Organizations spend a significant amount of money to determine the level of public demand for their products and services. There are consistent studies and researches conducted to verify if the manufactured product will be saleable. Incorrect estimates can lead to dire results and losses. Supply and demand are both proportionately important to drive the economy.

A Fundamental Concept

Supply and demand patterns form the foundation of the modern economy. The price, utility, and people's preferences affect the supply and demand patterns.

When there's a huge demand for a good despite a price-rise the manufacturers will increase the supply.

We will explore supply and demand in great detail in this article. If you are looking to understand supply and demand and how it impacts markets and your business, then you are in the right place.

This article will cover:

- Supply and demand definitions

- Law of supply and demand

- How supply and demand affect each other

- How supply and demand affect market prices

- What if supply is more than demand?

- What if demand is more than supply?

- Exceptions to the law of supply and demand

What is Supply?

In economics, supply is a concept that describes the total quantity of goods, or inventory, available to the consumers. Supply depends on the quantity of goods available at a particular price. Because of this fact, supply is closely related to demand. This implies that when the demand for goods increase, the supply also increases. Moreover, supply also increases when the price increases as the manufacturers would like to produce goods that help them maximize their profits.

Factors Affecting Supply

While supply could relate to anything that has competitive market demand, it is usually spoken of in context to goods, labor, or services.

Supply is a concept that is measured through a lot of formulas and is determined through various factors. One such immensely important factor is the price of a product as it plays a crucial role in the process of supply. We often observe that the supply increases with an increase in the price. Apart from the main good, the prices of raw materials and labor also affect the supply. After all, the prices of the related items or services also contribute to the overall price of the main good.

The mathematical formulas for supply establish a relation between supply and the factors affecting it, like the price of the good. Apart from the ones seen in the previous section, the market influences, government rules, and inflation could be other reasons for affecting the supply.

Having learned some basics about supply, let’s move on to its close relative: Demand.

What is Demand?

Just like supply, demand is an economic concept. The readiness and potential of consumers to purchase a specific quantity of a good or service at a specific point in time or over a specific period of time are referred to as demand.

Demand can be categorized as:

Market demand: It signifies the demand for a specific good.

Aggregate demand: Aggregate demand stands for the demand for all the goods.

Factors Affecting Demand

With the increase of supply, the price tends to reduce owing to the continuing demand. Theoretically, the markets will reach a point of balance where the supply is equal to demand for a certain price point. This will mean there is no oversupply and no shortfall either; which in turn ensures a beneficial utility to consumers and maximization of profits for the manufacturers.

Economic concepts- Supply and Demand, are equally responsible for the impact on the prices of goods and services. The association between supply and demand eventually gets balanced. This is called an equilibrium price as per the market economy theory.

One of the primary reasons for consumers to purchase a product is its low price whereas the manufacturers want to maximize their profits by increasing the prices. If the prices increase, the customers may not purchase the particular product and the demand for the product takes a dip. This will lead to a loss for the suppliers as the products are not consumed enough.

Similarly, if the prices go down then the demand may increase but again, the suppliers would be at loss due to reduced profits. Therefore, supply and demand are said to be very closely associated.

Some factors that affect demand are:

- The overall appeal of the good

- Competition faced from rival products

- Financing for the said product

- Quantity available in the market

What is the Law of Supply and Demand?

By definition, Law of supply and demand depicts the association between the sellers and purchasers of a particular good. It is a theory that describes the relationship between the price of a particular good or product and people's willingness to buy or sell it. In general, people tend to supply more and demand less as prices rise, while the reverse is true if the prices fall.

It is a theory that takes from both: the law of supply and the law of demand.

Law of Supply: On one side, the law of supply states that the higher the cost of the goods, the more is the supply from the sellers.

Law of Demand: On the other side, the law of demand states that the higher the prices, the lower will be the purchases from consumers.

Both these laws aid in determining the prices and quantities of goods traded in the economy.

Law of Supply and Demand: The Difference

Being one of the most fundamental economic laws, the laws of supply and demand are intertwined with almost all economic principles in some way.

The willingness of the consumers to supply and demand a product establishes the market equilibrium. This equilibrium can also be achieved when the suppliers readily supply the amount demanded by the consumers. Yet, numerous factors may affect supply and demand.

What is the Supply and Demand Curve?

The supply and demand curve will require us to consider the supply curve and demand curve independently.

Supply Curve

Supply represents the sellers’ perspective of maximizing their profits. A supply curve exhibits the quantity of the goods that a supplier is able and willing to provide for the consumers, at a price rise for a particular time.

Example:

For simplicity, we assume an economic backdrop where the producer sells directly to consumers. Here’s a schedule that depicts the fuel provided by the suppliers. The suppliers offer 50 liters per customer or consumer each week at the cost of $1.20 per liter. However, if the consumers are willing to pay $2 per liter, then the suppliers will provide 130 liters per week.

The supply graph for this is shown below:

The curve is an upward slope indicating a direct relationship between the price and the supply. With the price-rise, the supply rises, and with a fall in price, the supply dives down, too.

Demand Curve

From the same example, we shall understand the demand curve.

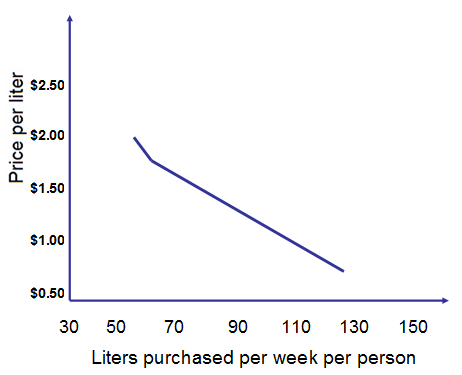

Demand implies the number of products the consumers are willing to buy at varying prices in certain time duration.

If the price of the fuel is $2.00 per liter, people willingly purchase 60 liters per week. In case of a price drop, $1.70 per liter, there may be a rise in consumption of say 70 liters per week. With a further reduction in prices: $1.50, people may purchase up to 75 liters each week.

With a reduced price per liter, people tend to make nonessential purchases. In this case, owing to the decline in fuel prices, they may buy surplus fuel or they may undertake unnecessary trips and journeys as the fuel prices fall within the budget bracket. But since the price is the factor that decides the purchasing capacity, if the prices rise again, there will be a dip in the demand.

The graph of this information is as follows:

The demand curve slopes downward. This indicates an inverse relationship between price and demand.

Equilibrium

Another essential aspect of the demand and supply curve is equilibrium. At this point, the demand and the supply for a good become equal. This means that neither is there a shortage nor a surplus of the good in the market. This equilibrium price can be seen in the following graph:

What Happens if Supply is More and Demand is Less?

More supply and less demand will lead to a lot of goods left behind for consumption. This scenario results in a surplus availability of the goods.

Surplus may be a result of very high prices of the goods, because of which people do not purchase goods and the demand reduces. In such a case, consumers either start buying substitute products or reduce their average purchase of this good.

Eliminating Surplus: To defeat surplus, the producers or suppliers will have to bring down the prices so that the customers resume their purchases.

What Happens if Demand is More and Supply is Less?

More demand and less supply will lead to lesser goods being available for the consumers resulting in a shortage of goods.

Shortage results when the products are priced very low. However, the chances of the prices shooting up are high as the competition to purchase catalyzes the price rise.

Eliminating Shortage:

The suppliers may restrict the supply so that the prices rise and they register profit, along with balancing out the shortage.

Exceptions to the Rule of Supply and Demand

Having learned about the laws of supply and demand in detail, we come to discuss the exception to the rules in both cases. Let’s start with the exceptions to the law of demand.

Exceptions to Law of Demand

Giffen and Veblen goods are the exceptions in this case. The experts believe that though these are rare occurrences and tough to prove, there are indeed instances where the law of demand gets breached.

Brushing up the concept before we move on: According to the law of demand, the quantity demanded increases when the prices fall; which is indicative of an inverse relationship between the price and quantity.

Giffen Goods

Giffen goods present a scenario where the demand increases even when the prices are increasing. The name comes from Sir Robert Giffen who introduced his observations. He observed that in the early 19th century, the low-wage British workers bought more bread despite the increased prices. This occurrence directly contradicts the Law of Demand.

The reason being that the increased prices of bread left the workers with little amount for meat. So, they compensated for the calories by buying more bread, using up the extra money remaining with them.

Giffen goods are generally regarded as inferior goods, as it reinforces that consumers consume more subpar goods despite the price-rise; this directly contradicts the Law of Demand and is therefore considered an exception.

Veblen Goods

This name also takes from the economist who introduced it. Thorstein Veblen stated that people perceived some higher-priced goods as having greater efficacy. An example of Veblen good is the diamonds. Due to its perceived worth, people will buy diamonds even if the prices keep rising. Veblen goods signify status and opulence and are much more visible in society than the Giffen goods. Luxury cars are another example here.

The Exception to Law of Supply

The Law of Supply states that as the cost of the good increases/decreases, the amount of good supplied decreases/increases respectively. Here are some factors that are exceptions to this law.

Competition: Sellers may reduce the prices of certain goods to stay relevant in the market competition. This disqualifies the law of supply.

Business change: When a business owner is planning to move to another trade, the chances are that he may sell off his stock at a lower price. So, a lot more is available to the new buyer at much lower prices. This cancels the Law of Supply.

Market Control: In other words, a monopoly can lead to a seller controlling the market supply despite the rise in prices. This again nullifies the law.

Perishable goods: Certain goods with an early expiry date may be given away at lower prices. This is done by sellers to avoid being at loss due to the perishability of the goods.

Authoritative Restriction on Quantities: Government regulations or the rules set by the local governing bodies could prohibit the sellers to produce beyond a regulated amount. Also, they may impose restrictions on the prices of some goods so that sellers do not sell the goods above the specified prices.

Artistic Goods: Even if there’s a surge in prices, artistic goods cannot be produced on demand. Therefore, such goods invalidate the law of supply.

Agricultural goods: Being a natural commodity, agricultural products cannot be supplied beyond a limit despite the price increase.

These are some of the areas where the Law of Supply cannot be applied.

Key Takeaways

And that's a wrap. With this systematic exploration of supply and demand, we pick up the following points from the article:

- Supply is the total quantity of goods or services that are available to the consumers.

- Demand is the consumer’s willingness to buy a product at a given price.

- Both demand and supply work hand-in-hand to determine the prices and the quantities of the goods in the market.

- The Law of Supply states that at higher prices of a good, the producers will supply a larger quantity to the market.

- The Law of Demand is a basic economic principle that states that higher prices will attract lesser demand from the consumers.

- Equilibrium is the stage where the supply and demand become equal.

- The condition when the Supply is more than the Demand is called Surplus.

- The condition where the Demand is more than the Supply is called Shortage.

- Price elasticity of a product is linked to its supply and demand curve.

Hope you have a better understanding of supply and demand, the cornerstones of modern economics and are able to use this understanding to run a better business.