Liabilities are never the problem; it’s the assets you need to worry about.

This statement refers to the financial position and the notion that one always has to pay off debts. To offset a debt/liability, you can use assets, and your company can include certain items on the asset side or write them off as required. This can result in inflation or deflation of the asset’s value, which makes your company’s assets unreliable or somewhat questionable. But the amount you owe is very much real.

Moving on, let’s understand the meaning of liabilities in accounting? Let’s understand this concept in great detail. Below is a snapshot of the ground to be covered in this article.

- What are liabilities in accounting?

- How to keep track of your liabilities?

- Classification of liabilities

- Liabilities on a balance sheet

- Common examples of liabilities

What are Liabilities in Accounting?

For a business, liabilities is what your business owes to other companies, organizations, employees, vendors, or government agencies. Common examples of liabilities include tax dues, salaries outstanding, vendor payments pending, purchases you made that are yet to be paid off, bank loans, etc.

You typically incur liabilities while conducting regular business operations. This number fluctuates continuously. So, if your business has more debts, you’ll have higher liabilities and vice-versa. Paying off the debts is the only way you can lower your business’s liabilities. Liabilities is found in the balance sheet with assets an owner's equity

How to keep track of your liabilities?

Whenever an invoice is generated, you incur a liability to your business, be it from your vendor or another organization. The money you owe is deemed a liability in standing, until you pay off the invoice. Keep track of your invoices using an accounting software like Deskera, and you can stay on top of your liabilities. Of course, you’ll have to pay them, but this way, at least you’ll have an idea of exactly how much amount you owe and to whom.

Loans are also considered a type of liability. You can take loans in your business’s name to help expand your small business. A mortgage is considered a liability until you pay back the entire principal amount along with interest to the bank or to the person you borrowed it from. For instance, you loaned a certain sum for the expansion of your business, which needs to be paid off over the next five years. Then the bank loan will stand as a liability in your balance sheet for the next five years or until you pay it off, whichever comes earlier.

Classification of Liabilities

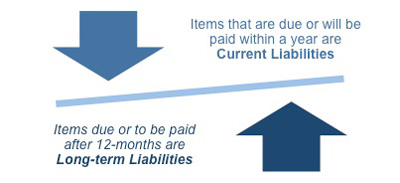

Liabilities are categorized into three types: Long-term liabilities, also known as non-current liabilities; short-term liabilities, also known as current liabilities; and contingent liabilities.

Long-term/Non-Current Liabilities

Any liability or money your business owes that will be paid off in more than a year, such as business loans, are known as long-term liabilities.

Examples of non-current liabilities

- Bonds payable

- Capital leases

- Deferred tax liabilities

- Long-term notes payable

- Mortgage payable

These types of liabilities are crucial in determining a company’s long-term solvency. If companies are unable to repay long term loans as they become due, the company can face a significant solvency crisis.

Short-term/Current Liabilities

What are the current liabilities? Also known as short-term liabilities, these are debts or money your business owes that needs to be paid off within a year. Short-term liabilities in accounting need to be overseen by the management to ensure that the company possesses enough liquid assets to guarantee that the debts are met.

Examples of current liabilities

- Accounts payable

- Accrued expenses

- Bank account overdrafts

- Bills payable

- Interest payable

- Income taxes payable

- Short-term loans

Contingent Liabilities

Contingent liabilities refer to those liabilities that “may” occur, depending upon the possible outcome of a future event. For instance, if your company is facing a lawsuit, you may need to pay a certain amount if you lose. That amount will stand as a contingent liability in your balance sheet, as you need to pay that amount only if you lose or settle. The losing or settling in the future is referred to as the “possible outcomes” in the definition.

Examples of contingent liabilities

- Lawsuits

- Product warranties

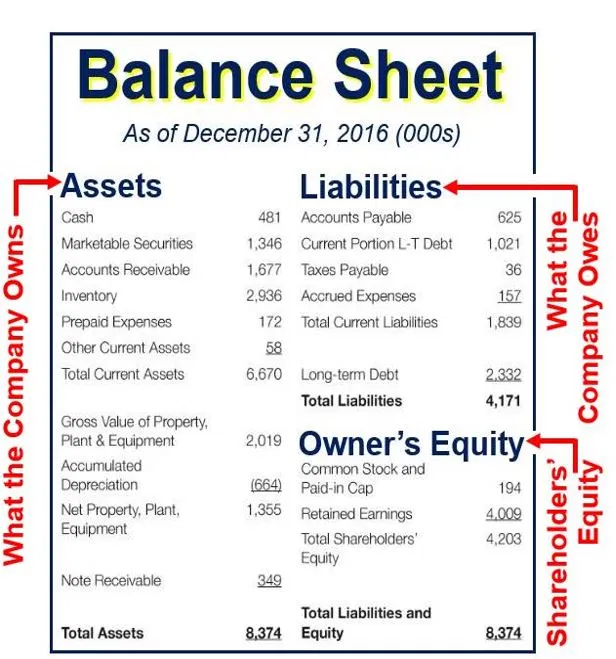

The below snapshot describes how the liabilities side of the balance sheet looks like.

Liabilities on a Balance Sheet

The financial report of a company generated from its accounting software gives a snapshot of its financial health, which mainly records three things:-

- Assets

- Equities

- Liabilities

An asset is anything that a firm owns and has a financial value, such as plant & machinery, revenue, etc. Assets are reflected on the left-hand side of a balance sheet.

On the other hand, liabilities are listed on the right-hand side and are subdivided into current and non-current liabilities, as discussed above.

Below is a sample balance sheet which displays the assets, liabilities, and equities clearly:-

Common Examples of Liabilities

Accounts Payable

Accounts payable is concerned with the amount of money your business owes to vendors for purchasing goods, raw material, or supplies. These are categorized under the current liabilities section of the balance sheet.

Income Taxes Payable

The amount of taxes your business owes to the government at the end of each financial year is known as income taxes payable. These are also recorded in the current liabilities section of the balance sheet.

Interest Payable

When you owe money to vendors or banking institutions and don’t pay it right away, you’ll likely need to pay interest. That amount which you pay in addition to the principal amount is known as interest payable.

Accrued Expenses

Accounting periods usually differ from the expense period, which is why accrued expenses come into play. For instance, you pay rent for the office space you operate out of. The rent for March became due, but you didn’t pay it until the next month. This amount is recorded as an accrued expense for the following month.

You can learn in great depth about liabilities and how each one is accounted in a balance sheet here.

Liabilities and Your Balance Sheet

A balance sheet gives you an accurate snapshot of everything you own or owe in the form of assets, liabilities, and equities. Liabilities play a crucial role in the balance sheet. By continually recording liabilities, you make sure your books are up-to-date, and an accurate representation of your finances is possible. A credible software like that of Deskera can help you keep track of your expenses, incomes, accruals, and receivables. Leverage such software and make sure your financials are streamlined. Deskera also provides a free mobile app for business accounting where you can keep a tab on your business from anywhere and get access to all financial reports.

Download the free Deskera app and run your business efficiently.