Have you ever wondered why two products made from the same materials and labor can still have vastly different production costs? The answer often lies in manufacturing overhead (MOH)—the indirect costs required to keep a manufacturing facility running. While these expenses may not be directly tied to a specific product, they significantly influence production costs, profitability, and overall business performance.

Manufacturing overhead includes a wide range of indirect expenses such as factory rent, utilities, equipment depreciation, maintenance, quality control, and indirect labor. Although these costs are essential for supporting production activities, they can be difficult to track and allocate accurately. Without proper management, overhead expenses can increase operating costs, distort product pricing, and reduce profit margins.

Calculating manufacturing overhead correctly is critical for determining the true cost of production and making informed business decisions. By understanding the different types of overhead costs and using appropriate allocation methods, manufacturers can improve budgeting, optimize resource utilization, and identify opportunities for cost reduction. Effective overhead management also enables businesses to enhance operational efficiency and maintain a competitive edge in increasingly demanding markets.

Modern manufacturing software such as Deskera MRP helps businesses gain better control over manufacturing overhead through real-time cost tracking, production monitoring, inventory management, and detailed reporting. By providing greater visibility into production expenses and resource utilization, Deskera MRP enables manufacturers to identify inefficiencies, reduce unnecessary costs, and make data-driven decisions. In this guide, we will explore manufacturing overhead, its types, calculation methods, and practical strategies to reduce costs and improve profitability.

What Is Manufacturing Overhead (MOH)?

Manufacturing Overhead (MOH) refers to all the indirect costs incurred during the production process that cannot be directly traced to a specific product. These costs are necessary to keep a manufacturing facility operating but are not classified as direct materials or direct labor.

In other words, manufacturing overhead includes the expenses that support production activities behind the scenes. While these costs do not become part of the finished product, they play a crucial role in ensuring that manufacturing operations run efficiently and consistently.

For example, when a company manufactures furniture, the wood used to make a table is a direct material cost, and the wages paid to workers assembling the table are direct labor costs. However, expenses such as factory rent, electricity, equipment depreciation, maintenance, and the salaries of production supervisors are considered manufacturing overhead because they support the production process without being directly attributable to a single product.

Manufacturing overhead is an essential component of total manufacturing costs and must be allocated to products to determine their true production cost. Accurate overhead tracking helps manufacturers set appropriate pricing, improve profitability, create realistic budgets, and identify opportunities to reduce operating expenses.

Some common examples of manufacturing overhead include:

- Factory rent or lease payments

- Utilities such as electricity, water, and gas

- Equipment depreciation

- Machine maintenance and repairs

- Indirect labor (supervisors, quality inspectors, maintenance staff)

- Indirect materials (lubricants, cleaning supplies, safety equipment)

- Factory insurance

- Quality control and inspection costs

- Safety and compliance expenses

By understanding and managing manufacturing overhead effectively, businesses can gain better visibility into production costs, improve cost control, and make more informed operational and financial decisions.

Types of Manufacturing Overhead Costs

Manufacturing overhead costs are generally categorized into three main types: fixed overhead, variable overhead, and semi-variable (mixed) overhead.

Understanding these categories helps manufacturers track expenses more accurately, allocate costs effectively, and identify opportunities for cost optimization.

Fixed Manufacturing Overhead

Fixed manufacturing overhead consists of costs that remain relatively constant regardless of production volume. Whether a factory produces 100 units or 10,000 units, these expenses typically do not change within a specific period.

Examples of fixed manufacturing overhead include:

- Factory rent or lease payments

- Property taxes

- Factory insurance premiums

- Depreciation of manufacturing equipment

- Salaries of production managers and supervisors

Since these costs remain stable, manufacturers must spread them across the units produced to determine the overhead cost per product.

Variable Manufacturing Overhead

Variable manufacturing overhead changes in proportion to production activity. As production increases, these costs tend to rise; when production decreases, they generally decline.

Examples of variable manufacturing overhead include:

- Indirect materials such as lubricants and cleaning supplies

- Utility costs related to machine operation

- Equipment maintenance linked to usage

- Production consumables

- Waste disposal costs associated with manufacturing activities

Managing variable overhead effectively can help manufacturers reduce unnecessary expenses and improve operational efficiency.

Semi-Variable (Mixed) Manufacturing Overhead

Semi-variable overhead contains both fixed and variable components. A portion of the cost remains constant, while the remaining amount fluctuates based on production levels or equipment usage.

Examples of semi-variable manufacturing overhead include:

- Utility bills with a fixed service charge and usage-based fees

- Maintenance contracts with fixed monthly payments plus repair costs

- Equipment servicing expenses

- Telephone and internet services used in production facilities

- Machine lease agreements with usage-based charges

Because mixed costs have both fixed and variable elements, manufacturers often analyze them separately to improve budgeting and forecasting accuracy.

Why Understanding Overhead Types Matters

Classifying manufacturing overhead into fixed, variable, and semi-variable categories helps businesses:

- Improve product costing accuracy

- Create more reliable budgets and forecasts

- Identify cost-saving opportunities

- Optimize resource allocation

- Make informed pricing decisions

- Improve profitability and operational performance

A clear understanding of these overhead categories enables manufacturers to manage production costs more effectively and maintain better control over their overall manufacturing expenses.

How to Calculate Manufacturing Overhead

Calculating manufacturing overhead helps businesses determine the total indirect costs associated with production. Accurate overhead calculations provide a clearer picture of product costs, support pricing decisions, and help identify opportunities to improve profitability.

Step 1: Identify All Indirect Manufacturing Costs

Start by listing all costs that support production but cannot be directly traced to a specific product.

Common manufacturing overhead costs include:

- Factory rent or lease

- Utilities (electricity, water, gas)

- Equipment depreciation

- Factory insurance

- Maintenance and repairs

- Indirect labor (supervisors, maintenance staff, quality inspectors)

- Indirect materials (lubricants, cleaning supplies, safety equipment)

Step 2: Calculate Total Manufacturing Overhead

Add together all indirect manufacturing expenses incurred during a specific period.

Manufacturing Overhead Formula

Manufacturing Overhead = Total Indirect Manufacturing Costs

Or

Manufacturing Overhead = Indirect Labor + Indirect Materials + Other Factory Overhead Costs

Step 3: Select an Allocation Base

Since overhead costs cannot be directly assigned to individual products, manufacturers use an allocation base to distribute these costs across production.

Common Allocation Bases

Direct Labor Hours

- Overhead is allocated based on the number of labor hours used in production.

Direct Labor Cost

- Overhead is allocated according to total direct labor expenses.

Machine Hours

- Overhead is assigned based on machine usage time.

- Common in highly automated manufacturing environments.

Units Produced

- Overhead is distributed equally across all units produced.

Step 4: Calculate the Manufacturing Overhead Rate

The manufacturing overhead rate determines how much overhead should be allocated to production based on the chosen allocation base.

Manufacturing Overhead Rate Formula

Manufacturing Overhead Rate = Total Manufacturing Overhead ÷ Total Allocation Base

Example of Manufacturing Overhead Calculation

Suppose a manufacturer incurs the following monthly overhead expenses:

- Factory rent: $8,000

- Utilities: $3,000

- Equipment depreciation: $4,000

- Indirect labor: $5,000

Total Manufacturing Overhead

Total Manufacturing Overhead = $8,000 + $3,000 + $4,000 + $5,000

Total Manufacturing Overhead = $20,000

Assume the company uses machine hours as its allocation base and records 4,000 machine hours during the month.

Manufacturing Overhead Rate

Manufacturing Overhead Rate = $20,000 ÷ 4,000 Machine Hours

Manufacturing Overhead Rate = $5 per Machine Hour

This means the company allocates $5 of manufacturing overhead for every machine hour used in production. If a product requires 10 machine hours to manufacture, it will be assigned:

Allocated Overhead = 10 × $5

Allocated Overhead = $50

By regularly calculating manufacturing overhead and monitoring overhead rates, manufacturers can improve cost accuracy, optimize resource utilization, and make more informed operational and financial decisions.

Benefits of Effective Manufacturing Overhead Management

Manufacturing overhead can account for a significant portion of total production costs. Effectively managing these indirect expenses helps manufacturers gain greater control over their operations, improve cost accuracy, and enhance profitability.

By monitoring and optimizing overhead costs, businesses can make better decisions, allocate resources more efficiently, and maintain a competitive advantage in the market.

More Accurate Product Costing

Effective manufacturing overhead management ensures that indirect costs are allocated accurately across products. This provides a more realistic view of production costs and prevents underpricing or overpricing.

Accurate product costing helps manufacturers evaluate profitability at the product level, identify high-cost areas, and make informed decisions about pricing, production, and resource allocation.

Improved Profit Margins

Controlling overhead expenses reduces unnecessary spending and lowers overall production costs. When manufacturers identify inefficiencies, eliminate waste, and optimize resource usage, they can improve profit margins without compromising product quality.

Better overhead management also enables businesses to maintain profitability even during periods of rising material, labor, or operational costs.

Better Pricing Decisions

A clear understanding of manufacturing overhead allows businesses to establish pricing strategies based on actual production costs rather than estimates.

Accurate cost data helps ensure that products are priced competitively while maintaining healthy margins. This reduces the risk of selling products below cost and supports long-term financial sustainability.

Enhanced Budgeting and Forecasting

Tracking and analyzing overhead costs provides valuable insights for budgeting and financial planning. Manufacturers can anticipate future expenses more accurately, allocate funds effectively, and prepare for changes in production demand. Improved forecasting helps businesses avoid unexpected cost overruns and supports better strategic decision-making across departments.

Greater Operational Efficiency

Manufacturing overhead management often highlights inefficiencies in production processes, equipment utilization, and resource consumption. By addressing these issues, manufacturers can streamline operations, reduce downtime, and improve workflow performance. Greater operational efficiency leads to faster production cycles, lower costs, and more consistent output quality.

Improved Resource Utilization

Monitoring overhead costs helps manufacturers understand how effectively they are using labor, equipment, facilities, and utilities. This visibility enables better allocation of resources and reduces underutilization or overuse. Improved resource utilization contributes to higher productivity, lower operating costs, and better overall manufacturing performance.

Stronger Competitive Advantage

Manufacturers that effectively manage overhead costs can operate more efficiently and offer products at competitive prices. Lower production costs create opportunities to improve profitability, invest in innovation, and respond more quickly to market changes. As a result, businesses can strengthen their market position and achieve sustainable long-term growth.

Challenges in Managing Manufacturing Overhead

While manufacturing overhead is essential to keeping production operations running smoothly, managing these indirect costs can be challenging. Unlike direct materials and labor, overhead expenses are often difficult to track, allocate, and control.

Without proper oversight, rising overhead costs can reduce profitability, distort product costing, and limit operational efficiency.

Understanding these challenges is the first step toward improving cost management and making more informed business decisions.

Rising Energy and Utility Costs

Energy and utility expenses are a significant component of manufacturing overhead and can fluctuate due to market conditions, seasonal demand, and regulatory changes.

Rising electricity, water, and fuel costs increase production expenses and can negatively impact profit margins. Manufacturers often struggle to predict and manage these costs, especially in energy-intensive production environments.

Inaccurate Cost Allocation Methods

Allocating overhead costs to products can be complex, particularly when multiple products or production lines share the same resources. Using outdated or inappropriate allocation methods may result in inaccurate product costing, leading to poor pricing decisions and distorted profitability analysis. This challenge becomes more pronounced as manufacturing operations grow in complexity.

Lack of Real-Time Cost Visibility

Many manufacturers rely on manual processes or disconnected systems to track overhead expenses. As a result, they may not have real-time visibility into production costs, resource usage, or operational inefficiencies. Delayed access to cost data makes it difficult to identify problems quickly and take corrective action before expenses escalate.

Equipment Downtime and Maintenance Expenses

Unexpected machine breakdowns and unplanned maintenance can significantly increase manufacturing overhead. Downtime not only leads to repair costs but also reduces production capacity and delays order fulfillment. Without a proactive maintenance strategy, manufacturers may experience frequent disruptions that drive up indirect production costs.

Production Inefficiencies and Waste

Inefficient production processes, excessive material waste, rework, and poor workflow management can increase overhead costs over time. These inefficiencies consume additional resources, labor, energy, and machine capacity without generating additional value. Identifying and eliminating operational bottlenecks is often a major challenge for manufacturers seeking to control overhead expenses.

Manual Tracking and Reporting Errors

Many organizations still use spreadsheets and manual record-keeping to monitor overhead costs. These methods are time-consuming and prone to errors, inconsistencies, and data duplication. Inaccurate reporting can lead to poor financial decisions, budgeting issues, and difficulty in identifying the true drivers of manufacturing overhead costs.

Fluctuating Production Volumes

Changes in production demand can make overhead management more difficult. Fixed overhead costs remain relatively constant regardless of output levels, which means lower production volumes can increase the overhead cost per unit. Manufacturers must carefully balance capacity utilization and production planning to minimize the impact of demand fluctuations on overall costs.

Difficulty Measuring Resource Utilization

Tracking how effectively equipment, facilities, utilities, and labor resources are being used can be challenging without proper monitoring systems. Limited visibility into resource utilization often results in underused assets, unnecessary expenses, and missed opportunities for cost optimization. Accurate measurement is essential for improving efficiency and reducing overhead costs.

10 Strategies to Reduce Manufacturing Overhead Costs

Reducing manufacturing overhead costs is essential for improving profitability, maintaining competitive pricing, and enhancing operational efficiency.

While overhead expenses cannot be eliminated entirely, manufacturers can implement targeted strategies to optimize resource utilization, minimize waste, and gain better control over indirect production costs.

The following strategies can help businesses effectively reduce manufacturing overhead while maintaining productivity and product quality.

Improve Production Planning and Scheduling

Effective production planning helps manufacturers optimize resource utilization and minimize idle time. By creating accurate production schedules, businesses can reduce machine downtime, prevent bottlenecks, and ensure labor and equipment are used efficiently. Better scheduling also helps avoid costly production delays and unnecessary overtime expenses.

Reduce Equipment Downtime Through Preventive Maintenance

Unexpected equipment failures often lead to higher repair costs, production interruptions, and increased overhead expenses. Implementing a preventive maintenance program helps identify potential issues before they become major problems. Regular inspections, servicing, and maintenance improve equipment reliability, extend asset lifespan, and reduce costly unplanned downtime.

Automate Manual Processes

Automation can significantly reduce labor-intensive tasks and improve operational efficiency. Automating activities such as inventory tracking, production monitoring, data entry, and reporting minimizes human error and reduces administrative overhead. It also allows employees to focus on higher-value activities that contribute directly to productivity and business growth.

Optimize Energy Consumption

Energy costs are a major component of manufacturing overhead. Manufacturers can lower utility expenses by upgrading to energy-efficient equipment, monitoring energy usage, and implementing conservation initiatives. Simple measures such as optimizing machine operation schedules, reducing idle equipment time, and improving facility lighting can generate substantial cost savings over time.

Improve Inventory Management

Poor inventory management can lead to excess stock, storage costs, obsolescence, and production inefficiencies. Maintaining optimal inventory levels helps reduce carrying costs while ensuring materials are available when needed. Accurate inventory tracking and demand forecasting also minimize waste and improve overall operational efficiency.

Minimize Material Waste and Scrap

Material waste directly increases production costs and contributes to higher overhead expenses. Manufacturers can reduce waste by improving quality control processes, standardizing work procedures, and continuously monitoring production performance. Identifying the root causes of scrap and rework helps lower material consumption and improve resource utilization.

Increase Workforce Productivity

A well-trained and productive workforce can help reduce indirect costs associated with delays, errors, and inefficiencies. Providing employee training, improving communication, and establishing clear performance goals can enhance productivity. Higher workforce efficiency enables manufacturers to achieve greater output without significantly increasing overhead expenses.

Monitor Costs with Real-Time Reporting

Real-time visibility into manufacturing costs enables businesses to identify inefficiencies and address issues before they escalate. Tracking overhead expenses through dashboards and automated reporting systems helps managers make faster, data-driven decisions. Continuous monitoring also supports more accurate budgeting and cost control initiatives.

Standardize Operational Processes

Standardized procedures improve consistency, reduce errors, and streamline production activities. Establishing best practices for manufacturing operations, maintenance, quality control, and inventory management helps eliminate unnecessary variations that contribute to higher overhead costs. Consistent processes also improve productivity and operational performance across the organization.

Leverage ERP and Manufacturing Software

Modern ERP and manufacturing management systems provide greater visibility into production costs, resource utilization, and operational performance. These solutions automate data collection, improve planning accuracy, and support real-time decision-making. By centralizing information and identifying inefficiencies, manufacturers can better control overhead expenses and drive continuous cost improvements.

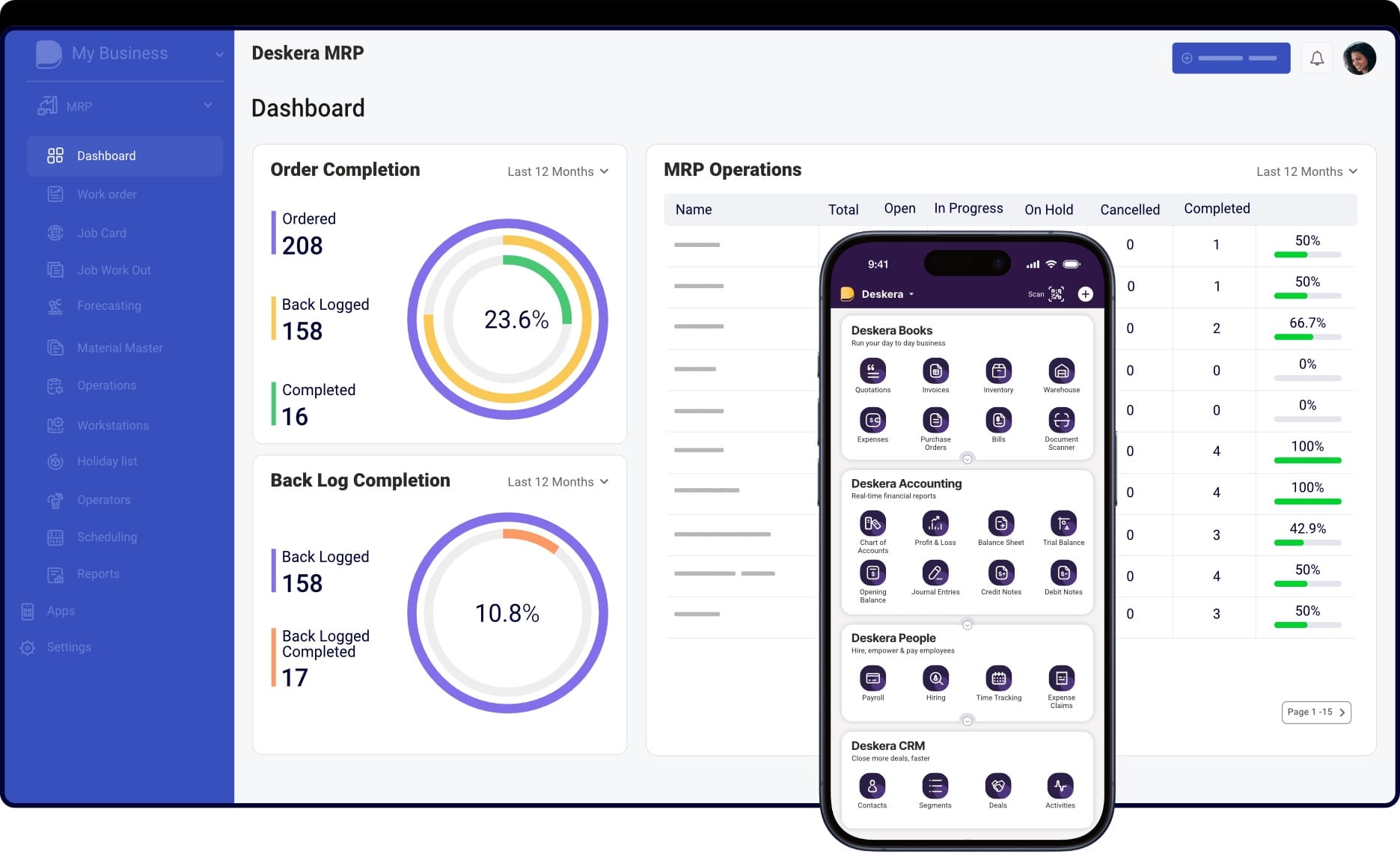

How Deskera MRP Helps Manufacturers Manage and Reduce Manufacturing Overhead

Managing manufacturing overhead requires visibility into production costs, resource utilization, machine performance, inventory levels, and operational efficiency. Deskera MRP helps manufacturers gain greater control over these cost drivers by integrating production planning, inventory management, machine maintenance, costing, and reporting into a single platform. This enables businesses to reduce inefficiencies, optimize resources, and make more informed decisions to improve profitability.

Real-Time Production Cost Tracking

Deskera MRP helps manufacturers track production activities and associated costs in real time. By providing visibility into work orders, production progress, and resource consumption, businesses can identify cost overruns early and take corrective action. This improves cost control and helps ensure manufacturing overhead is allocated more accurately across products.

Production Planning and Scheduling Optimization

Inefficient scheduling often leads to idle labor, machine downtime, and unnecessary overhead expenses. Deskera MRP's production planning and scheduling capabilities help manufacturers allocate resources effectively, balance workloads, and streamline production workflows. Better planning reduces delays, improves capacity utilization, and lowers indirect production costs.

Material Requirement Planning and Inventory Control

Excess inventory, stock shortages, and inefficient material management can significantly increase manufacturing overhead. Deskera MRP helps manufacturers plan material requirements, monitor inventory levels, and align procurement with production demand. This reduces carrying costs, minimizes waste, and ensures materials are available when needed without tying up excess working capital.

Machine Management and Preventive Maintenance

Unexpected equipment breakdowns can increase maintenance costs and production downtime. Deskera MRP includes machine management and maintenance capabilities that help manufacturers monitor machine performance, automate maintenance schedules, and track maintenance activities. This proactive approach improves equipment reliability, reduces downtime, and lowers overhead costs associated with repairs and production interruptions.

WIP Tracking and Bottleneck Identification

Work-in-progress (WIP) tracking provides real-time visibility into production status and resource utilization. Deskera MRP enables manufacturers to monitor production flow, identify bottlenecks, and address inefficiencies before they impact operations. Improved workflow visibility helps reduce delays, improve throughput, and optimize overhead-related expenses.

Yield Calculation and Scrap Management

Material waste and production scrap contribute directly to higher manufacturing overhead. Deskera MRP helps manufacturers track yields, monitor finished goods costs, and manage by-products and scrap. By identifying sources of waste and improving production efficiency, businesses can reduce unnecessary expenses and improve overall profitability.

Advanced Reporting and Cost Analysis

Deskera MRP provides comprehensive production reports and analytics that help manufacturers monitor costs, efficiency, and profitability. Real-time reporting enables managers to evaluate overhead trends, identify cost-saving opportunities, and make data-driven decisions. This level of visibility supports continuous improvement and more effective overhead management.

AI-Powered Insights and Decision-Making

Deskera's AI assistant, David, helps manufacturers access reports, insights, and recommendations more quickly. Combined with real-time operational data, AI-powered insights help managers identify inefficiencies, improve planning accuracy, and optimize resource utilization. This enables faster decision-making and supports ongoing efforts to reduce manufacturing overhead costs.

By combining production planning, inventory management, machine maintenance, costing, reporting, and AI-driven insights in a unified platform, Deskera MRP helps manufacturers improve operational efficiency, reduce indirect production expenses, and maintain better control over manufacturing overhead costs.

Key Takeaways

- Manufacturing overhead (MOH) includes all indirect production costs, such as utilities, factory rent, maintenance, depreciation, and indirect labor, that support manufacturing operations but cannot be directly traced to specific products.

- Manufacturing overhead differs from direct materials and direct labor because it represents the indirect expenses required to keep production facilities running efficiently.

- Manufacturing overhead costs are typically categorized into fixed, variable, and semi-variable overhead, each affecting production costs and budgeting differently.

- Common manufacturing overhead expenses include factory utilities, equipment depreciation, maintenance costs, quality control activities, insurance, and indirect materials and labor.

- Calculating manufacturing overhead involves identifying all indirect production costs, determining total overhead expenses, and allocating them using an appropriate allocation base.

- Manufacturing overhead rates help businesses distribute indirect costs accurately across products using allocation bases such as direct labor hours, labor costs, machine hours, or units produced.

- Manufacturers often face challenges in managing overhead due to rising utility costs, inaccurate cost allocation, equipment downtime, production inefficiencies, and limited visibility into real-time costs.

- Reducing manufacturing overhead requires a combination of strategies, including better production planning, preventive maintenance, automation, energy optimization, inventory control, waste reduction, and process standardization.

- Effective manufacturing overhead management improves product costing accuracy, profit margins, pricing decisions, budgeting, resource utilization, operational efficiency, and long-term competitiveness.

- Monitoring key metrics such as overhead rate, overhead cost per unit, machine utilization, capacity utilization, maintenance costs, energy consumption, scrap rates, and OEE helps manufacturers control overhead expenses more effectively.

- Deskera MRP helps manufacturers reduce manufacturing overhead by providing real-time production visibility, production planning, inventory control, machine maintenance management, cost tracking, advanced reporting, and AI-powered insights for better decision-making.

Related Articles