As an employer, you certainly want to know about the best health plans to offer to your employees. You tumble through a lot of HRA plans and then you get to hear about the QSEHRA or the Qualifies Small Employee Health Reimbursement Arrangement.

If you are the owner of a small business that comprises of up to 50 permanent employees, then QSEHRA could just be the right health reimbursement plan you are looking to offer.

Here, we see through the entire process of conveniently setting up QSEHRA for a small business. We will be driving through the following points as well:

- What is a Qualified Small Employer HRA QSEHRA?

- Steps to Set Up a QSEHRA

What is a Qualified Small Employer HRA QSEHRA?

A QSEHRA or Qualified Small Employer Health Reimbursement Arrangement, or small business HRAs provide subsidies for health insurance for employees who work at businesses with fewer than 50 full-time employees. For employees, reimbursement is tax-free. For employers, reimbursement is tax-deductible.

QSEHRA plans are also utilized to cover uncovered medical costs or offset health insurance coverage.

Steps to Set Up a QSEHRA

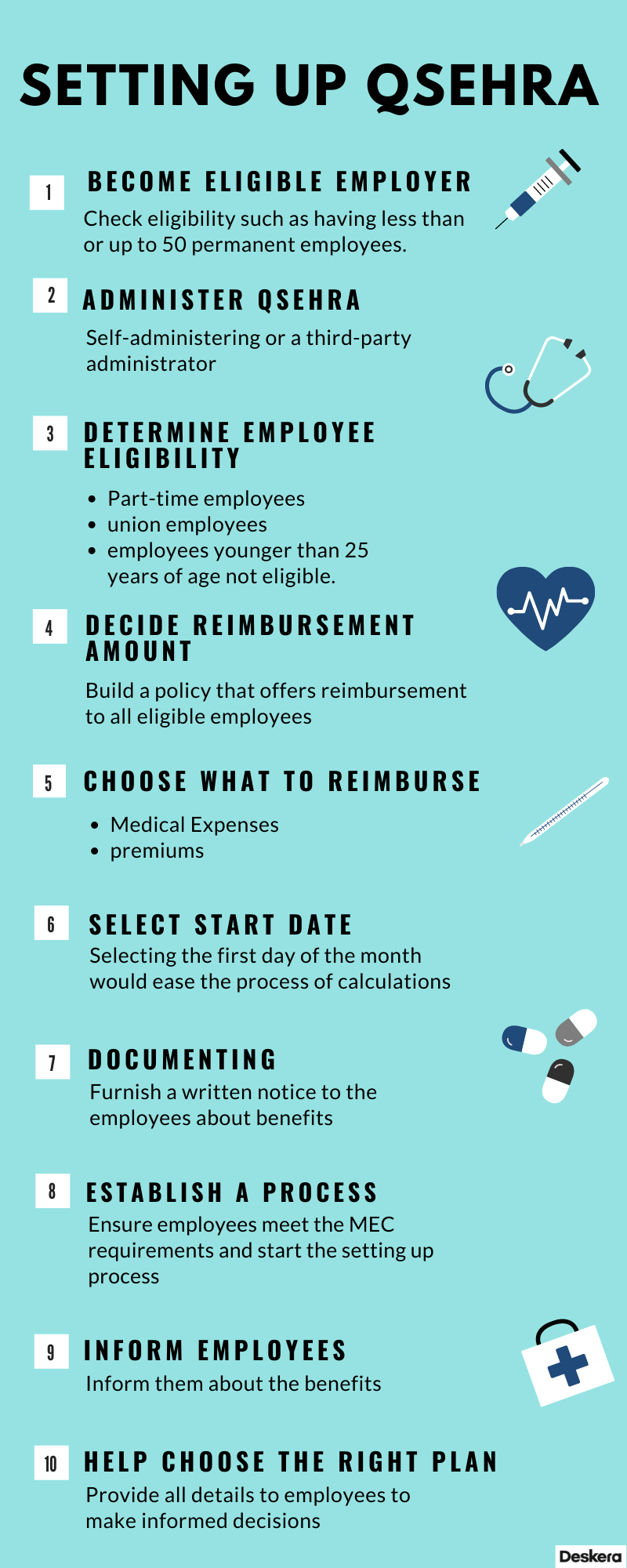

This section depicts the steps you can follow to set up a QSEHRA for your employees.

STEP 1: Become an Eligible Employer

As an employer, you can offer QSEHRA only when you fulfill the following criteria:

- You have only up to 50 employees in the previous year

- You do not offer any group health plans that comprise of HRAs (Health Reimbursement Arrangements), FSAs (Flexible Spending Arrangements), any vision and dental plans

- You offer an HSA or Health Savings Account QSEHRA only if employees are enrolled in an HDHP, i.e., Highly Deductible Health Plan, which is a requirement for HSA

- You can provide QSEHRA and HSA together; only QSEHRA reimburses or covers only premiums

- You can also offer HSA with QSEHRA only when the QSEHRA reimburses premiums and not the medical expenses

STEP 2: Administer Your QSEHRA the way you want

You are free to determine how you want to administer your QSEHRAs. Self-administering or a third-party administrator, you have both options available.

- When you choose a third-party admin, they will offer you a lot of combinations and configurations. There could be specific restrictions, too, including the eligibility and types of reimbursements. Before moving ahead, you must ensure having understood the plan in its entirety

- Whether self-administered or not, you must be mindful that it would be you, as an employer who would make the reimbursements to the employees under the plan

STEP3: Determine Employee Eligibility for QSEHRA

As an employer, when you decide to provide QSEHRA to your employees, you will have to provide it for all your permanent employees except the ones mentioned here:

- Employees who are under 25 years of age at the start of the plan

- Part-time employees

- Union employees

- Employees who haven’t worked for over 90 days in your organization

- Individuals who don't receive income from U.S. sources

Having mentioned that, it is interesting to note that if you can decide to offer QSEHRA to a particular part-time employee, then you must present it to all the part-time employees working for you.

Important Note: Ensure that all your employees (along with family members) who want to participate in QSEHRA have their own health insurance policies that meet the MEC requirements- Minimum Essential Coverage requirements.

On that note, employees must also learn about the affordability of the QSEHRA the employer is offering. Referring to the HealthCare.gov worksheet would cater more clarity while estimating the affordability of the QSEHRA.

STEP 4: Decide the Reimbursement Amount for Each Employee

With no restriction on the minimum amounts for contribution or participation, QSEHRA lets you have complete control over your expenses. Although, the maximum limits are set ad changed by the IRS every year.

Here are the rules you would need to remember when you are setting your reimbursement amounts:

- You must build a policy that offers reimbursement to all eligible employees alike

- Additionally, you will have to make QSEHRA benefits available to all eligible candidates. Plan your QSEHRA budget, including those costs

- The employer may choose to roll over the unused reimbursement amount from an earlier plan year if an employer's QSEHRA allows that to happen, but the total reimbursement for the employee cannot exceed the maximum limits set by the IRS for the new plan year

- Each employee can be reimbursed the same amount or the IRS maximum; you can, however, adjust the reimbursement amount for family size and employee age. Some options for varying reimbursement amounts are as follows:

- Calculate your maximums based on the premium amounts of a baseline policy with MEC

- Calculate the percentage of IRS limits. This means you can provide, say, 50% coverage of the IRS maximum to the employees and about the same (50%) IRS limit for the employees’ families

- Based on a one-third ratio, distinguish contributions between the ages. For example, setting a reimbursement rate of $45 for the employees of age 25, whereas the reimbursement rate for the employees at 60 could be $150. So, the employees between 25 and 60 years of age could receive a uniform amount

STEP 5: Choose the Expenses You want to Reimburse

Being an employer, you enjoy the authority to select the health care expenses of an employee for reimbursing. However, they should be within the legal boundaries.

You can choose to reimburse either only the medical expenses or the premiums. When you reimburse only the premiums, you will be able to get more clarity on the overall expenses as the premium amounts are the same across the months. Of course, changing the plans will affect it, but that happens occasionally.

Furthermore, you will also be able to provide an HSA with the QSEHRA to the employees that have HDHPs; however, reimbursing medical expenses through QSEHRA would not be possible.

When you choose to reimburse the employees’ medical expenses, you will be taking into account the maximum allowable limit. It is important to remember here that you will not be able to offer HSA with the QSEHRA in this option.

Follow the IRS-permitted medical expenses for guidance on what expenses you can reimburse.

STEP 6: Selecting a Start Date

You can choose to start a QSEHRA plan as soon as you decide to provide it to your employees. Yet, selecting the first day of the month would ease the process of calculations later on.

You will need to prorate the contribution limit if your QSEHRA is available for less than 12 months.

When you cancel a group health insurance plan for providing the QSEHRA, the QSEHRA will begin with the new year. Hence, your employees will be able to enroll in individual health insurance coverage. By canceling the QSEHRA at another time of the year, your employees will have to enroll in an individual health insurance plan through the Health Insurance Marketplace at that time.

STEP 7: Documenting Important Information

Having decided upon a starting date and after collecting all the other pertinent data, now it is time to put it together in a legally documented format. Prepare documents and furnish a written notice to the employees comprising the following:

- The number of benefits that may be received

- Information about the employees purchasing health insurance through the individual marketplace, applying for advance PTC payment, should make sure that their health insurance exchange is aware of their QSEHRA benefit amount

- A note that the employees who do not maintain their MEC health insurance may have their reimbursements taxed

- A plan document is also required, which outlines how the QSEHRA is managed.

- Information about how they will receive the reimbursements.

If you find putting together this information tedious, you can hire a third party to draft the legal documents for you.

STEP 8: Establish a Process for Running your QSEHRA

Once you have ensured that your employees meet the MEC requirements, you now need to set up a process to run the QSEHRA. Under the process, your employees will have to furnish documents that support their expenses and act as proof for the eligibility of the reimbursement.

STEP 9: Inform Employees about the new Benefit

After setting up and finalizing all the steps mentioned up to this point, you will not be letting your staff know about the benefits they shall receive from QSEHRA. At least 90 days before you want the QSEHRA plan year to roll out, complete all the documentation processes.

All this documented information (observed in Step 7 above) must be passed on to the employees so that they can become eligible. The employers may face a penalty of $50 per employee (and a maximum of $2500 for the year) if they do not provide the notice to the employees in time.

STEP 10: Help Employees Choose the Right Plan

While you have done your bit and have completed the processes at your end, it is also essential to inform your employees about QSEHRA and the benefits that it holds. Although you cannot dictate to them what plans they must choose, you can always inform them about the various aspects that can help them make the right decisions.

Conclusion

As a gist of the article, we can say that you can provide a QSEHRA if you are not a large employer, and do not offer group health plans to your employees. When you provide QSEHRA, you cannot offer any other health insurance plan to your employees.

How can Deskera Help You?

Deskera People is an all-in-one software that lets you manage payroll, leave, attendance, and other expenses. Generating pay slips for your employees is now easy as the platform also digitizes and automates HR processes.

Key Takeaways

Here is a quick glimpse of the important points from the article:

- A QSEHRA or Qualified Small Employer Health Reimbursement Arrangement, or small business HRAs provide subsidies for health insurance for employees who work at businesses with fewer than 50 full-time employees (or small businesses)

- There are 10 easy steps that will help you set up QSEHRA in your organization

- Ensuring your eligibility as an employer is the first step. You have only up to 50 employees in the previous year and you do not offer any group health plans that comprise of HRAs are some of the parameters to gauge the eligibility

- You are free to determine how you want to administer your QSEHRAs. Self-administering or a third-party administrator, you have both options available

- Next is determining the employees’ eligibility. Part-time employees, union employees, employees under the age of 25 are all ineligible for QSEHRA

- Determining the amount for reimbursement and building your policy around it is the next step

- You can choose to reimburse either the medical expenses or the premiums

- Select a starting date for your plan. Opting to start at the onset of the month proves be useful for calculation later

- Document all your important information and notify your employees such as benefits they shall receive from the plan

- Establish your process to run QSEHRA on the basis of the information collected so far

- As you cannot choose plans for your employees, you can comprehensively inform them to make the decision

Related Articles