According to the tax foundation, in 2022, the top individual federal income tax rate is projected to be 38.5%, while the corporate federal income tax rate is projected to be 22.5%.

Federal income tax liability is the amount of money that an individual or a business is legally obligated to pay to the federal government in taxes. This amount is determined by applying the relevant tax rates to the individual's or business's taxable income. The amount of federal income tax liability must be paid either in full or in installments throughout the year.

This highlights the importance of paying your federal income tax liabilities on a timely basis to avoid being penalized or punished due to its failure. Additionally, paying them on time will put you on the right side of the law.

Thus, understanding your federal income tax liabilities is a must.

Taxation and Tax Liabilities

For an individual or a business, the tax liability is calculated based on the current tax laws. This involves multiplying the tax base by the tax rate.

One thing to keep in mind is that the income that is subjected to federal income tax includes earnings, gains on sales of a home or other asset, and other taxable events. Also this income may also be subjected to state as well as local taxes.

Finally, the amount of tax liability that you calculate is reduced by items such as credits, deductions, and estimated tax payments, made to reach your total tax liability.

However, what you must note here is that if your tax liability is unpaid, then you will accrue fees, charges, and interest over time.

What are Federal Income Tax Liabilities?

Federal income tax is a tax imposed by the United States federal government on the income of individuals, corporations, trusts, and other legal entities. Income tax is calculated based on taxable income, which is adjusted gross income plus certain deductions and exemptions.

Taxpayers are required to file a federal income tax return each year to report their income, deductions, exemptions, and other pertinent information. Tax liability is the amount of money an individual or business owes in taxes to the federal government.

Tax liability is determined by subtracting any credits or deductions from the taxpayer’s total taxable income. Taxpayers can reduce their tax liability by taking advantage of deductions, credits, and other available tax breaks.

Taxpayers with a higher income may be subject to higher tax brackets and owe more in taxes. Taxpayers can also lower their federal income tax liabilities by contributing to retirement accounts, such as a 401(k), IRA, or other tax-advantaged plans.

Additionally, taxpayers may be able to offset some of their federal income tax liability by claiming certain credits, such as the Earned Income Tax Credit or the Child Tax Credit. Taxpayers may also be able to reduce their tax liability by making charitable donations.

In fact, taxpayers may be able to reduce their tax liability by taking advantage of tax-deferred investments. Taxpayers may be able to reduce their federal income tax liability by taking advantage of tax-free investments, such as municipal bonds.

Also taxpayers may also be able to reduce their tax liability by taking advantage of tax-exempt investments, such as certain mutual funds. Taxpayers may be able to reduce their tax liability by taking advantage of other strategies, such as timing their investments or taking advantage of tax-loss harvesting.

Lastly, taxpayers may be able to reduce their federal income tax liability by consulting with a qualified tax professional.

What are the Components of Federal Income Tax Liabilities?

Before you can calculate your federal tax liabilities (i.e., the amount that you owe as a taxpayer after all the deductions and credits are applied), some of the information that you must know are:

- Gross Income: This is the total income earned from all sources before deductions and exemptions.

- Deductions: These are the allowable deductions that reduce a taxpayer's taxable income.

- Exemptions: These are the amounts that are exempt from taxation, such as personal exemptions, dependents, and certain credits.

- Taxable Income: This is the amount left after deductions and exemptions are taken into account.

- Tax Brackets: Tax brackets are the various income levels at which different tax rates are applied.

- Tax Rate: This is the rate at which taxes are applied to taxable income.

- Tax Credits: These are the amounts that reduce the amount of taxes owed.

Thus, the four main components of federal income tax liabilities are:

Principal Tax

This is the base amount on which your interest will be calculated. This amount comes from original and substitute balances, along with additional assessments.

- The number shown in the balance due section of a prepared tax return is the original balance.

- The liability amount determined by an IRS-prepared return, using either third-party information or past taxpayer information, is a substitute balance.

- Lastly, there are additional tax assessments, such as balances derived from audits or error corrections.

Penalties

These are the fees that you are charged for failing to pay and file your taxes in accordance with IRS regulations. Typically, penalties are a percentage of the total owed. Thus, if your balance is zero, then you may not be penalized.

However, there are some types of businesses that will be subjected to a late-payment penalty even if they do not owe taxes. Some of the most common types of penalties are:

- Late payment

- Underpayment

- Failure to file

Interest

Additionally, the IRS will also assess interest as a fee on your past-due balance, even if you are enrolled in a payment plan. What you must take note of here is that the interest is calculated not only on the principal tax but also on accrued penalties and interest.

Other Components

Other components of federal tax liability may include self-employment tax, household employment taxes, and penalties such as those for lack of health insurance coverage or the IRA early distribution penalty.

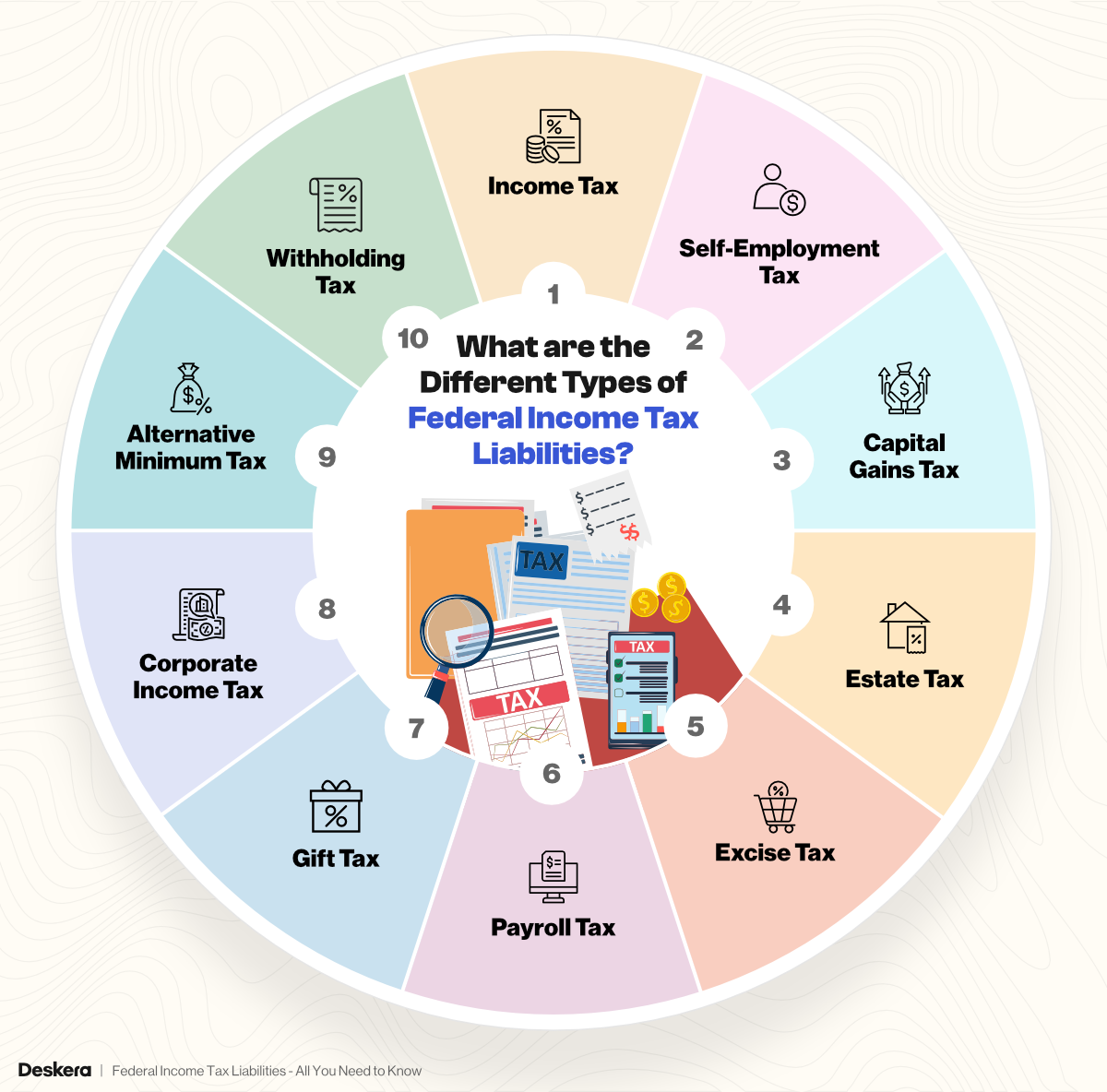

What are the Different Types of Federal Income Tax Liabilities?

Considering that federal income tax liability is any amount that you owe to the federal taxing authority, the different types of federal income tax liabilities are:

Income Tax

This is a liability imposed by the federal government on individuals or businesses that have earned income. It is based on a person's or entity's taxable income and is typically paid annually. To know your federal income tax liability, you should check the income tax bracket that is applicable to you.

Self-Employment Tax

This is a tax imposed on those who are self-employed or have wages from certain businesses. It is calculated as a percentage of net earnings from self-employment.

Capital Gains Tax

This is a tax imposed on the profit from the sale of certain assets. This includes stocks, bonds, real estate, and other investments. For example, if you purchase property for $100,000 and sell it for $150,000, then the capital gains tax will be assessed on the $50,000 profit.

However, what you must keep in mind is that your capital gains tax rate will vary and, in fact, may even be different than the income tax rate applicable to you. Also, long-term gains are taxed at special capital gains rates of 0%, 15%, and 20%, depending on your income (with some rare exceptions).

Note: If you owned an asset for one year or less, then profit from the sale of the same will be considered as short-term gain and would be added to your tax liability as ordinary income and taxed according to your tax bracket.

Estate Tax

This is a tax imposed on the transfer of property from a deceased person to their heirs. It is based on the value of the estate and is paid by the executor of the estate.

Excise Tax

Excise tax is a tax imposed on certain goods and services. It is typically a flat tax and is imposed on items such as alcohol, cigarettes, and gasoline.

Payroll Tax

Payroll tax is a tax imposed on employers and employees to fund programs such as Social Security and Medicare. It is typically withheld from an employee's wages or salary and paid to the government by the employer.

Gift Tax

This is a tax imposed on gifts given by an individual or entity to another. It is based on the value of the gift and is typically paid for by the donor.

Corporate Income Tax

This is a tax imposed on corporations based on their net profits. It is typically paid annually to the federal government.

Alternative Minimum Tax

This is a tax imposed on individuals and entities with high incomes. It is designed to ensure that those with higher incomes pay their fair share of taxes.

Withholding Tax

This is a tax imposed on wages, salaries, and other income. It is typically withheld from an employee's wages or salary and paid to the government by the employer.

How can You Reduce Your Federal Income Tax Liabilities?

One of the key ways to reduce your federal income tax liabilities is by undertaking careful planning. This involves making sure that you are claiming all the deductions for which you qualify. In fact, you can also file a new W-4 with your employer to adjust your payroll tax exemption.

Thus, 15 strategies that you can implement to reduce your federal income tax liabilities are:

Contribute to a Retirement Account

Contributing to a retirement account, such as a 401(k) or IRA, reduces your taxable income as these contributions are made pre-tax.

Take Advantage of Tax Deductions

Tax deductions reduce your taxable income by the amount of the deduction, resulting in a lower tax liability.

Claim Tax Credits

Tax credits reduce the amount of tax you owe dollar-for-dollar rather than reducing your taxable income.

Use a Flexible Spending Account

Contributions to a flexible spending account reduce your taxable income, as these funds are taken out of your paycheck before taxes.

Invest in Tax-Advantaged Accounts

Investing in accounts such as a Health Savings Account (HSA) or 529 plan can reduce your taxable income.

Give to Charity

Charitable donations are deductible, reducing your taxable income and resulting in a lower tax bill.

Take the Home Office Deduction

If you use your home for business and meet certain criteria, you can take a home office deduction and reduce your taxable income.

Bunch Itemized Deductions

Bunching itemized deductions into one year instead of spreading them out can help you to exceed the standard deduction, resulting in a lower taxable income.

Take the Saver’s Credit

Low- and moderate-income taxpayers can take the saver’s credit for contributions to a retirement plan, reducing their taxable income.

Utilize the Child and Dependent Care Tax Credit

If you pay for childcare or dependent care, you may be able to take the child and dependent care tax credit, which reduces your taxable income.

Claim the Lifetime Learning Credit

The lifetime learning credit is available for tuition and other educational expenses, reducing your taxable income.

Take the Earned Income Tax Credit

Low-income taxpayers may qualify for the earned income tax credit, which reduces their tax liability.

Utilize the American Opportunity Tax Credit

The American opportunity tax credit is available for higher education expenses, reducing your taxable income.

Postpone Income

Postponing income to the next year can help you to reduce your taxable income in a given year.

Sell Losing Investments

If you sell investments for a loss, you can use that loss to offset gains and reduce your taxable income.

Deferred Tax Liabilities

You might be one among those several types of businesses that are affected by deferred tax liability. Deferred tax liability occurs because of the discrepancy between IRS and financial accounting rules.

One of the most common types of deferred tax liability is five-year business asset depreciation. The IRS treats depreciation differently than the accounting profession does.

Thus, in such situations, you will have to subtract the tax expense using the financial accounting method by tax payable according to the IRS accounting method. This will help you find either deferred tax liability or deferred tax asset.

How to Calculate Your Federal Income Tax Liabilities?

Some of the steps that you will need to undertake to calculate your federal income tax liabilities are:

Determine Your Filing Status

Before you can determine your federal income tax liabilities, you must first determine your filing status. Your filing status will determine which tax rate and deductions you are eligible for.

The most common filing statuses are single, married filing jointly, married filing separately, head of household, and qualifying widow/widower with dependent child.

Determine Your Income

Next, you will need to determine your income. This includes all income you received during the tax year. This could include wages, salaries, tips, bonuses, and self-employment income. You must also include any income from investments, such as interest or dividends.

Calculate Your Adjusted Gross Income

After determining your income, you must calculate your adjusted gross income (AGI). Your AGI is your total income minus certain deductions, such as student loan interest, IRA contributions, and alimony payments.

Calculate Your Taxable Income

Once you have calculated your AGI, you can calculate your taxable income. Your taxable income is your AGI minus any deductions and credits you are eligible for. These deductions and credits can significantly reduce your taxable income, meaning you will owe fewer taxes.

Calculate Your Tax Liability

Once you have calculated your taxable income, you can calculate your federal income tax liability. To do this, you will need to look up the tax rate for your filing status and income level in the Internal Revenue Service (IRS) tax tables. The tax tables are published each year and are available online.

Calculate Your Tax Payments

Finally, you will need to calculate your tax payments. To do this, you will need to take into account any taxes you have already paid, such as through payroll deductions or estimated tax payments. You may also be eligible for certain tax credits, such as the Earned Income Tax Credit or the Child Tax Credit, which can reduce your tax liability.

File Your Tax Return

Once you have calculated your federal income tax liabilities, you can then prepare and file your tax return. This will allow the IRS to verify your tax information and determine if you owe any additional taxes or are due a refund. If the taxes are not paid in full by the deadline, penalties and interest may be assessed on balance due.

FAQs Related to Federal Income Tax Liabilities

- What is a federal income tax?

A federal income tax is a tax imposed by the United States federal government and collected from individuals and businesses to fund the government’s operations.

- How much do I have to pay in federal income taxes?

The amount of federal income taxes you owe depends on your income, filing status, and other factors. You can use the Internal Revenue Service’s (IRS) Tax Withholding Estimator to estimate the amount of taxes you will owe.

- When is the federal income tax filing deadline?

The federal income tax filing deadline is generally April 15th of each year.

- What forms do I need to file my federal income taxes?

The IRS provides a list of the forms you may need to file. Generally, most individuals will need to file Form 1040 and the applicable schedules.

- What are the penalties for not filing or paying my federal income taxes?

Failure to file and/or pay your federal income taxes can result in penalties, interest, and other collection actions, such as liens or levies.

- Do I have to pay taxes on my Social Security benefits?

It depends on your income. Social Security benefits can be taxable if your combined income is greater than certain thresholds.

- What is the difference between federal and state income taxes?

Federal income taxes are imposed by the federal government, while state income taxes are imposed by the state in which you live.

- How can I get help with filing my federal income taxes?

The IRS has a variety of resources available to help you understand and file your federal income taxes. You can also seek assistance from a tax professional.

- Can I file my federal income taxes electronically?

Yes, you can file your federal income taxes electronically using the IRS e-file system.

- When do I need to make estimated tax payments?

If you owe taxes that exceed a certain threshold, you may be required to make estimated tax payments throughout the year. You can use the IRS Tax Withholding Estimator to determine your estimated tax liability.

How can Deskera Help You Calculate Your Federal Income Tax Liabilities?

Deskera Books is an online accounting system that will automate several of your accounting tasks, including calculation, payment, and reporting of taxes. Thus, accounting and filing not only becomes a lot easier but also more efficient, thereby saving you from penalties.

Deskera Books will not only keep all your financial records, statements, data, and reports in one place, but it will also let you give access to your account to your accountant or tax professional by sending them an invite link.

In fact, Deskera Books comes with pre-configured tax codes, charts of accounts, and even accounting rules as needed to be followed in the USA. This will thus ensure that you are accurately calculating your federal income tax liabilities. It will also help you in fulfilling all the required forms and adhere to the deadline for it all.

Lastly, through the dashboard of Deskera Books, you will be able to monitor your financial analytics.

Key Takeaways

Federal income tax liability is the amount of money that an individual or a business is legally obligated to pay to the federal government in taxes.

This amount is determined by applying the relevant tax rates to the individual's or business's taxable income. The amount of federal income tax liability must be paid either in full or in installments throughout the year.

The four main components of federal income tax liabilities are:

- Principal tax

- Penalties

- Interest

- Other components like self-employment tax, household employment taxes

Also, before calculating your federal income tax liabilities, some of the information you must know are:

- Gross income

- Deductions

- Exemptions

- Taxable income

- Tax brackets

- Tax rate

- Tax credits

The different types of federal income tax liabilities are:

- Income tax

- Self-employment tax

- Capital gains tax

- Estate tax

- Excise tax

- Payroll tax

- Gift tax

- Corporate income tax

- Alternative minimum tax

- Withholding tax

Some of the strategies that you can implement to reduce your federal income tax liabilities are:

- Contribute to a Retirement Account

- Take Advantage of Tax Deductions

- Claim Tax Credits

- Use a Flexible Spending Account

- Invest in Tax-Advantaged Accounts

- Give to Charity

- Take the Home Office Deduction

- Bunch Itemized Deductions

- Take the Saver’s Credit

- Utilize the Child and Dependent Care Tax Credit

- Claim the Lifetime Learning Credit

- Take the Earned Income Tax Credit

- Utilize the American Opportunity Tax Credit

- Postpone Income

- Sell Losing Investments

Implementing accounting software like Deskera MRP will automate several of your tasks while also ensuring accurate tax calculations and filings.

Related Articles