business owner or a professional in the accounting field must be aware of -

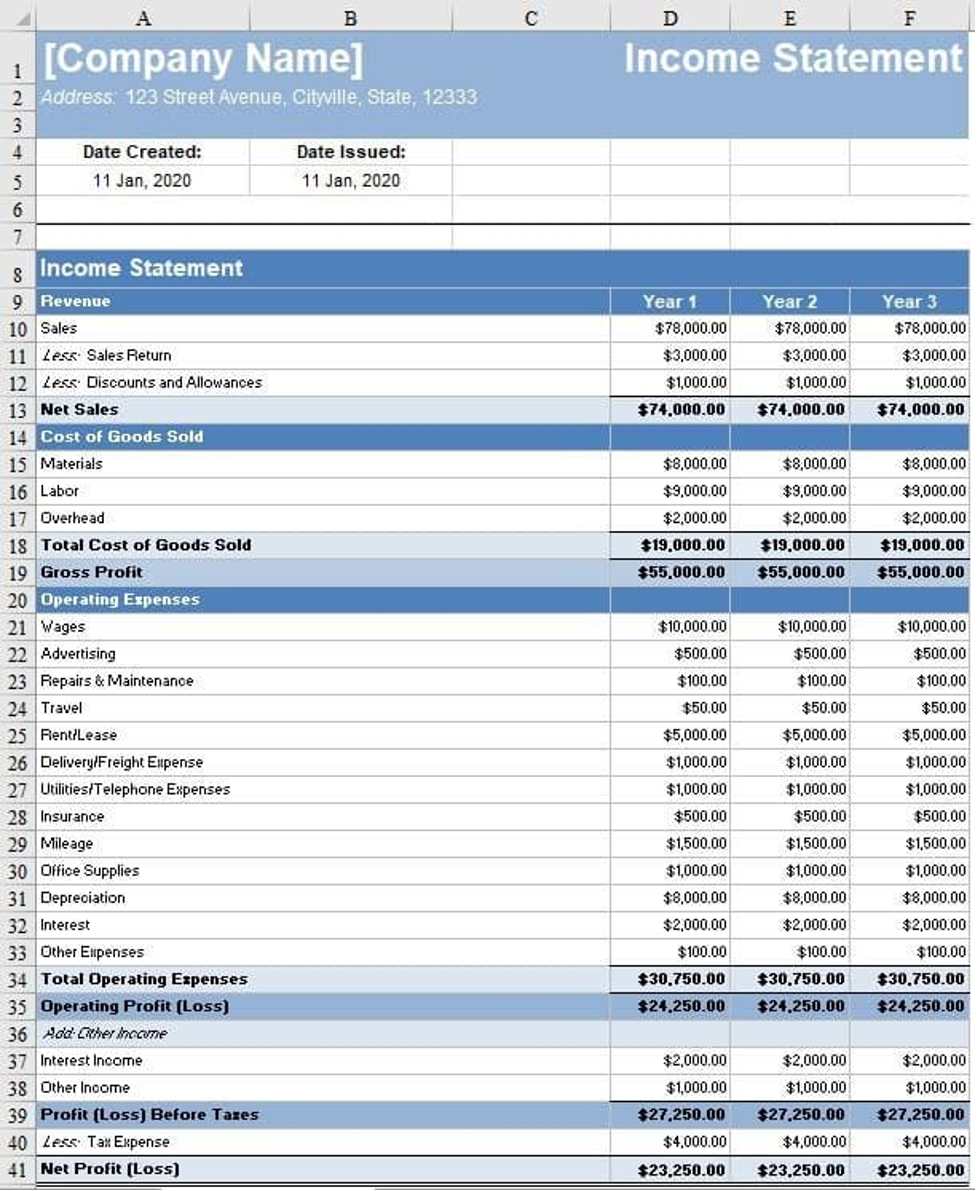

1. Income statement: In accounting, an income statement can be said to be a document that shows the company’s profitability. It lets the business owner know about how much money his business has made as well as tells about the losses.

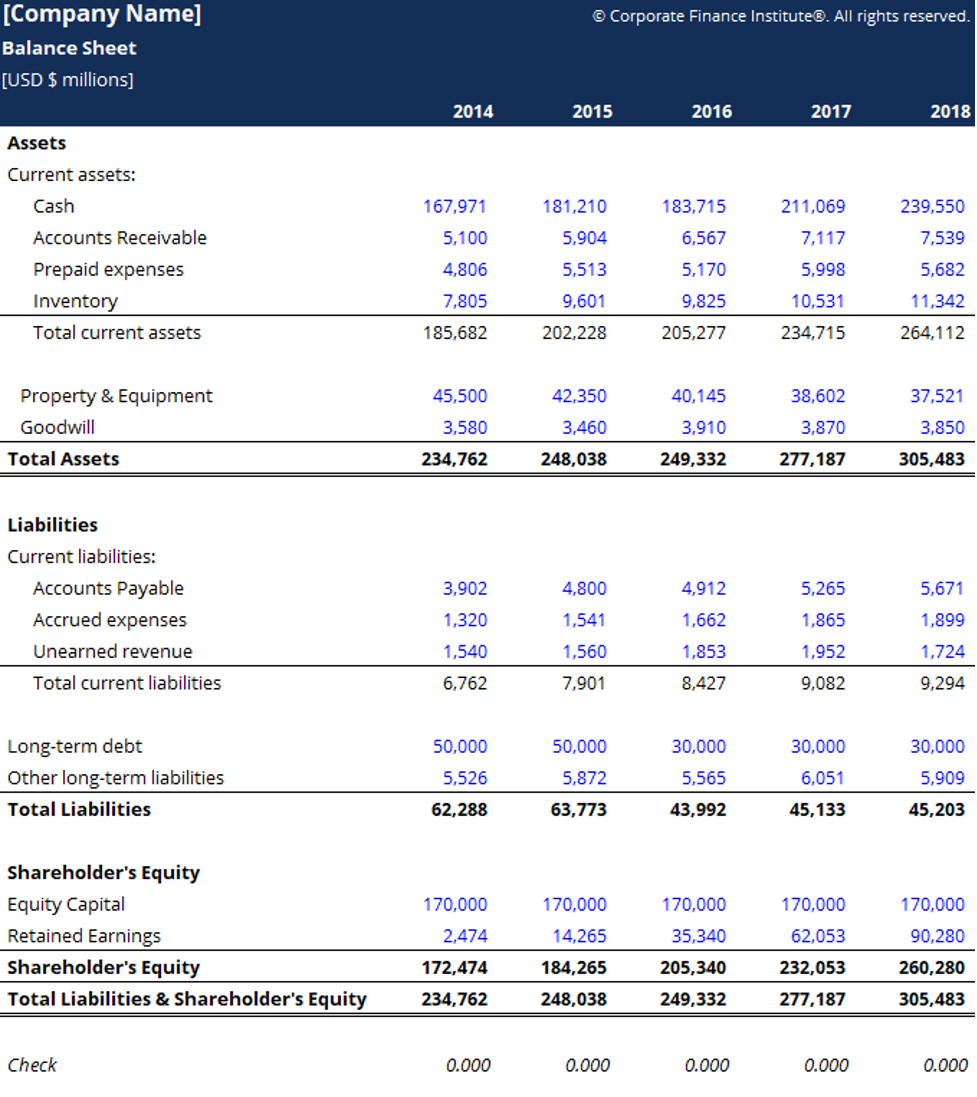

2. Balance sheet: A balance sheet can be defined as a snapshot of the business's financial standing at a single point in time. In accounting, this document can be used by the business owner to know about his retained earnings. The retained earnings can be defined as the amount of profit that the employer can reinvest in the business or even distribute to the company’s shareholders.

3. Profit and Loss (P&L) Statement: A P&L statement can be defined as a document that talks about the business income and expenses for a pre-fixed time. These calculations can be done quarterly, monthly or annually by a business owner. According to the rules, the calculations done in this statement must be reflected in the Schedule C tax document of the business.

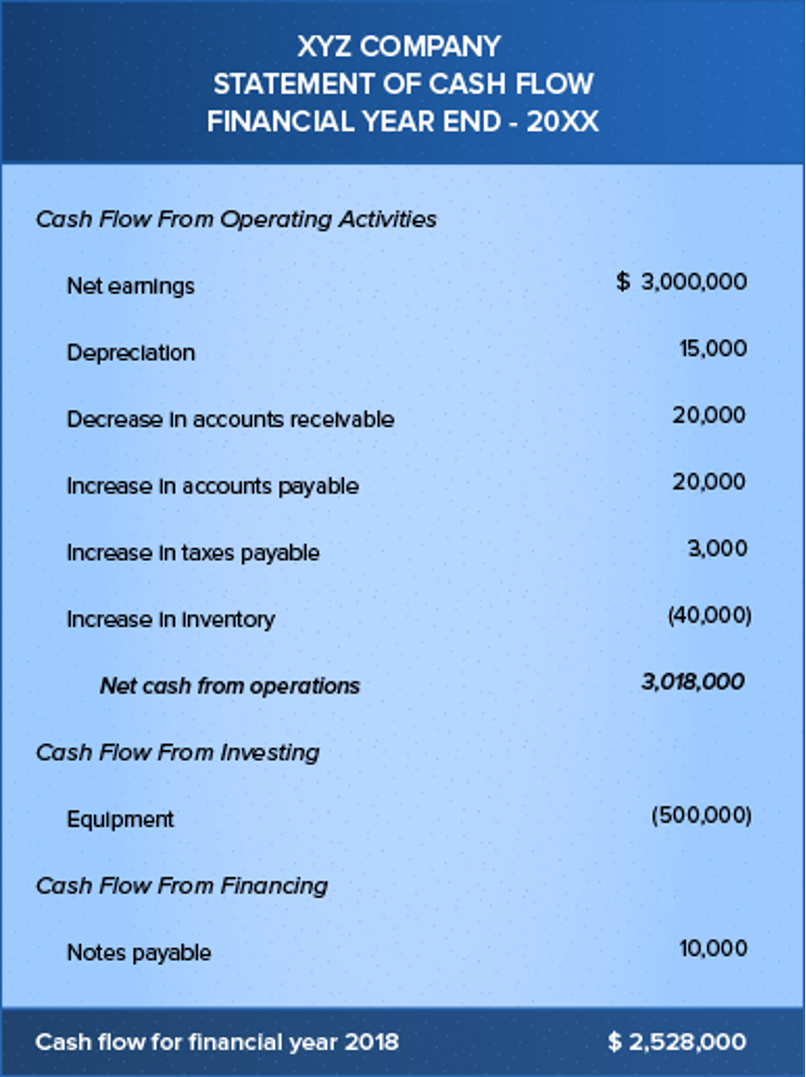

4. Cash flow statement: In accounting, a cash flow statement can be defined as a document that assists in the analysis of various activities of the business. This includes the operating, financing and investing activities involved in the business. It helps the business owner know how and where he has received the income from and even talks about the expenses that are where he has spent money on.

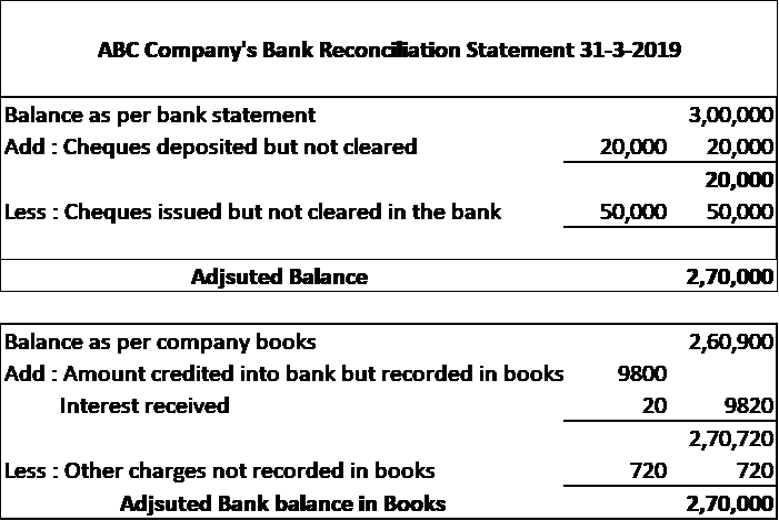

5. Bank Reconciliation: A bank reconciliation is a document that a business owner can use to compare the cash expenditures with overall bank statements. It helps the employer to keep his business records consistent. In this process, a business owner has to reconcile his bookkeeping balance with the bank balance

Accounting Principles

Once a business owner has a basic idea about the different documents in accounting, he should have sound knowledge of the basic accounting principles. These can be defined as a body of doctrines which are associated with the theory and procedures related to accounting. They can be referred to as the principles which are an explanation for the current practices followed in the business by the employer. Furthermore, these can also be looked at as an appropriate guide from which the business owner can get alternative conventions or procedures in accounting if required.

These principles should satisfy the following conditions in business -

a. It should be based on real assumptions

b. It should be simple, easy to understand and explanatory

c. The business owner needs to follow the accounting principles consistently

d. The employer must be able to reflect future predictions for his business using them

e. It should give relevant and proper information to the employees and users of the organization.

GAAP principles

According to the law, the accountants who represent the public traded companies are required to comply with Generally Accepted Accounting Principles which is abbreviated GAAP. These principles are as follows -

A. Principle of Regularity - The accountant in a business must comply with the GAAP rules and regulations.

B. Principle of Consistency - It states that in a business, an accountant or the business owner must consistently report all the information throughout the reporting process. It specifies that under this, an accountant is liable to clearly state even the minimal changes done in the financial data on the company’s financial statements.

C. Principle of Sincerity: The business owner or his accountant should give an accurate financial statement of the company and should not indulge in any discrepancy.

D. Principle of Permanence of Methods: The accountant or small business owner must follow consistent financial reporting methods across the time periods.

E. Principle of Non-Compensation: A business owner must disclose all the financial information including positive and negative business outcomes accurately. He should do a proper reporting of the financial data with no expectations regarding the compensation for the performance of the business during the period.

F. Principle of Prudence: The business owner should provide the financial data of the organization purely based on facts and not give any speculations about the same.

G. Principle of Continuity: It means a business owner has to abide by the accounting principles and states that the company will continue its operations normally.

H. Principle of Periodicity: The accountant for a small business owner or the industrialist must report the documents during relevant periods which are monthly, quarterly or yearly as decided by the employer

I. Principle of Materiality: The business owner or their accountants must aim to give full disclosure of all the financial and accounting informative data in the financial reports.

J. Principle of Utmost Good Faith: According to this accounting principle, the parties must remain honest in all business transactions.

What are the Basic Accounting Terms?

A business owner must know the 15 basic business accounting terms that he can use in his company whenever required. It would not only provide an idea about the various terms but also be of great help if the employer plans to expand his business into a new industry. Let us understand these different terms in short -

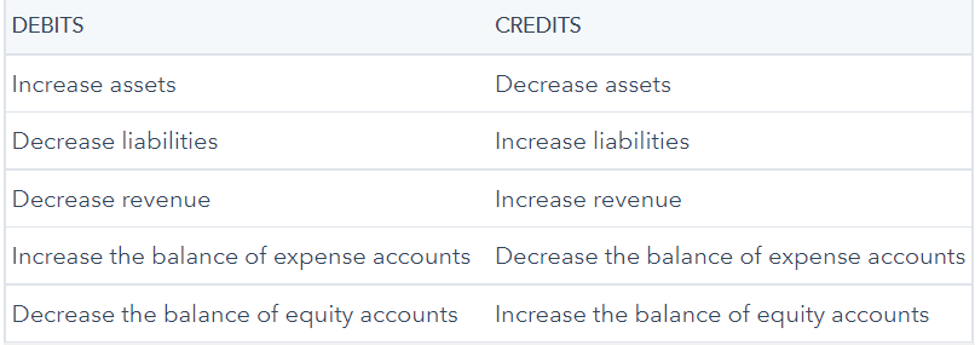

1. Debit & Credit: It is the record of all money that gets subtracted from the business account when a payment is done. In opposition to this, a credit is a record of all the money that gets deposited in the business account.

2. Accounts receivable and accounts payable: Accounts receivable is the money in a business that the people owe to the owner when they have bought the products or services from him. In contrast, accounts payable is the money a business owner owes to another vendor. For example - Rent

3. Accruals: These are the credits and debits that a business owner has recorded but is waiting for the fulfilment of the same.

4. Assets: Assets can be defined as everything that a business owner owns - it includes both tangible and intangible assets. For example - cash, property, copyrights, tools, trademarks and patents.

5. Burn rate: Burn rate in accounting can be defined as how fast a business owner spends his money. This is considered to be a very critical factor while calculating the cash flow in the business.

6. Capital: It is the amount that a business owner has to invest or spend for his business.

7. Cost of goods sold (COGS): This can be defined as the cost required to produce a product or offer a service to the end customer. It is considered to be the first expense in the profit and loss statement.

8. Depreciation: Depreciation in accounting can be defined as the decrease in the value of the business assets over some time. This value is considered to be important for tax purposes as the value of larger assets can be written off while filing income tax by the business owner.

9. Equity: It can be defined as the amount of money a business owner has invested in his business. This can also be defined as the difference between assets and liabilities. For a business owner, it can include non-monetary things such as energy, time and even other resources.

10. Expenses: Expenses in accounting can be said to be the various purchases a business owner makes to generate revenue. It is also known as the cost of doing business in simple man’s language. The different types of expenses are fixed expenses, variable expenses, accrued expenses, and operating expenses.

11. Fiscal year: A fiscal year can be said to be the period that a company uses for accounting. The start date and end date of the year are dependent on the business owner. It can be the same as the calendar year or can vary as per the business owner/ accountant’s decision.

12. Liabilities: These are the things that a company owes in the short-term or long-term. It includes payroll, loans, taxes and even credit card balance.

13. Profit: In accounting, profit can be defined as the difference between income, COGS and all types of expenses.

14. Revenue: In accounting, revenue is considered to be the total amount of money that a business owner collects for the goods or services he offers to the customers. The company expenses are not included in revenue/

15. Gross margin: A gross margin is calculated by subtracting COGS from the total sales. This figure in accounting denotes the sustainability of business in the market.

How to do Accounting for Small Businesses?

If you are an entrepreneur who has just launched his business and is getting familiar with the various business process through your startup, it is very natural for you to be unaware of the accounting process.

Here are the 8 steps that every business owner must follow to set up his business in a sustainable way in his industry -

1. The business owner must first open a business bank account which is linked to all points of sale. A business owner who has an LLC company, a Corporation, is a sole proprietor or does business in partnership should have a separate bank account. This will help the business owner to keep an accurate record of income and expenses. Moreover, the account must be registered in the name of your business.

2. It would be easy to understand the business expenses if they are itemized by the corresponding department name. This would prove to be of great help to the employer while filing an income tax return and also when completing other tax forms. The different expenses in the business include advertising, marketing, business travel, and installation of internet setups such as Wi-Fi or equipment. The vehicle expenses and office meals are also included in this department. The employees and business owners must keep the copy of receipts, bank statements, tax returns and any forms such as W-2, W-9 or 1099-C properly

3. The employer must adhere to bookkeeping practices for proper business management. In addition to this, he should keep a proper record of the employment and excise taxes declared by the federal government of the US.

4. The business owner must be very clear about hiring - whether he wants full-time employees or wants to have part-time contractors as his workers in the business. He should set up an automated payroll process as it is considered to be the most tedious part of accounting.

5. The business owner must then identify the right payment gateway according to his business needs. It will help him understand how he wants to collect money from the customers in his business.

6. Taxes are an inevitable part of the business and hence, find their mention in accounting. Paying taxes for small businesses could be complicated for the new business owners and hence, it is important to maintain accurate records. The employer can consult a tax professional or take the help of a professional to ensure all the procedures are appropriately followed.

7. The accounting books in your business must be regularly reviewed to evaluate the used methods. It helps the business owner understand if the set accounting processes are properly followed and what changes should be bought in the business to get more profitable income.

8. Hire a professional CPA or accounting professional from the CPA directory if you do not want to do this whole process alone.

Conclusion

Having basic information about accounting and its terms is very important for every business owner. It will give him a better understanding of the output of his business ideas. This would help him know if he wants to continue with the existing methods or think of innovative ideas to expand his business. Deskera People can provide you with tools to manage payroll and leaves.

How can Deskera Help You?

Deskera Books is an online accounting, invoicing, and inventory management software that is designed to make your life easy. A one-stop solution, it caters to all your business needs, from creating invoices and tracking expenses to viewing all your financial documents whenever you need them.

Key Takeaways

1. Accounting can be defined as the systematic procedure to keep records, doing analysis and final interpreting the various financial documents in business. These different documents for accounting basics include income statements, balance sheets, profit and loss statements, cash flow statements and bank reconciliation.

2. A business owner must follow the accounting principles along with the GAAP principles for proper management of the business.

3. An entrepreneur who is just set to enter the market or small business owner should have a basic idea about the various accounting terms as it would prove useful in business.

4. These terms include debit & credit, accounts receivable & accounts payable, accruals, assets, burn rate, capital, COGS, depreciation, equity, expenses, fiscal year, liabilities, profit, revenue, and gross margin.

5. Every business owner must maintain a separate bank account to list the profits and expenses properly while doing accounting.

Related Articles