From this article, we are hoping to see how depreciation functions, so you can amplify your tax benefits. Your accountant or financial specialist will deal with this for you, yet it's imperative to see how it helps. All-inclusive accounting software can facilitate learning about depreciation and its impact on your business and assets over time.

In this article, we learn about:

- Details of the concept of Depreciation

- Why do we need to depreciate assets

- How depreciation can help small businesses

- Tax impact of depreciation

- We shall also learn about the difference between depreciation and amortization

- We shall also look at the kind of entries made for depreciation

What is Depreciation?

Depreciation represents the decrease in the value of an asset due to its continuous deterioration through its useful life. Companies calculate depreciation to estimate how much their assets have decreased in value over time.

Depreciation is carried out for tangible assets which are the physical assets. A company acquires these assets to increase productivity and raise the overall performance of the business. Intangible assets are amortized which is a concept similar to depreciation but the type of assets differ in both cases.

Tangible assets have a physical form whereas intangible assets do not have a physical presence. Some examples of tangible assets are:

- Furniture

- Equipment

- Land

- Machinery

- Vehicles

- computers, and so on.

Across its useful years, an asset is utilized continuously and this causes it to wear out. After the company has utilized the asset for its useful life, the company may decide to sell it off by calculating its salvage value.

All this is done so that the enterprises can accurately calculate the profits and gross revenue at the end of the year.

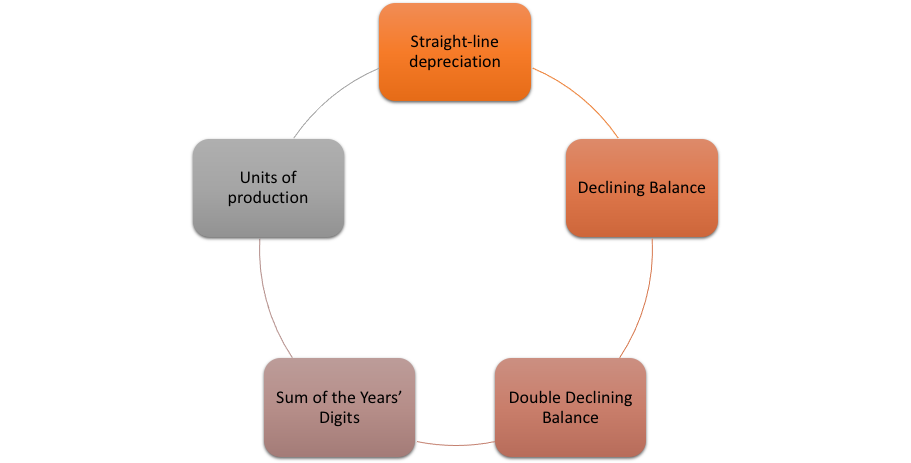

What are the Types of Depreciation with Formula?

In the US, it is mandatory for accountants to calculate depreciation per the rules set by GAAP- Generally Accepted Accounting Principles. These rules take into account all the complications and legitimacy involved in corporate accounting. Based on these rules, here are the primarily applied methods across the sectors.

- Straight-line depreciation

- Declining Balance

- Double Declining Balance

- Sum of the Years’ Digits

- Units of production

Each method carries out the calculation differently. Due to different calculations, the amount of depreciation expense is also different, and therefore, each method affects the company’s taxable earnings and thereby, its tax deductibles.

1. Straight-line Depreciation

Companies tend to use this method more often than any other method. It is a simple technique that considers an even amount as a depreciation expense each year.

The technique also considers the residual or salvage value which is subtracted from the original cost of the asset. The result is divided by the useful life of the asset to obtain the straight-line depreciation.

The straight-line method calculates depreciation through this expression:

2. Declining Balance Method

In this method, the companies calculate depreciation based on the diminishing value of the asset. This method considers a varying value of depreciation each year based on the deterioration of the asset. It is an accelerated method of calculating depreciation that depreciates the assets rapidly.

Here’s the expression for the formula:

3. Double Declining Balance Method

This method has taken from the declining balance method with a difference that this is more rapid in its action. The Double declining method depreciates assets even more aggressively and facilitates creating better profits when the asset is sold.

The companies use this is accelerated method when they expect a greater utility of the asset in the earlier years and much lesser in the later years. Here, the companies consider the accumulated depreciation which is the total of depreciation expenses incurred till that period.

4. Sum of the Year’s Digits Depreciation

The Sum of the years’ digits method segregates annual depreciation into fractions considering the number of years of the usefulness of the asset. The method is more aggressively rapid than the straight-line method but less rapid than the double-declining method.

Like other accelerated methods, the sum of years’ digits is also apt for assets that have a greater production capacity in their earlier years.

Formula:

The method involves several steps for the calculation of depreciation that need to be applied.

5. Unit of Production Method

The next method in line is the Unit of Production method. It considers the productivity of the asset rather than the number of years it was utilized for. Therefore, the method is called the unit-based method, unlike the other methods which are time-based methods.

This method offers greater deductions for depreciation in the time when the machine/ asset was heavily used, offsetting the periods when it will not be much in use.

Here, estimated production capacity is the capacity of the asset to produce units. ‘Units per year’ is the number of units produced by the asset per year.

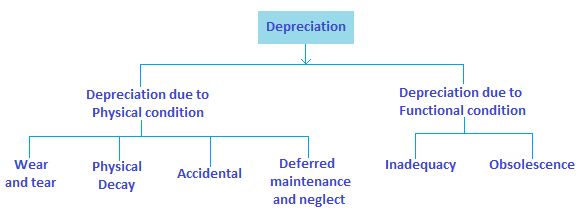

Top Causes of Accounting Depreciation

Companies need to assess the actual consumption of an asset and reduce its value accordingly. This process helps them to gauge the salvage value by the time the asset has been utilized completely.

In this section, we look at the top reasons we need depreciation for.

- Deterioration: After continual use, assets generally wear out to the extent that they may no longer be productive. Here, production equipment is a typical example. Such assets wear out after producing a certain number of units. Such assets need to be replaced. Other assets such as buildings and constructed establishments can be repaired.

- Rights to use: A company may have acquired the right to use a fixed asset for a particular duration. In that case, the useful life of the asset is the duration for which the company has the right to use it. The company must depreciate the asset across this duration to obtain an accurate value of expenses.

- Perishability: Assets with extremely short life need to be depreciated accordingly. The inventory goods are a good example under this category.

- Obsolescence: Becoming outdated is one of the reasons some assets need to get depreciated. Computers and other technological devices serve as examples here.

- Using Natural Resource as Asset: An oil and gas company needs to look at the depletion levels rather than the depreciation, oil being a natural resource. The rate of depletion is considered in such cases as it may change over time based on the reserves left.

Why should Small Businesses Care about Depreciation?

Fundamentally, depreciation refers to decreasing the value of the asset over time. This implies that when you buy an asset like a computer for your business, you can claim a part of the loss in its value as a business expense.

Small businesses can benefit by claiming maximum tax advantage by depreciating assets. Here are some points that help recognize the importance of depreciation for businesses:

- It is important to include the depreciation expense while costing for your products. Physical assets are not perpetual or everlasting. They deteriorate after regular intervals which is a cost to your businesses, and that must be accounted for.

- A point that businesses must keep a note of is that the depreciation starts only when the assets start producing or generate a value. You cannot claim expenses for an asset that is non-productive or one which will start producing after a certain time.

- While calculating depreciation on a monthly basis, you shall be able to claim only for the months the asset was used for. Say, you bought a car 4 months before the financial year ends, then you will be eligible to claim only four months of depreciation for the financial period and not the entire year.

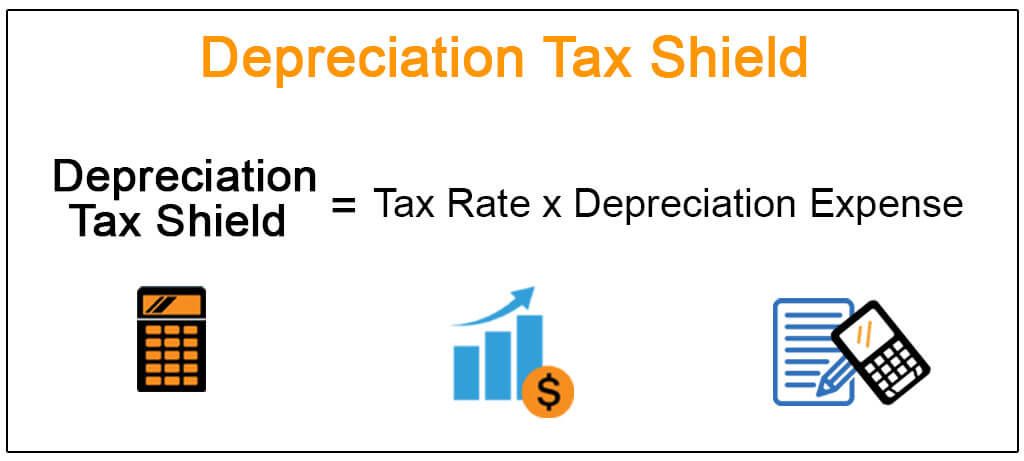

Tax Impact of Depreciation

In accounting, depreciation refers to the method of allocating the cost of tangible assets across their valuable life. When the businesses record a decrease in the value of the asset, there is a simultaneous decrease in the amount of taxes the company pays.

This is to say that the depreciation expenses signal reduced earnings which form the basis of the tax amount. Therefore, depreciation directly reduces the amount going towards tax deductions. The higher the depreciation expense, the lower are the tax deductions and vice versa.

Depreciation Tax Shield is the tax saved resulting from the deduction of depreciation expense from the taxable income. It and can be calculated by multiplying the tax rate with the depreciation expense. Companies using accelerated depreciation methods (higher depreciation in initial years) are able to save more taxes due to higher value of tax shield. However, the straight-line depreciation method, the depreciation shield is lower.

On selling the assets, the accumulated depreciation that appears on the balance sheet is reversed; which eventually removes assets from financial statements.

Depreciation Vs. Amortization

Businesses regularly value their assets. Depreciation and Amortization are two methods that are used in the process. The basic difference between the two is that while depreciation is used to value tangible assets, amortization is used for intangible assets.

Intangible assets include the following:

- Patents

- Copyrights

- Trademarks

- Goodwill of a company

Another point of difference is that amortization uses the straight-line method to record expenses. Plus, the assets that are amortized do not have a salvage value as is in the case of the depreciated assets.

How are Depreciation and Accumulated Depreciation Different?

We know by now that the accumulated depreciation is the cumulative depreciation of an asset up to a certain time in the useful life.

Besides this, let’s learn about the other points from the table below:

Recording Depreciation

When a company purchases an asset, it records the asset as a debit to show an increase in the asset account on the balance sheet. Along with this, the company also records it as a credit to reduce cash, which also makes an appearance on the balance sheet. This way, the income statement does not get affected by either of the journal entries.

So, to show the cost of the asset on the income statement, the companies consider depreciating assets regularly.

To understand this better, let’s consider a simple example:

A company buys a van for internal use worth $ 40,000 at the start of 2015. It estimates the useful life of the van to be 5 years. Now, the company distributes $40,000 over the 5 years of the van’s useful life. So, assuming zero salvage value, the depreciation expense is $8,000 every year.

Calculating depreciation through the Straight-line method:

The company records depreciation as follows:

Depreciation expense is presented on the income statement. From the above table, $8,000 is the depreciation measured each for the years 2016, 2017, 2018, 2019, and 2020.

Accumulated depreciation is the cumulative depreciation across the 5 years. Therefore, the accumulated depreciation at the end of 2016 will be $8,000, at the end of 2017 will be 16,000, by 2018 is $24,000. Likewise, by the end of 2020, the accumulated depreciation is $40,000.

We notice that the carrying value becomes equivalent to the residual value at the end of the asset’s useful life, zero in this case.

How can Deskera help your Accounting and Business?

As a business owner, you can invest in accounting softwares that can help you keep track of your journal entries, balance sheet, inventory and production costs.A successful business needs an efficient financing process that meets its specific needs.

Deskera Books is an online accounting software that your business can use to automate the process of journal entry creation and save time. The double-entry record will be auto-populated for each sale and purchase business transaction in debit and credit terms. Deskera has the transaction data consolidate into each ledger account. Their values will automatically flow to respective financial reports.

You can have access to Deskera's ready-made Profit and Loss Statement, Balance Sheet, and other financial reports in an instant.

Deskera can also help with your inventory management, customer relationship management, HR, attendance and payroll management software. Deskera can help you generate payroll and payslips in minutes with Deskera People. Your employees can view their payslips, apply for time off, and file their claims and expenses online.

With Deksera CRM you can manage contact and deal management, sales pipelines, email campaigns, customer support, etc. You can manage both sales and support from one single platform. You can generate leads for your business by creating email campaigns and view performance with detailed analytics on open rates and click-through rates (CTR).

Deskera is an all-in-one software that can overall help with your business to bring in more leads, manage customers and generate more revenue.

Key Takeaways

We shall take a quick recap of the article here:

- Depreciation is a record of the decrease in the value of the assets over time.

- The GAAP sets the rules for recording depreciation made by companies.

- There are five key methods the companies use to record depreciation: Straight-line, Declining Balance, Double Declining Balance, Unit of production, and sum of the Years’ Digits.

- Deterioration, obsolescence, and perishability are some of the reasons for calculating depreciation.

- Depreciation helps companies estimate the true values of the assets and therefore, help assess earnings and tax deductibles.

- A higher depreciation amount implies lesser earnings and thereby, leading to lower tax deductibles.

- Accumulated depreciation is the sum of all the depreciation expenses till a specific date.

- Amortization is another method to decrease the value of assets but it is applicable only for intangible assets.

Related Links