Philippines is a country with thousands of islands. There are approximately seven thousand islands in the Philippines! Edged by pristine, turquoise-colored beaches and remarkable islands, the Philippines is divided into three geographical areas from north to south - Luzon, Visayas, and Mindanao, with Manila as the capital city.

With close to 111 million population in this country, the Philippines is ranked 25th as the world's largest economy by GDP and the third-highest economy by nominal GDP in Southeast Asia, after Indonesia and Thailand.

Although the Philippines is a famous hotspot for travellers around the world, it's also a great place to kickstart or establish your business as it's one of the emerging countries in the world - meaning you have higher business opportunities and have the chance to explore uncharted markets.

If you start your business in the Philippines, you first need to understand the VAT rules and regulations, whether you're a local or a foreigner.

Here's the guide to help you better understand the VAT rules in the Philippines. Let's begin.

What are the different types of tax rates?

On 1 January 1988, the Philippines has introduced the Value Added Tax (VAT) regulation, replacing the sales and turnover tax range.

There are three different tax rates in the Philippines: the standard rate, zero-rated supplies, and exempt supplies.

Standard Rated Supplies

The standard rate of supplies in the Philippines is 12% on most goods and services.

Some of the standard rated supplies are:

- Sales of goods and properties; 12% of the gross selling price or gross value of the products and properties sold

- Sales of services and use/lease of properties; 12% of gross receipts from the exchange of sales of services

- Importation of goods; the value of the tax used by the Bureau of Customs (BOC) in determining tariff, custom duties, excise taxes, and other charges.

- Any purchases made by a registered dealer in the course of business; VAT computation is based on a particular percentage of the purchase cost will be imposed on a VAT-registered dealer who buys goods or services from another supplier.

Zero-Rated Supplies

The zero-rated supplies are supplies with 0% VAT. It means that the products and services are taxable but with a 0% rate.

Here are some of the zero-rated supplies in the Philippines:

- Export of sales

- Any sales in foreign currency

- Any sales made to an individual or entity who are exempted under special laws of an international agreement

- Any sales of services conducted outside the Philippines

Effective on June 27, 2021, the Revenue Regulations has issued a 12% VAT on certain sales transactions that were subject to 0% VAT earlier.

Following are the sales transactions that are 12% VAT as per the new rules:

- Any sales of raw materials or packing materials to a foreigner for delivery to a local export-oriented enterprise

- Any sales of raw or packing materials to an export-oriented enterprise, whose sales are greater than 70% of the total annual productions

- Any export sales activities under Executive Order (EO) No.226, or the Omnibus Investment Code of 1987

- Any services performed by contractors or subcontractors in manufacturing, processing, or converting goods for an entity whose export sales exceed 70% of its total annual production.

Exempted Supplies

Tax-exempt supplies are goods and services free from tax - meaning that these goods and services are not taxable.

The reporting of tax-free items may be on a taxpayer's business or individual tax return for informational purposes only.

Stated below is a list of products and services that are exempted from VAT under SEC 109 and CREATE LAW (as of 1 January 2021):

- Any services provided by the financial intermediaries

- Invoice sales or importation of medicine for cancer, mental illness, and kidney diseases

- Any sales, importation, printing, or publication of the journal, or any educational materials covered by the UNESCO

- Any sales or importation of COVID-19 related medicines, medical supplies, and equipment from 1 January 2021 to 31 December 2023

- Any sales or importation of fertilizer, seeds, and seedlings

What is an excise tax?

The excise tax is the tax imposed on specific goods and services paid by businesses to the government. The tax is imposed on the consumers, which means they will have to pay an exorbitant price for the excise goods.

In the Philippines, the excise rate is imposed on alcohol products, tobacco products, petroleum products, mineral products, automobiles and other motor vehicles, and cosmetic procedures.

There are two excise taxes; specific tax (based on weight or volume or the u.o.m of the goods ) and ad valorem tax (based on selling price or other specified value of the goods/articles).

You can refer to the table below for the excise rate imposed on the goods listed/

A) Alcohol Products

B) Tobacco Products

In addition to that, an inspection fee is collected on leaf tobacco, cigars, cigarettes, scrap, and other manufactured tobacco products as well.

Refer to the inspection fee as per the table below.

C) Sweetened Beverages

You can visit the BIR official website if you wish to find out more about the excise rate for mineral products, automobiles, and petroleum products.

What is withholding tax (WHT)?

A withholding tax is when a business holds a portion of the payment of goods and services and then remits this payment to the government in the Philippines - which helps reduce the government's burden as the tax collection responsibility is shifted to the businesses.

In return, the businesses, also known as the tax withholding agents, will have to provide BIR Form 2307 (or Form 2306) as evidence that the supplier paid up. The businesses can deduct the tax amount withheld from their income tax for the taxable period.

What are the different types of withholding tax?

There are two types of withholding tax in the Philippines. They are:

Creditable withholding tax (CWT)

- Compensation: This withholding tax arises from any income payment from an employer-employee relationship

- Expanded: This withholding tax is prescribed on specific income payments. The amount is creditable against the income tax due of the payee for the taxable period

- Withholding Tax on GMP - Value-Added Taxes (GVAT): This withholding tax is performed by the National Government Agencies (NGAs), government-owned, controlled corporations, and local government units (LGUs) before making any payment to VAT-registered taxpayers on their purchases of goods and services

- Withholding Tax on Government Money Payments (GMP) - Percentage Taxes: This withholding tax is performed by the National Government Agencies (NGAs), government-owned, controlled corporations, and local government units (LGUs) before making any payment to non-VAT registered taxpayers on their purchases of goods and services

Final Withholding Tax (FWT)

This withholding tax is prescribed on specific income payments. It's not creditable against the income tax for the taxable period.

The total income tax is complete, and the final payment of income tax due from the payee is subject to the final withholding tax.

Does withholding tax apply to all suppliers?

Only regular suppliers are subject to withholding tax. If the withholding agent has transacted with a supplier at least six times for the current and previous year or transacted at least P10,000 in a single purchase, then the withholding tax applies.

*As a withholding tax agent, you must deduct 1% of the value of payments for purchases of goods and 2% for the purchases of services (EWT) from all local suppliers and withhold tax from non-resident doing business in the Philippines.

Who are the withholding tax agents?

A Withholding Agent can be a person or an entity in control of the payment subject to withholding tax. Therefore, they are required to deduct and remit the withheld taxes to the government.

Stated below are the groups classified as the Top Withholding Agents (TWAs) in the Philippines:

- Top 20,000 private companies and top 25,000 individual taxpayers under RR No.6-2009

- Top 500 non-individual taxpayers that meet the requirements of a large taxpayer but have yet to be designated by the BIR, under RMO 17-2017

- Large taxpayers under Revenue Regulation No. 1-1998, as amended by Sections 4.5, 5.1, and 5.2 under RR 17-2010

- Those identified under the Taxpayer Account Management Program (TAMP) as per RR-2014

To find out about the latest withholding agent list, you can check the BIR website to keep yourself updated.

Do I need to register for VAT?

If you provide taxable supplies and your annual sales threshold exceeds PHP 3 million, yes, you must register for VAT. By any chance, if you wish to register for VAT, even though you do not meet the annual threshold, you can still opt to register for VAT voluntarily.

What is Tax Identification Number (TIN)?

A tax identification number (TIN) is a special string of numbers assigned to every taxpayer in the Philippines. It is a 12-digit number, with the first nine numbers are the TIN itself, and the last three numbers are the branch code. If you're a corporation, your first number will start with 0. For individuals, the first number will start from 1 to 9.

It's essential to get your tax identification number. You will need to use the TIN to file personal income tax, corporate tax, VAT returns and deal with the Bureau of Internal Revenue.

How do I register for my Tax Identification Number (TIN)?

Go to your Revenue District Office(RDO) near your residential area.

Inform the BIR officer that you intend to apply for a tax identification number (TIN).

To complete the TIN registration process, you will need to provide the following information:

- Fully furnished Form 1901 (those with mixed incomes, those who are self-employed, estates and trusts), Form 1902 (individuals that are non-resident citizens, resident aliens and employees with a purely compensation-based income), Form 1903 (corporations and partnerships), or Form 1904 (one-time taxpayers working)

- Birth certificate, passport, LTO driver's license, work permit, community tax certificate, business name certificate, etc

- Marriage contract for women

- Passport with your current visa or employment contract for foreigners

Once you have submitted all the documents, the BIR officer will process your tax identification number (TIN). You will receive a copy of the respective form at the end, indicating your tax identification number.

To reduce the high number of visitors in the Revenue District Office, the government has allowed its citizen to apply for TIN online. You can visit the BIR website to register online.

Note: Only self-employed, mixed-income earners, employees, and unemployed categories under the Executive Order No.98 can register online.

How do I register for VAT?

Once you have registered your business in the Philippines, the BIR will send you a Certificate of Registration (Form 2303), highlighting the corporate taxes that your company must pay.

On the Certificate of Registration (Form 2303), you can find the information on whether your company is VAT-registered or not. If your company is not VAT-registered during the initial stage, it doesn't mean that you do not need to register for VAT after that.

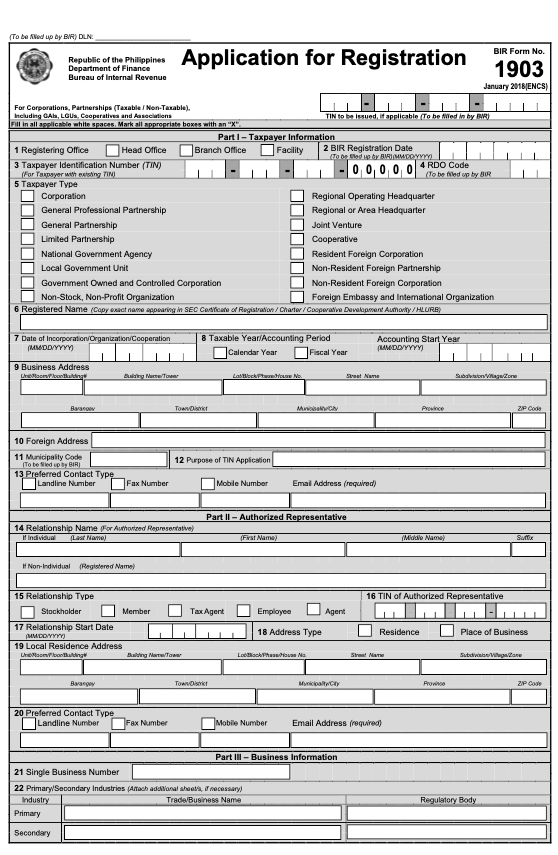

To register for Certificate of Registration (COR), corporations must submit Form 1903 to the BIR. So, what is Form 1903?

Form 1903 is a tax form submitted by corporations or partnerships to register their organizations with the Bureau of Revenue (BIR) in the Philippines.

If you wish to download the Form 1903, you can click on this link Form 1903.

When is the due date of my VAT Return's filing?

Every business owner must file the monthly paper return of their VAT Return by the 20th of the following month after their taxable period.

If you are filing your VAT Return using electronics, you can submit your monthly VAT Returns between the 21st to 25th, the following month.

You will also have to submit the details of your sales or receipts and VAT every quarter. Once you have filed your VAT Return, you will have to remit your tax payment simultaneously.

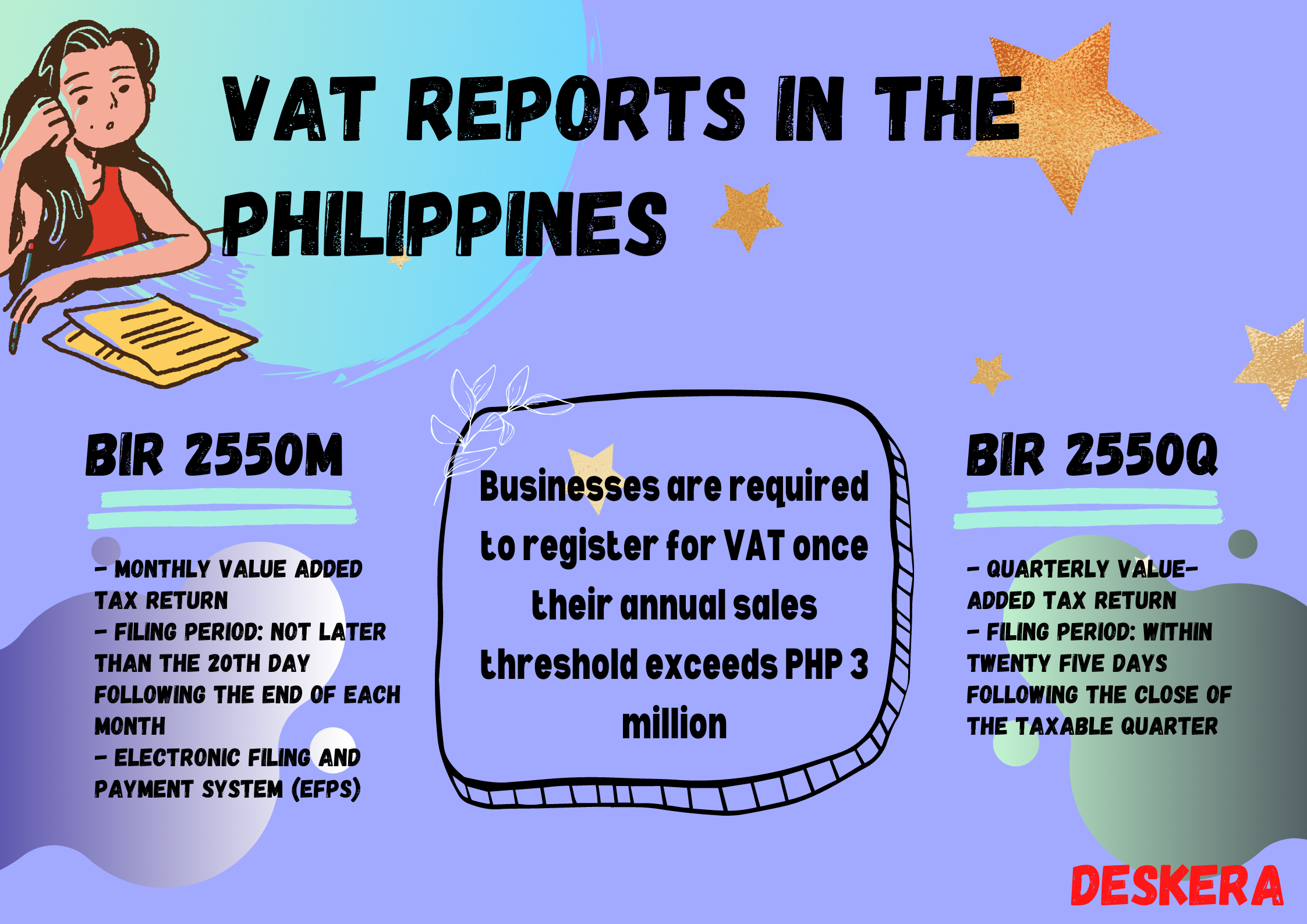

What are the VAT reports in the Philippines?

There are two types of VAT reports in the Philippines, and they are;

A. BIR Form No. 2550M

BIR Form No.2550M is the monthly Value-Added-Tax Declarations, a form outlining the sales tax imposed on sales of goods and services in the Philippines. A VAT-registered person shall perform the return in the Philippines.

The taxpayers will have to file this return if;

- their VAT registration has not been canceled

- there are no taxable sales for the month, or

- the aggregate sales/receipts for any 12 months did not exceed the PHP 1,500,000.00 threshold

Using manual filing, the BIR Form 2550M should be submitted no later than 20th the following month after the taxable period.

Suppose you are filing your VAT return using the Electronic Filing and Payment System (eFPS); you will have to check the filing period based on the group assigned to each business category.

You can refer to the table below regarding the filing period for different business groups using eFPS.

B. BIR Form No. 2550Q

Also known as Quarterly Value-Added Tax Return, Form 2550Q is a form outlining the sales tax on sales of goods and services in the Philippines, filed every quarter.

You must file Form 2550Q if your business' actual gross sales or receipts exceed P3,000,000.00. You have to file Form 2550Q no later than the 25th of the following month for your taxable quarter.

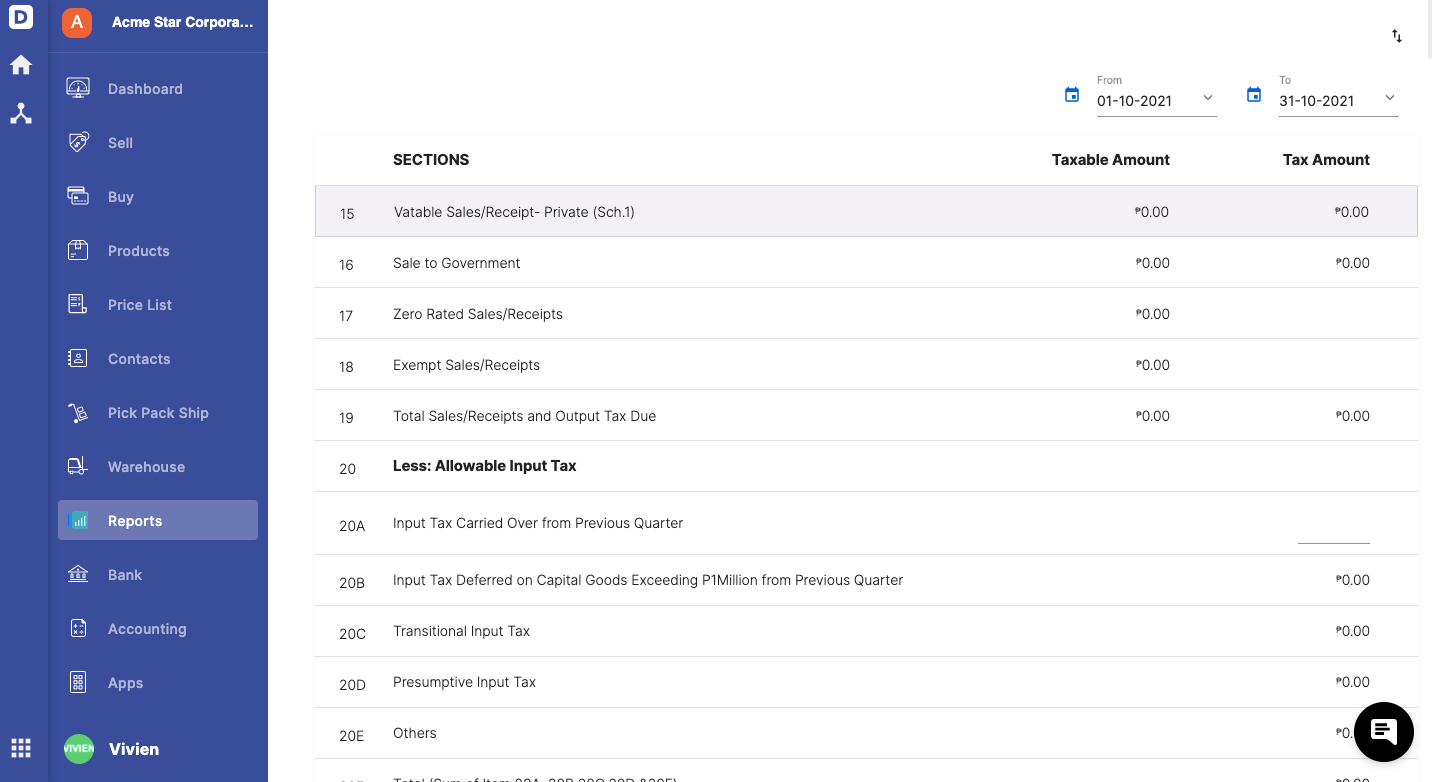

The table below explains the meaning of each section in Form 2550Q.

How do I make VAT payment?

Stated below are the ways you can make your VAT payment:

- Pay at any Authorized Agent Bank (AAB) under the jurisdiction of Revenue District Office (RDO)/Large Taxpayers District Office (LTDO) where the taxpayer (head office of the business establishment) is registered.

- For places without AAB - file your Monthly VAT declaration and pay the VAT due to the Revenue Collection Officer (RCO). The RCO will issue the payment receipt to you.

- Using online services such as PayMaya, LandBank, Union Bank, PesoNet, GlobeGCash, etc.

What are the penalties for late filing and payment?

Under the tax code section 255, for anyone who fails to file or pay VAT to the internal revenue tax, a fine not less than P10,000 will be imposed on you and imprisonment not less than one year but not more than ten years.

Note: Make sure that you file your VAT Return and promptly make payment to avoid surcharges, interest, and penalties.

BIR, VAT and Invoicing in the Philippines Using Deskera Books

Generating V.A.T. and B.I.R. reports is a piece of cake with Deskera. You can set up your Philippines company in minutes and start creating and sending invoices immediately.

In addition, you can generate beautiful invoice templates from the system without the need to design your template from scratch.

Start adding essential pieces of information when you are creating an invoice using Deskera Books, such as;

- Your company name and address

- The date when you issue the invoice

- Your tax identification number (TIN)

- Your customer's name, bill-to, and ship-to address

- Term of Payment

- List of line items with its respective U.O.M., price per unit, and tax, if applied

- The total sum of the invoice payment

- Memo or invoice description

And send the invoices to the customers effortlessly.

Learn more about the invoicing feature using Deskera Books.

Key Takeaways

And that is a wrap. From this article, you can take away the following points:

- What are the different types of tax rates?

- What is an excise tax?

- What is withholding tax (WHT)?

- What are the different types of withholding tax?

- Does withholding tax apply to all suppliers?

- Who are the withholding tax agents?

- Do I need to register for VAT?

- What is Tax Identification Number (TIN)?

- How do I register for my Tax Identification Number (TIN)?

- How do I register for VAT?

- When is the due date of my VAT Return filing?

- What are the VAT reports in the Philippines?

- How do I make a VAT payment?

- What are the penalties for late filing and payment?

- BIR, VAT and Invoicing in the Philippines Using Deskera Books

You can rest assured as the software will do the work for your tax calculation. Instead of spending a tremendous amount of time on manual tasks, you can have more time for the things you love with Deskera.