Why do many businesses now see lease obligations appearing directly on their balance sheets? The answer lies in modern accounting standards that require companies to recognize the financial commitments associated with leases. Instead of treating most leases as simple operating expenses, businesses must now record lease liabilities—representing the present value of future lease payments—making financial statements more transparent and reflective of actual obligations.

Lease liabilities play a crucial role in accounting because they represent a company’s contractual responsibility to make payments for leased assets such as office spaces, machinery, vehicles, or equipment. By recognizing these liabilities, businesses can present a clearer picture of their financial health, helping stakeholders, investors, and lenders better understand the company’s long-term commitments. This shift has significantly improved financial reporting accuracy and comparability across organizations.

However, managing lease liabilities can be complex. Businesses must determine lease terms, calculate the present value of lease payments, apply appropriate discount rates, and ensure compliance with accounting standards such as IFRS 16 and ASC 842. For organizations with multiple leases, tracking these obligations manually can quickly become challenging, increasing the risk of errors and compliance issues.

This is where solutions like Deskera ERP can make a difference. Deskera ERP helps businesses streamline financial management by centralizing lease-related data, automating accounting processes, and generating accurate financial reports. With real-time insights, automated calculations, and seamless integration with accounting workflows, Deskera enables companies to manage lease liabilities more efficiently while ensuring compliance and financial accuracy.

What Are Lease Liabilities in Accounting?

Lease liabilities refer to the financial obligation a business has to make future payments for assets it leases rather than owns. When a company signs a lease agreement for assets such as office space, machinery, or vehicles, it gains the right to use that asset for a specified period. In accounting terms, the present value of the future lease payments associated with that agreement is recorded as a lease liability, reflecting the company’s contractual commitment over the lease term.

Modern accounting standards require companies to recognize these obligations more transparently. Under IFRS 16, most leases must be recorded directly on the balance sheet. This means businesses must recognize both a lease liability, representing the obligation to make lease payments, and a corresponding right-of-use (ROU) asset, representing the company’s right to use the leased asset during the lease period. This approach significantly improved financial transparency by bringing many previously off-balance-sheet lease commitments into formal financial reporting.

However, not all accounting frameworks follow identical rules. For example, under FRS 102, finance leases result in the recognition of lease liabilities, while operating leases may continue to be treated differently. Some organizations choose to apply principles similar to IFRS 16 to maintain consistency across group reporting or internal financial policies. Understanding the applicable accounting standard is therefore essential, as it directly affects how lease liabilities are calculated, reported, and disclosed.

It is also important to note that lease liabilities differ from traditional debt obligations. While both represent future payment commitments, lease liabilities arise specifically from the right to use a leased asset rather than from borrowing funds. As a result, they follow unique measurement, amortization, and disclosure rules. Properly accounting for lease liabilities helps businesses present a clearer picture of their financial commitments, which can influence financial ratios, borrowing capacity, and investor confidence.

Understanding Lease Accounting Standards

Lease accounting standards define how businesses recognize, measure, and report lease transactions in their financial statements. These standards were updated to improve financial transparency and ensure that companies properly disclose their lease obligations. Two of the most widely used standards governing lease accounting are IFRS 16 and ASC 842, both of which require businesses to bring most lease obligations onto the balance sheet.

IFRS 16

IFRS 16, issued by the International Accounting Standards Board (IASB), significantly changed how leases are accounted for under international financial reporting standards. The primary goal of this standard is to increase transparency by ensuring that lease commitments are clearly reflected in a company’s financial statements.

Key principles

The core principle of IFRS 16 is that a company must recognize assets and liabilities arising from most lease agreements. Instead of categorizing leases as operating or finance leases from the lessee’s perspective, the standard requires businesses to account for nearly all leases using a single accounting model. This approach ensures that lease obligations are visible to investors, lenders, and other stakeholders.

Recognition of right-of-use assets and lease liabilities

Under IFRS 16, when a company enters into a lease agreement with a term longer than 12 months, it must record two items on the balance sheet:

- A right-of-use (ROU) asset, representing the company’s right to use the leased asset during the lease term

- A lease liability, representing the present value of future lease payments the company is obligated to make

The lease liability is initially measured using the present value of lease payments over the lease period, typically discounted using the interest rate implicit in the lease or the company’s incremental borrowing rate.

Impact on financial reporting

IFRS 16 has a significant impact on financial statements. By bringing lease obligations onto the balance sheet, the standard increases both reported assets and liabilities. This can affect key financial ratios such as debt-to-equity, return on assets, and EBITDA. As a result, investors and lenders gain a more accurate view of a company’s financial commitments and long-term obligations.

ASC 842

ASC 842 is the lease accounting standard issued by the Financial Accounting Standards Board (FASB) and is used by organizations reporting under US GAAP. Like IFRS 16, ASC 842 was introduced to improve transparency by requiring companies to recognize lease obligations on the balance sheet.

Overview of the US GAAP standard

ASC 842 requires companies to record both a lease liability and a right-of-use asset for most leases with a term of more than 12 months. The lease liability represents the present value of future lease payments, while the right-of-use asset reflects the company’s right to use the leased asset during the lease period. This standard applies to a wide range of leased assets, including buildings, vehicles, equipment, and technology infrastructure.

Key differences from previous lease accounting rules

Before ASC 842, lease accounting under ASC 840 allowed many operating leases to remain off the balance sheet. Companies only recognized lease expenses in the income statement, while the associated obligations were disclosed in the notes to financial statements. ASC 842 eliminated this lack of transparency by requiring operating leases to be recognized on the balance sheet as well.

However, ASC 842 still maintains a distinction between operating leases and finance leases for expense recognition in the income statement. This differs from IFRS 16, which uses a single accounting model for lessees. Despite these differences, both standards share the same objective: providing stakeholders with a clearer and more complete view of a company’s lease-related financial commitments.

Key Components of Lease Liabilities

Lease liabilities are calculated based on several important elements defined within a lease agreement. These components determine the total obligation a business must recognize on its balance sheet. Understanding these elements is essential because they directly influence how lease liabilities are measured, reported, and adjusted throughout the lease term.

Each component plays a role in determining the present value of future lease payments and ensuring accurate financial reporting.

Lease Payments

Lease payments form the foundation of a lease liability calculation. These are the fixed or predetermined payments that a lessee is required to make to the lessor over the duration of the lease agreement.

Lease payments typically include base rental charges, fixed service fees, and any other payments specified in the contract. When calculating lease liabilities, these payments are projected over the lease term and discounted to their present value to determine the amount recorded on the balance sheet.

Discount Rate

The discount rate is used to calculate the present value of future lease payments. Since lease payments are made over time, they must be adjusted to reflect their current value at the start of the lease. Businesses generally use the interest rate implicit in the lease if it can be easily determined.

If not, they may use the company’s incremental borrowing rate, which represents the rate the company would pay to borrow funds to purchase a similar asset. The chosen discount rate significantly affects the size of the recognized lease liability.

Lease Term

The lease term represents the total period during which the lessee has the right to use the leased asset. This includes the non-cancellable lease period as well as any renewal options that the lessee is reasonably certain to exercise.

Determining the correct lease term is important because it influences the number of payments included in the lease liability calculation. A longer lease term results in a higher liability since more payments must be recognized.

Variable Lease Payments

Variable lease payments are amounts that may change depending on specific conditions outlined in the lease agreement. These payments might be linked to factors such as usage levels, performance metrics, or changes in an index or market rate.

While some variable payments based on indices or rates may be included in the initial lease liability calculation, others are recognized as expenses when they occur. Properly identifying which variable payments should be included in the liability calculation is crucial for accurate accounting.

Residual Value Guarantees

Residual value guarantees are commitments made by the lessee to ensure that the leased asset retains a certain value at the end of the lease term. If the asset’s market value falls below the guaranteed amount, the lessee may be required to compensate the lessor for the difference.

The expected amount payable under a residual value guarantee is included when calculating the lease liability, as it represents a potential future payment obligation.

Purchase Options

Some lease agreements include purchase options that allow the lessee to buy the leased asset at the end of the lease term. If it is reasonably certain that the lessee will exercise this option, the purchase price is included in the lease liability calculation.

This ensures that the financial statements reflect the full expected obligation related to the lease arrangement. Properly evaluating purchase options is important because it can significantly influence both the lease liability and the right-of-use asset recognized by the company.

How to Calculate Lease Liabilities

Calculating lease liabilities is a structured process guided by accounting standards such as IFRS 16 and ASC 842. The main objective is to determine the present value of future lease payments, which represents the financial obligation a business must record on its balance sheet. By discounting future payments to their current value, companies can accurately reflect the economic impact of leasing assets such as buildings, vehicles, or equipment.

Identify All Lease Payments

The first step is to determine the lease payments that must be included in the calculation. These typically include fixed lease payments specified in the agreement, payments linked to an index or rate, and any expected payments under residual value guarantees.

In some cases, lease agreements also include optional renewal periods. If the business is reasonably certain it will exercise the extension option, the payments related to that period must also be included in the lease liability calculation.

Determine the Discount Rate

The next step is selecting the appropriate discount rate used to calculate the present value of lease payments. Ideally, businesses should use the interest rate implicit in the lease, which reflects the rate that equates the present value of lease payments with the fair value of the leased asset.

However, this rate is not always available. In such cases, companies use their incremental borrowing rate, which represents the interest rate they would pay to borrow funds to purchase a similar asset over a comparable period. The chosen rate significantly influences the final lease liability amount.

Define the Lease Term

The lease term determines the total duration over which payments are considered in the calculation. It includes the non-cancellable lease period along with any renewal or extension options that the lessee is reasonably certain to exercise.

Evaluating the lease term often requires judgment, especially when businesses frequently extend lease agreements or have economic incentives to continue using the asset beyond the initial term.

Apply the Present Value Calculation

Once the lease payments, discount rate, and lease term are determined, businesses calculate the present value of future payments. Each lease payment is discounted using the selected rate to reflect its value at the start of the lease.

The sum of all discounted payments represents the lease liability recorded on the balance sheet. This calculation ensures that the liability reflects the economic cost of the lease rather than the total cash payments over time.

Example of Lease Liability Calculation

Consider a company that leases equipment and agrees to pay ₹20,000 annually for five years. If the discount rate applied is 5 percent, the business calculates the present value of those five payments rather than simply multiplying the annual payment by the lease term.

After applying the present value formula, the total lease liability recorded on the balance sheet will be lower than the total cash paid over the lease period because future payments are adjusted to their current value. This approach ensures that financial statements provide a realistic representation of the company’s lease obligations.

Lease Liabilities in Financial Statements

Lease liabilities affect multiple financial statements because they represent a long-term obligation arising from a lease agreement. Under modern accounting standards such as IFRS 16 and ASC 842, leases are no longer treated merely as operating expenses.

Instead, they are recognized as both an asset and a liability, which impacts the balance sheet, income statement, and cash flow statement. Understanding how lease liabilities appear in these financial statements helps businesses evaluate their financial position and performance more accurately.

Balance Sheet

Recognition as a liability

On the balance sheet, lease liabilities are recorded as a financial obligation representing the present value of future lease payments. When a company enters into a lease agreement, it recognizes this liability at the commencement date of the lease.

Over time, the liability decreases as lease payments are made, while interest expense increases the liability before each payment is applied. Lease liabilities are usually classified into current and non-current portions, depending on the timing of the remaining payments.

Relationship with right-of-use assets

Alongside the lease liability, companies also recognize a right-of-use (ROU) asset on the balance sheet. This asset represents the company’s right to use the leased property or equipment for the duration of the lease term.

The initial value of the ROU asset is generally equal to the lease liability, adjusted for initial direct costs, lease incentives, or prepaid lease payments.

While the lease liability is gradually reduced as payments are made, the ROU asset is depreciated over the lease term, reflecting the consumption of the leased asset’s economic benefits.

Income Statement

Interest expense

Lease liabilities generate interest expense over time. Each lease payment includes two components: an interest portion and a principal portion. The interest portion is calculated based on the outstanding lease liability and the discount rate used in the lease calculation. This interest expense is recorded in the income statement and typically decreases over time as the lease liability balance declines.

Depreciation of right-of-use assets

The right-of-use asset recognized at the beginning of the lease is depreciated throughout the lease term. This depreciation expense is also recorded in the income statement.

As a result, lease accounting usually leads to two separate expenses being recognized—interest expense on the lease liability and depreciation of the ROU asset. This differs from earlier accounting approaches where lease payments were often recorded as a single operating expense.

Cash Flow Statement

Operating vs financing cash flows

Lease payments also affect the cash flow statement, but the classification depends on the accounting standard applied. Under IFRS 16, the principal portion of lease payments is typically recorded as a financing cash outflow, while the interest portion may be classified as either operating or financing cash flow depending on the company’s accounting policy.

Under US GAAP (ASC 842), operating lease payments are generally classified as operating cash flows, while finance lease payments are divided between operating (interest portion) and financing (principal portion). This classification helps users of financial statements better understand how lease obligations affect a company’s operating and financing activities.

Journal Entries for Lease Liabilities

Lease accounting involves several journal entries throughout the lifecycle of a lease agreement. Under modern accounting standards, businesses must record the initial recognition of the lease, the interest expense associated with the lease liability, and the periodic lease payments.

These entries ensure that the company’s financial records accurately reflect its obligations and the gradual reduction of the lease liability over time.

Initial Recognition of Lease Liability and Right-of-Use Asset

At the start of a lease agreement (known as the lease commencement date), the business recognizes both a lease liability and a right-of-use (ROU) asset. The lease liability represents the present value of future lease payments, while the ROU asset reflects the company’s right to use the leased asset during the lease term.

Journal Entry at Lease Commencement:

The amount recorded is based on the present value of the lease payments calculated using the appropriate discount rate.

Recording Interest Expense on Lease Liability

After the lease is recognized, the lease liability accrues interest expense over time. This interest is calculated on the outstanding lease liability using the discount rate determined during the initial measurement.

Journal Entry to Record Interest Expense:

This entry increases the lease liability before the actual lease payment is applied.

Recording Lease Payments

When the business makes a lease payment, the payment reduces the lease liability. A portion of the payment covers the interest expense, while the remaining portion reduces the principal balance of the lease liability.

Journal Entry for Lease Payment:

The exact allocation between interest and principal depends on the amortization schedule of the lease liability.

Recording Depreciation of the Right-of-Use Asset

In addition to the lease liability entries, the company must also record depreciation on the right-of-use asset throughout the lease term. This reflects the consumption of the asset’s economic benefits over time.

Journal Entry for Depreciation:

These journal entries ensure that both the liability and the asset are properly accounted for during the lease period, providing an accurate representation of the company’s financial obligations and asset usage in its financial statements.

Benefits of Lease Liability Accounting Treatment

Recognizing lease liabilities in accounting provides greater transparency and accuracy in financial reporting. Modern accounting standards require businesses to record lease obligations directly on the balance sheet, allowing stakeholders to better understand the company’s financial commitments. This approach improves financial visibility, enhances decision-making, and ensures compliance with accounting regulations.

Improved Financial Transparency

One of the primary benefits of lease liability accounting is increased financial transparency. By recognizing lease obligations on the balance sheet, businesses provide a clearer view of their long-term commitments. Investors, lenders, and other stakeholders can easily assess the company’s financial position without relying on disclosures in footnotes or supplementary reports.

More Accurate Financial Statements

Lease liability accounting ensures that financial statements accurately reflect the economic impact of lease agreements. Recording the present value of lease payments provides a realistic picture of a company’s obligations. This helps organizations present a more precise balance sheet, making it easier to evaluate financial health and operational performance.

Better Decision-Making

When lease liabilities are properly recorded, management gains better insight into the company’s financial obligations and cash flow requirements. This information supports more informed decisions regarding leasing versus purchasing assets, negotiating lease terms, and planning future investments. Accurate lease accounting also helps businesses evaluate the true cost of using leased assets.

Improved Financial Ratio Analysis

Recognizing lease liabilities directly on the balance sheet allows financial ratios to better reflect the company’s actual financial position. Ratios such as debt-to-equity, return on assets, and leverage ratios become more meaningful because lease commitments are included in the company’s total obligations. This provides analysts and investors with a more reliable basis for comparison across organizations.

Stronger Compliance with Accounting Standards

Lease liability accounting ensures compliance with modern accounting standards such as IFRS 16 and ASC 842. Adhering to these standards helps businesses avoid regulatory issues, maintain accurate financial reporting, and meet audit requirements. Compliance also strengthens stakeholder confidence in the organization’s financial practices.

Enhanced Investor and Lender Confidence

Transparent reporting of lease liabilities improves trust among investors, lenders, and financial institutions. When lease commitments are clearly reflected in financial statements, stakeholders can better evaluate the company’s financial stability and risk exposure. This level of transparency can strengthen business relationships and support access to financing when needed.

Challenges Businesses Face in Managing Lease Liabilities

While recognizing lease liabilities improves financial transparency, managing them can be complex for many businesses. Organizations often deal with multiple lease agreements, varying payment structures, and strict compliance requirements under modern accounting standards. Without proper systems and processes, tracking and reporting lease liabilities accurately can become time-consuming and prone to errors.

Complex Calculations and Measurements

Lease liability calculations require businesses to determine the present value of future lease payments using appropriate discount rates. This involves identifying fixed payments, variable payments tied to an index, residual value guarantees, and potential extension options. Even small changes in assumptions—such as the discount rate or lease term—can significantly affect the calculated liability, making the process complicated for finance teams.

Managing Multiple Lease Agreements

Many companies lease several assets simultaneously, including office spaces, warehouses, vehicles, and equipment. Tracking the details of each lease—such as payment schedules, renewal options, and termination clauses—can be difficult when managed manually. As the number of leases increases, maintaining accurate records and monitoring payment obligations becomes more challenging.

Compliance with Accounting Standards

Accounting standards such as IFRS 16 and ASC 842 require businesses to follow specific rules for recognizing, measuring, and disclosing lease liabilities. These regulations demand consistent documentation, detailed calculations, and proper financial reporting. Failure to comply with these requirements can result in inaccurate financial statements and potential audit issues.

Ongoing Reassessments and Modifications

Lease agreements are not always static. Businesses may renegotiate lease terms, extend lease periods, or modify payment structures during the lease lifecycle. When such changes occur, companies must reassess the lease liability and adjust the right-of-use asset accordingly. These remeasurements require careful analysis and updated calculations, adding another layer of complexity to lease management.

Data Management and Reporting Difficulties

Accurate lease liability accounting depends on reliable data from lease agreements, payment schedules, and financial records. When information is stored across spreadsheets or separate systems, it becomes difficult to maintain consistency and generate reliable reports. Poor data management can lead to calculation errors, incomplete disclosures, and inefficiencies in financial reporting.

Best Practices for Managing Lease Liabilities

Effectively managing lease liabilities is essential for maintaining accurate financial records and ensuring compliance with accounting standards. As businesses often manage multiple leases with varying terms and payment structures, adopting structured processes and reliable systems can simplify lease accounting. Implementing best practices helps organizations track lease obligations more efficiently, reduce errors, and improve financial reporting.

Maintain a Centralized Lease Database

One of the most effective ways to manage lease liabilities is to maintain a centralized repository for all lease agreements. This database should include key details such as lease terms, payment schedules, renewal options, and discount rates. Having all lease-related information in one place makes it easier for finance teams to monitor obligations, access documentation quickly, and maintain consistency in reporting.

Clearly Define Lease Terms and Conditions

Carefully reviewing and documenting lease terms is essential for accurate liability calculations. Businesses should clearly identify elements such as the lease duration, payment structure, variable payment clauses, and purchase options. Properly defining these details helps ensure that all relevant payments are included in the lease liability calculation and reduces the risk of misinterpretation.

Use Accurate Discount Rates

Selecting the correct discount rate is critical for calculating the present value of lease payments. Businesses should use the interest rate implicit in the lease whenever possible or determine an appropriate incremental borrowing rate if the implicit rate is unavailable. Applying the correct rate ensures that the recorded lease liability accurately reflects the economic value of future payment obligations.

Regularly Review and Update Lease Data

Lease agreements may change during their lifecycle due to renegotiations, extensions, or modifications. Companies should periodically review lease data to ensure that any changes are reflected in their accounting records. Updating lease information promptly helps businesses adjust lease liabilities and right-of-use assets accurately when conditions change.

Implement Automated Lease Accounting Tools

Manual tracking of lease liabilities using spreadsheets can be time-consuming and prone to errors, especially for organizations managing numerous leases. Using automated accounting or ERP systems can simplify the process by performing calculations, generating amortization schedules, and updating financial records automatically. Automation improves efficiency and reduces the likelihood of calculation errors.

Ensure Compliance with Accounting Standards

Businesses must ensure that their lease accounting practices align with applicable standards such as IFRS 16 or ASC 842. This includes proper recognition of lease liabilities, accurate measurement of lease payments, and complete financial disclosures. Regular internal reviews and audits can help organizations maintain compliance and ensure that their financial statements accurately reflect lease obligations.

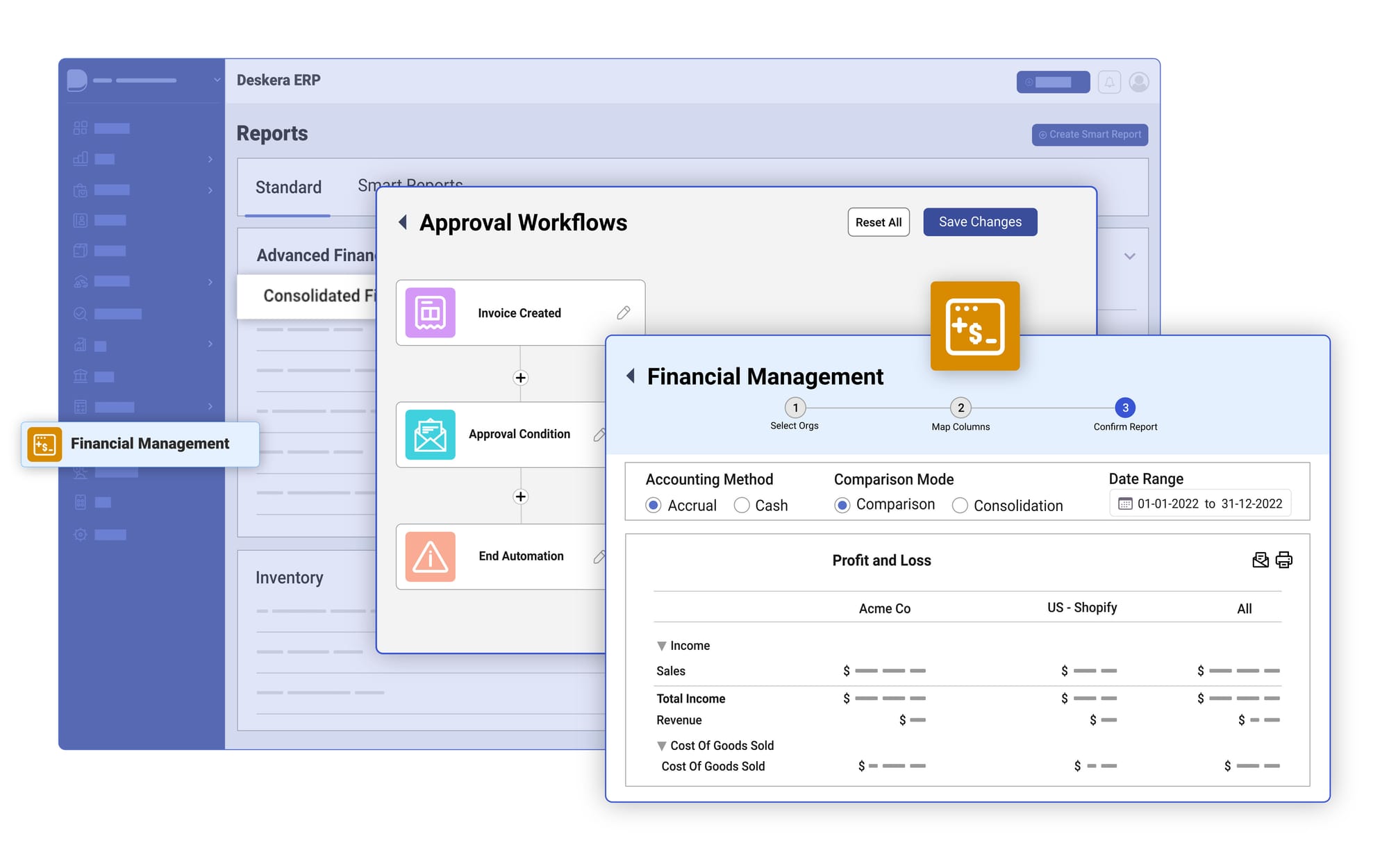

How Deskera ERP Helps Manage Lease Liabilities

Managing lease liabilities requires accurate calculations, consistent journal entries, and clear financial reporting. Manual tracking using spreadsheets can make this process complicated, especially for businesses managing multiple leases. Deskera ERP helps simplify lease accounting by integrating lease-related financial data into a centralized accounting system and automating key financial processes.

Centralized Financial Data Management

Deskera ERP provides a centralized general ledger where businesses can record and track lease-related transactions such as lease liabilities, right-of-use assets, lease payments, and interest expenses. Keeping all financial data in a single system improves visibility and helps finance teams maintain consistent and organized records for lease agreements.

Automated Journal Entries

Lease accounting involves recurring entries for interest expenses, depreciation of right-of-use assets, and periodic lease payments. Deskera ERP allows businesses to automate journal entries and recurring transactions, reducing manual work and minimizing the risk of calculation errors during monthly or annual financial closing processes.

Accurate Financial Reporting

With built-in financial reporting tools, Deskera ERP enables businesses to generate balance sheets, income statements, and other financial reports that reflect lease liabilities and related expenses. This helps organizations maintain transparency in financial reporting and ensures that lease obligations are properly reflected in financial statements.

Integration With Asset and Financial Management

Deskera ERP integrates accounting with other financial modules such as fixed asset management and financial planning. This allows businesses to track right-of-use assets alongside other company assets, manage depreciation, and analyze the financial impact of leases within the broader financial ecosystem.

Real-Time Visibility and Audit Trails

The platform provides real-time dashboards and detailed audit trails for financial transactions. Finance teams can easily track changes to lease entries, monitor outstanding obligations, and maintain proper documentation for audits and compliance requirements. This level of transparency strengthens internal controls and improves financial oversight.

Multi-Currency and Multi-Entity Support

For organizations operating in multiple countries or subsidiaries, Deskera ERP supports multi-currency and multi-entity accounting. This makes it easier to manage lease transactions across different regions while maintaining consistent financial reporting and consolidated financial statements.

Overall, Deskera ERP enables businesses to manage lease liabilities more efficiently by combining automation, centralized financial management, and real-time reporting. By integrating lease accounting with broader financial operations, companies can improve accuracy, maintain compliance with accounting standards, and gain better visibility into their long-term financial commitments.

Key Takeaways

- Lease liabilities represent the present value of future lease payments that a business is obligated to make for using leased assets, ensuring that financial commitments are clearly reflected in accounting records.

- Modern lease accounting standards such as IFRS 16 and ASC 842 require businesses to recognize most leases on the balance sheet through both lease liabilities and right-of-use assets.

- Several elements influence lease liability calculations, including lease payments, discount rates, lease terms, variable payments, residual value guarantees, and purchase options.

- Calculating lease liabilities involves identifying lease payments, selecting the appropriate discount rate, determining the lease term, and applying present value calculations to future payments.

- Lease liabilities impact multiple financial statements, including the balance sheet, income statement, and cash flow statement, affecting both financial reporting and performance analysis.

- Lease accounting requires specific journal entries for initial recognition, interest expense, lease payments, and depreciation of the right-of-use asset throughout the lease term.

- Recognizing lease liabilities improves financial transparency, enhances the accuracy of financial statements, and provides stakeholders with a clearer view of a company’s long-term obligations.

- Businesses often face challenges such as complex calculations, managing multiple leases, compliance with accounting standards, and maintaining accurate financial records.

- Implementing best practices such as centralized lease tracking, regular reviews, accurate discount rate selection, and automation can simplify lease liability management.

- ERP systems like Deskera ERP help businesses manage lease liabilities more efficiently by centralizing financial data, automating accounting processes, and improving financial reporting accuracy.

Related Articles